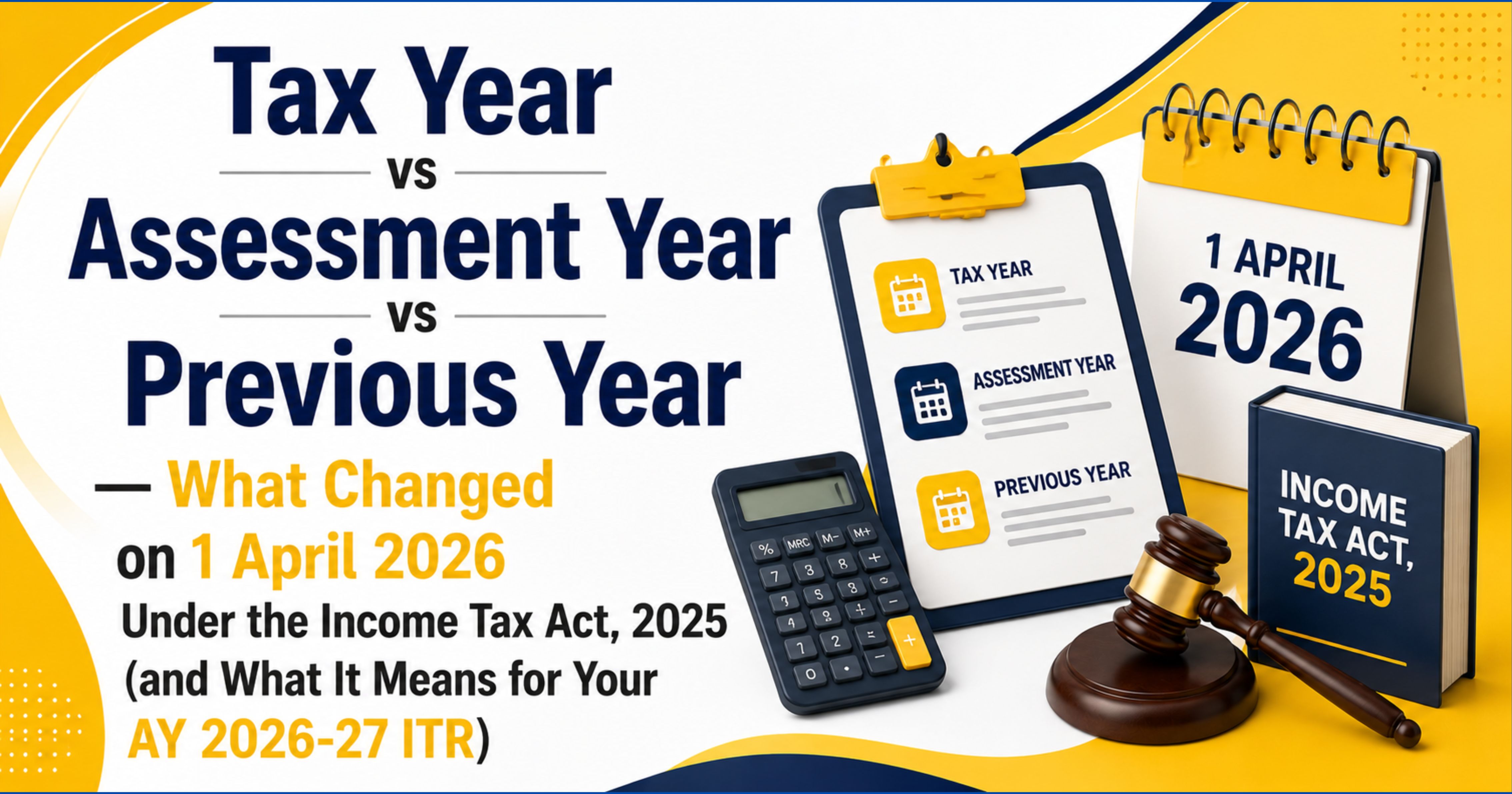

Tax Year vs Assessment Year vs Previous Year — What Changed on 1 April 2026 Under the Income Tax Act, 2025 (and What It Means for Your AY 2026-27 ITR)

Karan is part of the founding editorial team at TaxSocial and writes flagship pieces on tax-law transitions and high-stakes filing decisions. He covers the Income-tax Act 2025 commencement on 1 April 2026, the Tax Year vs Assessment Year vs Previous Year vocabulary shift, capital gains exemptions on sale of house property under Sections 82, 85 and 86 of the new Act, and the cross-year transitional questions practitioners have been asking since the Act was published. His articles are built around the bare Act text, the Income-tax Rules 2026 notified by CBDT, and Section 536 savings clauses that govern how 1961-Act matters are preserved into the new framework. He is a regular contributor on the Section 148 reassessment and dispute-resolution beats.