TL;DR: The Income-tax Department notified the seven ITR forms for AY 2026-27 vide CBDT Notification No. 45/2026 dated 30 March 2026 (with a corrigendum dated 10 April 2026). For an individual or HUF filer, the choice is between four forms — ITR-1 (Sahaj), ITR-2, ITR-3, and ITR-4 (Sugam). The two material expansions this year are inside ITR-1 (and the parallel ITR-4): up to two house properties are now permitted (was one), and long-term capital gain under Section 112A up to Rs. 1,25,000 from listed equity / equity mutual funds can now be reported directly in ITR-1 / ITR-4 (was previously a forced shift to ITR-2). Picking the wrong form does not invalidate the return on its own, but it sets up a Section 139(9) defective return notice with a 15-day rectification window — an entirely avoidable round-trip.

This guide walks the four-way fork in detail, with statute references, the ten most common taxpayer scenarios (matched to the right form), and the recovery path if you have already filed under the wrong form.

1. The Four-Form Quick Reference for Individual / HUF Filers

Form Headline use Total-income cap Residency Business / profession? ITR-1 (Sahaj) Salaried + simple investors Rs. 50 lakh Resident only (excludes RNOR & NR) Not allowed ITR-2 Capital gains, foreign assets, NRI, multi-property No cap Resident, RNOR, NR all eligible Not allowed ITR-3 Any business or professional income No cap Resident, RNOR, NR all eligible Required if you have it ITR-4 (Sugam) Presumptive 44AD / 44ADA / 44AE Rs. 50 lakh Resident individual / HUF / firm (not LLP) Yes, on presumptive basis onlyITR-5, ITR-6, and ITR-7 are for firms/LLPs (other than presumptive on ITR-4), companies, and trusts/political parties respectively — out of scope for this guide.

2. ITR-1 (Sahaj) — Eligibility for AY 2026-27

You can file ITR-1 (Sahaj) only if every one of these conditions holds:

- You are a resident individual (not RNOR — resident but not ordinarily resident, and not non-resident). Residency is determined under Section 6 of the Income-tax Act, 1961.

- Your total income for the year is up to Rs. 50 lakh.

- Income is from one or more of the following heads only:

- Salary or pension

- Up to two house properties (the AY 2026-27 expansion under Notification 45/2026 — earlier ITR-1 capped at one; if the second is let out, declare rent received and municipal taxes paid). This is subject to overall ITR-1 eligibility conditions and to there being no disqualifying carry-forward / brought-forward loss situation — if the let-out property generates a loss you want to carry forward, ITR-2 is required.

- Other sources — bank interest, FD interest, dividends, family pension

- Agricultural income is up to Rs. 5,000.

- Long-term capital gain under Section 112A from listed equity shares or equity mutual funds is up to Rs. 1,25,000 (the second AY 2026-27 expansion). Above this, you must move to ITR-2.

You cannot use ITR-1 if any of these apply:

- You are a director in any company (listed or unlisted, including dormant companies, and including unpaid / non-executive directorships)

- You held unlisted equity shares any time during the year (including ESOPs / RSUs in a private subsidiary, vested but unsold equity in a foreign brokerage account where signing authority gives rise to disclosure)

- You have any short-term capital gain taxable under the capital-gains head (Section 111A or otherwise) — intraday or other speculative gains taxable as business income do not get reported in the capital-gains schedule, but they take you to ITR-3 anyway

- You have LTCG above Rs. 1,25,000, or LTCG under sections other than 112A (debt MF, gold, jewellery, property, foreign assets)

- You have any foreign asset, foreign income, or signing authority on a foreign account

- You want to carry forward any loss to subsequent years (a current-year house-property loss can be reported as a negative figure within ITR-1 itself, but to carry forward requires ITR-2)

- You have any business or professional income

- Agricultural income exceeds Rs. 5,000

- You are a non-resident or RNOR

3. ITR-2 — The Salaried Filer’s Most Common Fallback

If even one ITR-1 condition fails (and you have no business or professional income), you fall to ITR-2. This is the most common form for an upper-middle-class salaried filer who also invests, holds RSUs, or owns property abroad. Typical triggers:

- You sold listed equity / equity MF and your LTCG exceeds Rs. 1.25 lakh, or you have any STCG — ITR-2 has Schedule CG with detailed grandfathering and section-wise reporting

- You are an NRI or RNOR — ITR-2 has the Schedule FA (foreign assets), Schedule FSI (foreign-source income), and Schedule TR (foreign tax credit)

- You hold RSUs / ESOPs / sweat equity in a foreign parent — mandatory disclosure even if not yet sold

- You have more than two house properties

- Total income exceeds Rs. 50 lakh, regardless of how simple the income mix is

- You want to carry forward a current-year loss (capital loss, or house-property loss exceeding the in-year set-off ceiling of Rs. 2 lakh under Section 71)

- You have agricultural income above Rs. 5,000 and want to claim the rebate computation

ITR-2 also handles capital gains exemptions under Sections 54, 54B, 54EC, 54F (re-investment in a residential house, agricultural land, NHAI / REC bonds, or another residential house). If you are claiming any such exemption, ITR-2 is required.

4. ITR-3 — The Moment You Have Any Business or Professional Income

Any material income taxable under the head "Profits and Gains of Business or Profession" generally requires ITR-3, unless you are eligible for and opting into ITR-4 under the presumptive scheme. There is no income threshold — the form applies to a Rs. 1 lakh side-consultancy and a Rs. 10 crore proprietorship alike. Common triggers:

- You ran a sole proprietorship

- You earned freelance or consulting income that you could have reported under Section 44ADA but chose not to (because you had high deductible expenses, or because the receipts crossed Rs. 50 / 75 lakh and disqualify the presumptive route)

- You traded F&O or intraday equity — both flow to ITR-3 as business income, but with different sub-classification: intraday equity is speculative business under the main limb of Section 43(5), while eligible F&O transactions on a recognised stock exchange are non-speculative business under proviso (d) to Section 43(5). Either way, ITR-3 with Schedule BP is mandatory and the speculative / non-speculative split affects set-off and carry-forward (Sections 73 and 72 respectively)

- You held a partnership interest — share of profit, interest on capital, remuneration from a firm all flow into Schedule BP of ITR-3

- Your presumptive turnover exceeded the cap or you opted out of presumptive within the 5-year continuity window under Section 44AD(4)

- You have crypto / VDA trading income that you treat as business (not capital gains)

ITR-3 also handles all the schedules ITR-2 covers (capital gains, foreign assets, multiple properties), so it is the natural form for a combined filer — salary plus property plus capital gains plus a side business.

5. ITR-4 (Sugam) — The Presumptive Form

ITR-4 (Sugam) is the simplified form for residents (individuals, HUFs, and firms other than LLPs) who opt for the presumptive scheme under Section 44AD (eligible business), Section 44ADA (specified professionals), or Section 44AE (goods-carriage operators). The trade-off is simplicity — no books of account, deemed profit, no audit at the relevant cap — in exchange for losing the right to claim actual expenses and accept the deemed margin.

Section Who can use Cap Deemed profit 44AD Eligible business (excluding professionals) Rs. 2 crore turnover (Rs. 3 crore if cash receipts ≤ 5 %) 8 % cash / 6 % digital of turnover 44ADA Specified professionals (legal, medical, accountancy, technical consultancy, etc.) Rs. 50 lakh receipts (Rs. 75 lakh if cash receipts ≤ 5 %) 50 % of gross receipts 44AE Goods-carriage operators (up to 10 vehicles) 10-vehicle ceiling Per-vehicle deemed profit (Rs. 1,000 per ton GVW per month for heavy goods, else Rs. 7,500 per vehicle per month)Eligibility for ITR-4 also requires that your total income is up to Rs. 50 lakh. If your business is presumptive but your salary plus interest plus other sources push total income above Rs. 50 lakh, you cannot use ITR-4 — you must move to ITR-3.

For AY 2026-27, ITR-4 too has been expanded to allow LTCG u/s 112A up to Rs. 1,25,000 in addition to the presumptive business / profession income.

Disqualifiers (must move to ITR-3 if any apply):

- Total income above Rs. 50 lakh

- Any income from outside India or any foreign asset / foreign account signing authority

- Any director / unlisted equity shareholding situation — same as ITR-1

- You are a non-resident or RNOR

- You are claiming relief under Section 90, 90A or 91 (DTAA)

- Capital gain other than LTCG u/s 112A up to Rs. 1.25L (any STCG, larger LTCG, sale of property, etc.)

6. The Decision Tree, Step by Step

Walk through these gates in order. The first gate that disqualifies you tells you which form to use.

- Are you a non-resident or RNOR for FY 2025-26?

- Yes → ITR-2 (or ITR-3 if you also have business / professional income earned in or related to India)

- No → continue

- Do you have any business or professional income? (consultancy invoices, F&O, intraday equity, sole proprietorship, partner-share in a firm)

- Yes, presumptive 44AD / 44ADA / 44AE eligible and total income ≤ Rs. 50 lakh and no foreign assets → ITR-4 (Sugam)

- Yes, otherwise → ITR-3

- No → continue

- Do you have any STCG, or LTCG above Rs. 1,25,000, or LTCG outside Section 112A?

- Yes → ITR-2

- No → continue

- Do you hold any foreign asset, foreign income, or signing authority on a foreign account?

- Yes → ITR-2

- No → continue

- Are you a director in any company, or do you hold unlisted equity shares (including private-company ESOPs)?

- Yes → ITR-2

- No → continue

- Is your total income above Rs. 50 lakh?

- Yes → ITR-2

- No → continue

- Do you own more than two house properties, or want to carry forward any loss?

- Yes → ITR-2

- No → ITR-1 (Sahaj)

The official e-filing portal also offers a guided "Help me decide which ITR" flow that walks the same decision tree with portal-side prompts.

7. Ten Worked Examples

Each example is a realistic AY 2026-27 fact pattern. We have used round numbers to keep the form-pick obvious.

Example 1 — Pure salaried, one house, no investments

Anjali earns Rs. 14 lakh salary, has one self-occupied home loan, no capital gains, no business income, no foreign assets. Form: ITR-1 (Sahaj).

Example 2 — Salaried, two houses, small equity LTCG

Ravi earns Rs. 18 lakh salary, owns two flats (one self-occupied, one rented out), and sold listed equity at a Rs. 1.10 lakh long-term gain (below the Rs. 1.25 lakh threshold of Section 112A). Form: ITR-1 (Sahaj) — the AY 2026-27 expansion covers exactly this case.

Example 3 — Salaried, equity LTCG above Rs. 1.25 lakh

Same Ravi, but the equity LTCG is Rs. 1.80 lakh. Form: ITR-2. Even Re. 1 above Rs. 1,25,000 forces the shift.

Example 4 — Salaried + intraday trading

Sneha earns Rs. 12 lakh salary and made Rs. 60,000 from intraday equity trading (turnover Rs. 4 lakh, ICAI 8th-edition methodology). Intraday is speculative business under Section 43(5). Form: ITR-3.

Example 5 — Freelance consultant on presumptive 44ADA

Kabir invoiced Rs. 28 lakh as a freelance product designer (95 % digital), no other income. He opts for Section 44ADA at 50 % deemed profit. Total income computes to Rs. 14 lakh. Form: ITR-4 (Sugam).

Example 6 — Salaried + freelance side income above 44ADA cap

Asha earns Rs. 16 lakh salary and Rs. 90 lakh freelance receipts. She is a specified professional, but her receipts cross the Rs. 75 lakh cap (95 % digital). Section 44ADA is unavailable. Form: ITR-3.

Example 7 — NRI with rental income from India

Priya is a Singapore-resident NRI. She earns Rs. 9 lakh rent from her Pune flat and Rs. 40,000 NRO interest. Form: ITR-2. NRIs cannot use ITR-1.

Example 8 — Salaried + ESOPs vested from a US parent

Manish earns Rs. 22 lakh salary and has vested RSUs in his US parent company (held, not sold). The foreign-asset disclosure under Schedule FA is mandatory. Form: ITR-2.

Example 9 — Director of a private company, salary + dividend

Rohan is a director of a Pvt. Ltd. company, earns Rs. 18 lakh salary plus Rs. 1.5 lakh dividend. Director-status disqualifies ITR-1 / ITR-4. Form: ITR-2.

Example 10 — Salaried + sold inherited property

Lakshmi earns Rs. 11 lakh salary and sold her inherited Hyderabad property in October 2025 for Rs. 80 lakh, against an indexed cost (acquired pre-2001) of Rs. 25 lakh. She wants to claim Section 54 exemption by re-investing in a new flat. The capital gain is computed under Section 48 / 112 and the exemption is in Schedule CG of ITR-2. Form: ITR-2.

8. What Happens If You File the Wrong Form

The Income-tax Department’s system runs validation checks on the ITR utility. If you file ITR-1 with disqualifying conditions (for example, you ticked “director — yes” or your total income exceeds Rs. 50 lakh), the portal usually catches it at submission and warns you. But many wrong-form cases pass through — you forgot a capital gain entry, or your share of a partnership firm was missed.

If the wrong form is detected post-submission, the Centralised Processing Centre (CPC) issues a Section 139(9) defective return notice. The notice typically provides around 15 days from the date of issue to rectify by filing a correction in the right form, subject to the period actually specified in the notice or any extension granted by the Assessing Officer on a written application. If you do not respond within the period given, the return is treated as invalid — equivalent to never having filed at all. That, in turn, can trigger:

- Section 234F late filing fee (Rs. 5,000; Rs. 1,000 if total income below Rs. 5 lakh)

- Loss of carry-forward rights for any capital / business loss in the year

- Loss of the right to revise to old regime if you had business income (Form 10-IEA option lapses)

- Interest under Section 234A from the original due date until the eventual filing date

Practical rule: respond to a 139(9) notice the same day it lands. The notice tells you which schedule failed validation; correcting and re-submitting with the right ITR form takes under thirty minutes.

9. Already Filed in the Wrong Form? File a Revised Return

If your return has been processed (Section 143(1) intimation already received) and you realise the form was wrong — for example you missed reporting an STCG and filed ITR-1 instead of ITR-2 — the cleanest correction is a revised return under Section 139(5). The revised return:

- Can be filed at any time before 31 December 2026 or before completion of assessment, whichever is earlier

- Replaces the original return entirely; the revision must be in the correct form

- Is filed using the same e-filing flow but with “Filing Type” set to Revised under Section 139(5); you enter the original ITR’s receipt number and date

- Does not attract the Section 234F late fee provided the original return was on time

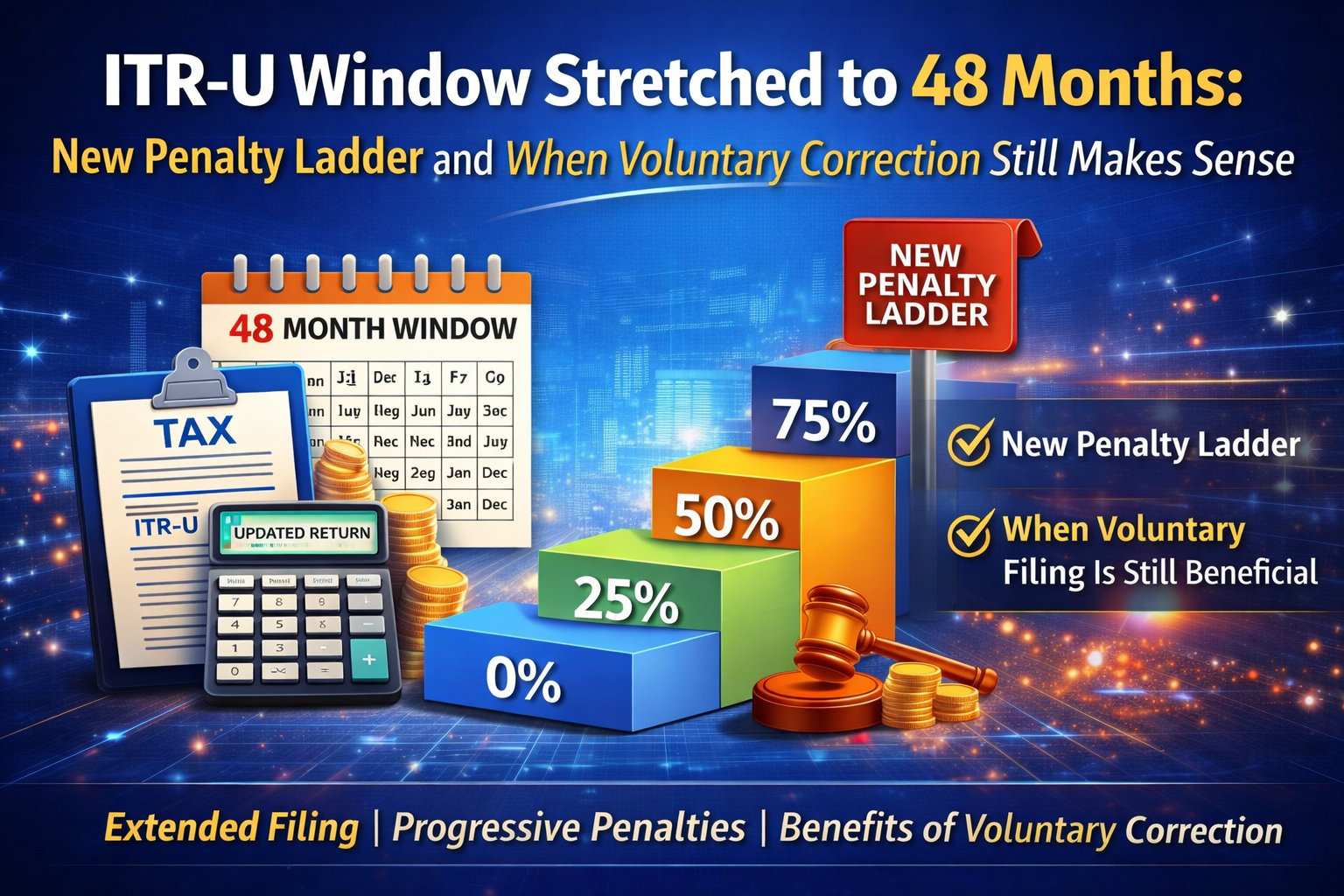

If the deadline for revised returns has also passed and you still need to fix something material (typically reported income), an updated return under Section 139(8A) is the last resort — available within 48 months from the end of the relevant assessment year (extended from 24 months by the Finance Act, 2025), with additional tax on the differential income (25 % up to 12 months, 50 % up to 24 months, 60 % up to 36 months, 70 % up to 48 months). An updated return can never reduce your reported income or claim a refund — it can only increase liability.

10. Common Pitfalls and How to Avoid Them

- “I sold equity for a small loss — can I use ITR-1?” No. STCG is reported even if it is negative, and any STCG (positive or negative) requires ITR-2. Same for LTCG losses on equity.

- “My ESOPs vested but I haven’t sold — just salary, right?” The vested portion is taxable as a perquisite under Section 17(2) and the underlying foreign-asset disclosure is mandatory if the parent is offshore. ITR-2.

- “Partnership share-of-profit is exempt — do I still need ITR-3?” Yes. Even though share-of-profit is exempt under Section 10(2A), the partner has business income (interest on capital and / or remuneration) reportable in Schedule BP of ITR-3.

- “I’m on presumptive 44ADA but earned a small dividend — can I still use ITR-4?” Yes — dividends are “other sources”, not capital gains, and ITR-4 accommodates them. The disqualifier is capital gain (other than LTCG u/s 112A up to Rs. 1.25L) or foreign asset, not dividend income.

- “I have a property sold but I’m claiming Section 54 exemption — do I still need ITR-2?” Yes. The Section 54 claim is reported in Schedule CG of ITR-2 (or ITR-3); the gain has to be disclosed even when fully exempted.

- “My total income is exactly Rs. 50,00,001.” Above Rs. 50 lakh forces ITR-2 (or ITR-3) regardless of how simple the income mix is. The ITR-1 cap is hard.

- “I changed residency status mid-year — what now?” If you are RNOR or NR for FY 2025-26 under Section 6, ITR-1 is unavailable. ITR-2 is the default; ITR-3 if there is also business income.

- “I have agricultural income of Rs. 30,000 — can I use ITR-1?” No. Agricultural income above Rs. 5,000 forces ITR-2 / ITR-3 (so the rebate calculation can run with the agricultural income separately).

11. Statutory and Notification References

- CBDT Notification No. 45/2026 dated 30 March 2026 (with corrigendum dated 10 April 2026) — ITR forms for AY 2026-27. Source for ITR-1 expansion (two house properties; LTCG u/s 112A up to Rs. 1,25,000).

- Section 6, Income-tax Act, 1961 — residence rules; basis for ITR-1 residency carve-out (resident only, not RNOR / NR).

- Section 5, Income-tax Act, 1961 — scope of total income for residents and non-residents.

- Section 139(1), Income-tax Act, 1961 — due dates for filing return; 31 July 2026 for non-audit individuals (any other assessee), 31 October 2026 for audit cases, 30 November 2026 for transfer-pricing cases.

- Section 139(5), Income-tax Act, 1961 — revised return; 31 December 2026 outer limit (or completion of assessment, whichever earlier).

- Section 139(8A) read with Section 140B, Income-tax Act, 1961 — updated return (ITR-U); time limit extended from 24 months to 48 months from end of relevant AY by the Finance Act, 2025, with graduated additional tax under Section 140B (25 % within 12 months, 50 % within 24, 60 % within 36, 70 % within 48 months). Refer to the operative text of Section 139(8A) and Section 140B as in force for the relevant date of furnishing.

- Section 139(9), Income-tax Act, 1961 — defective return; 15-day rectification window from issue of notice.

- Section 44AD, Income-tax Act, 1961 — presumptive scheme for eligible business; Rs. 3 crore turnover cap with 5 % cash limit; 6 % digital / 8 % cash deemed profit. (Corresponding provision exists at Section 58 of the Income-tax Act, 2025, which becomes operative for income from 1 April 2026 onwards — that is, Tax Year 2026-27, not the AY 2026-27 return covered by this guide.)

- Section 44ADA, Income-tax Act, 1961 — presumptive scheme for specified professionals; Rs. 75 lakh / Rs. 50 lakh cap; 50 % deemed profit. (Corresponding provision in the 2025 Act applies prospectively, as above.)

- Section 44AE, Income-tax Act, 1961 — presumptive scheme for goods-carriage operators; per-vehicle deemed profit.

- Section 43(5), Income-tax Act, 1961 — speculative-transaction definition; basis for treating intraday equity as speculative business and F&O as non-speculative business (proviso (d)).

- Section 111A, Income-tax Act, 1961 — STCG on listed equity (20 % for transfers on or after 23 July 2024).

- Section 112A, Income-tax Act, 1961 — LTCG on listed equity (12.5 % above Rs. 1.25 lakh, for transfers on or after 23 July 2024).

- Section 234F, Income-tax Act, 1961 — late filing fee.

- Section 234A, Income-tax Act, 1961 — interest for delay in filing return.

This guide reflects the AY 2026-27 ITR form notifications as on 6 May 2026. The official ITR utility / JSON schema released on the e-filing portal may further refine practical eligibility (additional validation rules, schedule constraints, JSON-level reporting requirements) on top of what the notified form text says. Subsequent CBDT clarifications, FAQ updates, or schema-level changes via portal release notes can shift the form-eligibility lines. Even unsold foreign RSUs / ESOPs may trigger Schedule FA disclosure requirements regardless of which form you choose. For complex residency, business-classification, or capital-gains exemption questions, consult a practising chartered accountant. Nothing on this page is a substitute for professional advice.

Comments (0)

No comments yet. Be the first to comment!