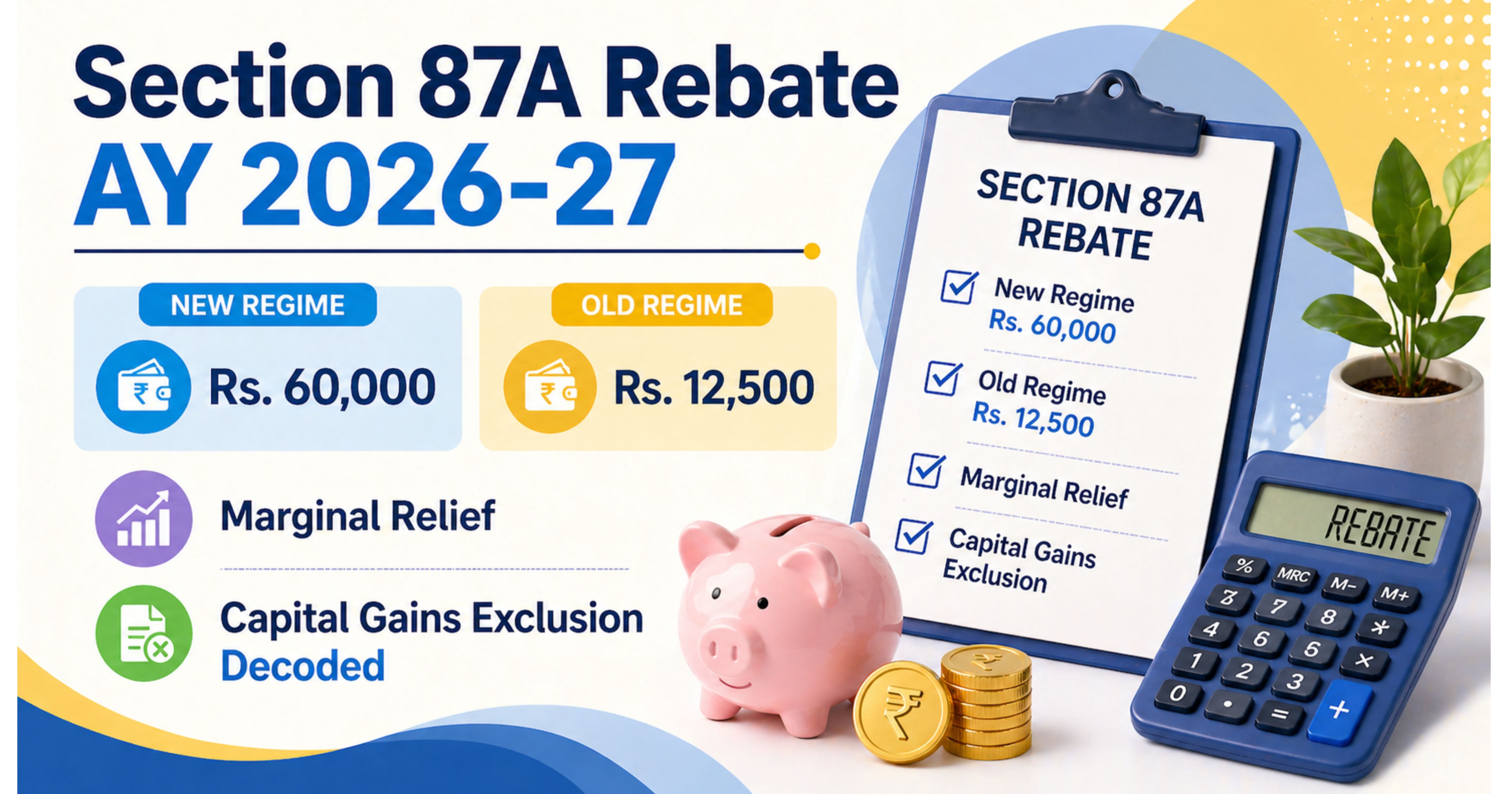

TL;DR for AY 2026-27 (FY 2025-26): A resident individual gets a Section 87A rebate of up to Rs. 60,000 under the new regime (default) if total income is up to Rs. 12,00,000 per the Finance Act 2025; or up to Rs. 12,500 under the old regime if total income is up to Rs. 5,00,000. The rebate works only against tax computed at slab rates. Tax on STCG under Section 111A, LTCG under Section 112 / 112A, and casual income under Section 115BB is at special rates and is excluded from the rebate per the department’s current ITR-utility view (matter sub judice before the Bombay High Court). Marginal relief above Rs. 12 lakh keeps the tax from overshooting the income that exceeds Rs. 12 lakh.

1. What is Section 87A and Who Can Claim It?

Section 87A of the Income-tax Act, 1961 gives a resident individual a rebate against income-tax payable, subject to a total-income ceiling. It is not a deduction from income — it is a deduction from tax. The provision applies only to:

- Resident individuals (residents of India in the previous year per Section 6).

- Total income (Gross Total Income reduced by Chapter VI-A deductions) not exceeding the prescribed threshold.

It is not available to:

- Non-residents (NRIs / RNORs in years they are non-resident).

- Hindu Undivided Families, firms, LLPs, companies, AOPs, BOIs.

- Any person whose total income exceeds the prescribed ceiling, even by Re. 1 — except where marginal relief applies (new regime, Rs. 12 lakh threshold).

2. New Regime (Default) Rebate for AY 2026-27 — Rs. 60,000 up to Rs. 12 Lakh

From AY 2024-25, the new regime under Section 115BAC became the default for individuals and HUFs. To use the old regime where eligible, you must opt out via Form 10-IEA. The Finance Act 2025 amended Section 115BAC for AY 2026-27 onwards as follows:

Total income (Rs.) Tax rate (new regime, AY 2026-27) Up to 4,00,000 Nil 4,00,001 – 8,00,000 5% 8,00,001 – 12,00,000 10% 12,00,001 – 16,00,000 15% 16,00,001 – 20,00,000 20% 20,00,001 – 24,00,000 25% Above 24,00,000 30%Under this slab structure, tax on Rs. 12,00,000 works out to exactly Rs. 60,000: 5% on (8L − 4L) = Rs. 20,000, plus 10% on (12L − 8L) = Rs. 40,000 = Rs. 60,000. The Section 87A rebate (Rs. 60,000) cancels this tax to nil, before health-and-education cess. With the Rs. 75,000 standard deduction for salaried taxpayers, the effective tax-free salary is around Rs. 12,75,000 under the new regime for AY 2026-27 — assuming standard deduction is the only adjustment and there is no income chargeable at special rates (e.g., STCG 111A, LTCG 112A) and no other income beyond salary.

Quick check — is your total income at or below Rs. 12 lakh?

- If yes: tax at slab rates is automatically reduced to nil by the rebate (assuming no income chargeable at special rates).

- If no but total income is between Rs. 12,00,001 and roughly Rs. 12,75,000: marginal relief kicks in (covered in Section 5).

- If income is well above the marginal-relief band: no rebate; tax follows the full slab table.

3. Old Regime Rebate — Rs. 12,500 up to Rs. 5 Lakh (Unchanged)

If you opt out of the new regime via Form 10-IEA — one-time election for assessees with business or professional income (returnable to new regime once in a lifetime), and an annual choice in the return for non-business assessees — the old slabs apply:

Total income (Rs.) Tax rate (old regime — individual below 60) Up to 2,50,000 Nil 2,50,001 – 5,00,000 5% 5,00,001 – 10,00,000 20% Above 10,00,000 30%Senior citizen (60-79) basic exemption is Rs. 3,00,000; super senior (80+) is Rs. 5,00,000. Standard deduction for salaried under the old regime is Rs. 50,000.

Under the old regime, the Section 87A rebate is Rs. 12,500 if total income does not exceed Rs. 5,00,000. Tax on Rs. 5 lakh at old slabs = Rs. 12,500 (5% on Rs. 2.5 lakh) — the rebate cancels it to nil. There is no marginal relief in the old regime: if total income is even Rs. 5,00,001, you lose the rebate entirely and pay tax from Rs. 2,50,001 onwards.

4. The Slab Math — Exactly How the Rebate Cancels Your Tax

The rebate is the lower of:

- The income-tax computed at slab rates on total income, or

- The cap (Rs. 60,000 new regime / Rs. 12,500 old regime).

So if your total income is Rs. 7,50,000 under the new regime, slab tax is Rs. 17,500 (5% on Rs. 3.5 lakh between Rs. 4 lakh and Rs. 7.5 lakh). Rebate = lower of (Rs. 17,500 or Rs. 60,000) = Rs. 17,500. Tax payable = nil. Health-and-education cess at 4% applies on the income-tax after rebate, so cess is also nil here.

The rebate cap of Rs. 60,000 only matters at incomes between Rs. 8 lakh and Rs. 12 lakh, where slab tax begins to exceed Rs. 20,000 and approaches Rs. 60,000.

5. Marginal Relief — What Happens Just Above Rs. 12 Lakh?

Without relief, an income of Rs. 12,01,000 would attract slab tax of Rs. 60,150 (Rs. 60,000 up to Rs. 12 lakh + 15% on Rs. 1,000) — and the entire rebate would vanish because total income exceeds the ceiling. The taxpayer earning Rs. 1,000 extra would pay Rs. 60,150 more in tax. That is the cliff Finance Act 2023 fixed for the earlier Rs. 7 lakh threshold and Finance Act 2025 carried forward at the new Rs. 12 lakh threshold.

Marginal relief, baked into Section 115BAC(1A), ensures the tax payable shall not exceed the amount by which total income exceeds Rs. 12,00,000.

Total income (Rs.) Slab tax (Rs.) Marginal relief cap (income − 12L) Income-tax payable before cess (Rs.) 12,00,000 60,000 — 0 (rebate) 12,10,000 61,500 10,000 10,000 12,50,000 67,500 50,000 50,000 12,70,000 70,500 70,000 70,000 12,75,000 (approx break-even) 71,250 75,000 71,250 13,00,000 75,000 1,00,000 75,000 (slab tax — relief no longer reduces)Reading the table: Marginal relief stops biting at roughly Rs. 12,75,000 of total income — beyond that, the regular slab tax is already lower than (income − 12L), so you simply pay the slab tax. Below Rs. 12,75,000, your income-tax equals exactly (total income − Rs. 12,00,000). Marginal relief applies only to the income-tax component; health-and-education cess at 4% is added separately on top of the relieved figure.

6. Capital Gains, Lottery, and Other Income Chargeable at Special Rates — The Rebate Exclusion

The single most-asked, most-confused question on Section 87A: can the rebate cancel tax on STCG under Section 111A or LTCG under Section 112A?

The current position implemented in the Income-tax department’s ITR utility (since the 5 July 2024 update for AY 2024-25 onwards) is that the rebate is not allowed against tax on income chargeable at special rates. Section 87A itself does not contain an express exclusion of capital gains or other special-rate income — the department’s stance flows from its reading of Section 115BAC(1A) read with Section 87A, and the matter is presently sub judice before the Bombay High Court. The reasoning the department applies:

- Section 115BAC(1A) charges income at slab rates after segregating income chargeable at special rates under specific provisions.

- The department reads the 87A rebate as applying only to the income-tax payable on income taxed at slab rates. Tax on income chargeable at special rates (computed under Sections 111A, 112, 112A, 115BB, 115BBE, etc.) is added after the rebate.

- Practical impact in the utility: a salaried taxpayer with Rs. 7 lakh salary and Rs. 1 lakh STCG on equity (Section 111A) cannot, under current utility logic, reduce the Rs. 20,000 STCG tax (now 20% for transfers on or after 23 July 2024 per Finance (No. 2) Act 2024) using the Section 87A rebate — even though total income is within the Rs. 12 lakh ceiling.

Special-rate sections you should mentally tag as currently 87A-excluded under the department’s utility view:

Section Income type Rate (post-Budget 2024) 111A STCG on listed equity / equity MF / business trust units (STT-paid) 20% (transfers on / after 23 Jul 2024) 112A LTCG on listed equity / equity MF (STT-paid), exemption up to Rs. 1.25 lakh per year 12.5% (transfers on / after 23 Jul 2024) 112 LTCG on other capital assets (debt MF acquired post Apr 2023, gold, unlisted shares, property) 12.5% without indexation (limited indexation grandfathering for resident individual property bought before 23 Jul 2024) 115BB Lottery, crossword, card games, horse races 30% 115BBE Unexplained income u/s 68 / 69 / 69A / 69B / 69C / 69D 60% (plus surcharge and cess)Important nuance: Where capital gains or other items happen to be taxed at slab rates rather than special rates (for example, debt mutual funds held less than 24 months, where STCG is taxed at slab), that tax is part of the slab-rate computation and can be reduced by the Section 87A rebate. The exclusion bites only where the income falls under a special-rate provision such as Sections 111A, 112, 112A, 115BB or 115BBE.

7. The Bombay HC Interim Order and the July 2024 Utility Change

The 5 July 2024 update to the Income-tax ITR filing utility silently switched off the Section 87A rebate against tax on Section 111A STCG and Section 112A LTCG for AY 2024-25 returns. Many returns filed before that date had claimed the rebate; many filed after were denied it.

The Bombay High Court, hearing The Chamber of Tax Consultants v. Director General of Income Tax (Systems) [WP(L)/35099/2024], passed an interim order on 24 December 2024 directing the department to allow taxpayers to claim the Section 87A rebate on income chargeable at special rates for AY 2024-25 by extending the revised-return / belated-return window and modifying the utility. Subsequent ITR utility updates partially restored the option, but the legal position itself remains contested as of April 2026.

What this means for your AY 2026-27 return:

- If your total income is at or below the Rs. 12 lakh ceiling and you have only income taxed at slab rates, the rebate is automatic — no controversy.

- If you have income chargeable at special rates (e.g., STCG 111A, LTCG 112A) and the utility blocks the rebate, the conservative position is to file in line with the department’s current view. Preserve your right to claim later through a rectification under Section 154 or an appeal once the matter is finally settled.

- Do not file an aggressive return claiming the rebate against tax on income chargeable at special rates without a written legal opinion. Risk of demand under a Section 143(1) intimation, plus interest under Sections 234A / 234B.

8. Eight Worked Examples

All examples assume AY 2026-27 (FY 2025-26), resident individual below 60, default new regime unless stated. Cess of 4% applies on the post-rebate income-tax.

Example 1 — Pure salary, fully within ceiling

Salary Rs. 12,75,000. Standard deduction Rs. 75,000. Total income Rs. 12,00,000. Slab tax Rs. 60,000. Rebate Rs. 60,000. Tax payable: Nil.

Example 2 — Salary just above the marginal-relief band

Salary Rs. 13,75,000. Standard deduction Rs. 75,000. Total income Rs. 13,00,000. Slab tax Rs. 75,000. Income above Rs. 12 lakh is Rs. 1,00,000, which exceeds the slab tax — relief no longer reduces. Tax payable: Rs. 75,000 + 4% cess = Rs. 78,000.

Example 3 — Salary inside the marginal-relief cushion

Salary Rs. 13,25,000. Standard deduction Rs. 75,000. Total income Rs. 12,50,000. Slab tax Rs. 67,500. Marginal-relief cap = Rs. 50,000. Tax payable: Rs. 50,000 + 4% cess = Rs. 52,000.

Example 4 — Salary plus STCG on equity (Section 111A)

Salary Rs. 7,75,000. Standard deduction Rs. 75,000. STCG 111A Rs. 1,00,000. Total income Rs. 8,00,000. Slab tax on (Rs. 8 lakh − Rs. 1 lakh STCG) = Rs. 7,00,000 = Rs. 15,000. STCG tax 20% on Rs. 1 lakh = Rs. 20,000. Rebate available against slab tax only = Rs. 15,000. Tax payable: Rs. 0 (slab) + Rs. 20,000 (STCG) + 4% cess = Rs. 20,800.

Example 5 — Salary plus LTCG on equity above the Rs. 1.25 lakh exemption

Salary Rs. 7,75,000. Standard deduction Rs. 75,000. LTCG 112A gross Rs. 2,25,000; net taxable after Rs. 1.25 lakh exemption = Rs. 1,00,000. Total income Rs. 8,00,000. Slab tax on Rs. 7,00,000 = Rs. 15,000. LTCG tax 12.5% on Rs. 1,00,000 = Rs. 12,500. Rebate against slab tax = Rs. 15,000. Tax payable: Rs. 0 (slab) + Rs. 12,500 (LTCG) + 4% cess = Rs. 13,000.

Example 6 — Senior citizen, old regime

Pension Rs. 5,50,000. Standard deduction Rs. 50,000. Total income Rs. 5,00,000. Slab tax (after Rs. 3 lakh senior basic exemption) = 5% on Rs. 2 lakh = Rs. 10,000. Rebate Rs. 10,000. Tax payable: Nil.

Example 7 — Old regime cliff

Salary Rs. 5,55,000. Standard deduction Rs. 50,000. Total income Rs. 5,05,000 — exceeds the Rs. 5 lakh threshold by Rs. 5,000. Slab tax = 5% on Rs. 2.5 lakh + 20% on Rs. 5,000 = Rs. 12,500 + Rs. 1,000 = Rs. 13,500. No marginal relief in old regime — full tax of Rs. 13,500 + 4% cess = Rs. 14,040. The Rs. 5,000 extra income costs Rs. 14,040 in tax.

Example 8 — NRI

NRI with rental income from India Rs. 8,00,000 (after standard deduction). Total Indian income Rs. 8,00,000. Slab tax under new regime Rs. 30,000 (Rs. 20,000 + Rs. 10,000). No Section 87A rebate — NRIs are not eligible. Tax payable: Rs. 30,000 + 4% cess = Rs. 31,200.

9. Common Mistakes to Avoid

- Assuming the rebate covers capital gains tax. Under the department’s current view it does not. A salaried taxpayer with Rs. 6 lakh salary and Rs. 2 lakh STCG cannot expect zero tax just because total income is Rs. 8 lakh.

- Confusing the standard deduction with the rebate. Standard deduction (Rs. 75,000 new regime, Rs. 50,000 old regime) reduces income; Section 87A reduces tax. Both apply. They are not substitutes.

- Forgetting marginal relief in the new regime. Many taxpayers see income of Rs. 12,40,000 and assume they pay Rs. 66,000 tax. The actual income-tax (with relief) is Rs. 40,000 (cess on top).

- Expecting marginal relief in the old regime. There is none at the Rs. 5 lakh threshold. The old-regime cliff is real.

- HUF claiming Section 87A. The rebate is for resident individuals only. An HUF is a separate person and is not eligible.

- Filing in the wrong regime. Salaried taxpayers without business income can switch every year by simply choosing the regime in the ITR. Those with business income face Form 10-IEA election restrictions — once you opt out of the new regime you can return to it only once in your lifetime.

- Including the rebate when computing advance tax. The rebate reduces final tax payable. Estimate it correctly when computing advance-tax instalments to avoid Sections 234B / 234C interest.

10. FAQ

Q1. I am a salaried employee with total income Rs. 11,80,000. Do I owe any tax under the new regime?

No. Slab tax is Rs. 58,000 (Rs. 20,000 at 5% + Rs. 38,000 at 10%). Rebate equals tax. Tax payable nil. Cess on nil is nil.

Q2. My total income is exactly Rs. 12,00,000. Will I get a tax demand?

No. The rebate ceiling is “up to and including Rs. 12,00,000”. Slab tax Rs. 60,000 is fully cancelled by the rebate.

Q3. I have salary Rs. 11 lakh and LTCG on equity Rs. 50,000 (within the Rs. 1.25 lakh exemption). What is my total income for Section 87A purposes?

LTCG within the Rs. 1.25 lakh per-year exemption under Section 112A is not taxed and is not added to taxable total income. Your taxable total income is Rs. 11 lakh; the rebate works fully on slab tax.

Q4. I had Rs. 10 lakh salary and won Rs. 50,000 in a TV show under Section 115BB. Will the rebate apply to the Rs. 50,000?

No. Section 115BB tax (30% flat = Rs. 15,000) is special-rate and excluded from rebate under the department’s current view. The rebate applies only to slab tax on Rs. 10 lakh.

Q5. I am 65, total income Rs. 4,90,000 (pension + interest). Old regime — how much tax?

Slab tax (after Rs. 3 lakh senior basic exemption) = 5% on Rs. 1,90,000 = Rs. 9,500. Rebate Rs. 9,500. Tax payable nil.

Q6. I’m filing ITR-2 with capital gains. The utility blocks Section 87A on my STCG 111A. What should I do?

File with the department’s restricted view (rebate not on tax for income chargeable at special rates). Note the disallowed amount. If the Bombay HC matter or a subsequent ruling later allows the rebate, file a Section 154 rectification application within four years from the end of the financial year in which the original order was passed, or pursue appeal.

Q7. I have salary of Rs. 11,50,000 and interest income of Rs. 60,000 from FDs. Is the rebate available under the new regime?

Yes. After the Rs. 75,000 standard deduction, your total income is Rs. 11,35,000 — within the Rs. 12 lakh ceiling. Slab tax on Rs. 11,35,000 is Rs. 53,500 (Rs. 20,000 at 5% on the Rs. 4–8 lakh band, plus Rs. 33,500 at 10% on the Rs. 3.35 lakh between Rs. 8 lakh and Rs. 11.35 lakh). The rebate equals the tax, so tax payable is nil. FD interest is taxed at slab rates and is fully covered by the rebate, just like salary.

Q8. I switched from the new regime to the old regime via Form 10-IEA last year (I have business income). Can I switch back this year?

You can return to the new regime once in your lifetime, after which you cannot opt back to the old regime as long as you continue to have business income. Plan the switch carefully — it is generally a one-way door.

11. Legal References

- Section 87A, Income-tax Act, 1961 — the rebate provision.

- Section 115BAC, Income-tax Act, 1961 — new tax regime; Section 115BAC(1A) inserted by Finance Act 2023, amended by Finance Act 2024 and Finance Act 2025.

- Finance Act 2025 — increased new-regime rebate ceiling to total income of Rs. 12,00,000 and rebate to Rs. 60,000; revised slab structure (Rs. 4 lakh basic exemption) for AY 2026-27 onwards.

- Sections 111A, 112, 112A, 115BB, 115BBE, Income-tax Act, 1961 — provisions taxing income at special rates.

- Finance (No. 2) Act 2024 — revised STCG 111A rate to 20% and LTCG 112A rate to 12.5% for transfers on or after 23 July 2024; LTCG 112 rate 12.5% without indexation (limited grandfathering for property held by resident individuals).

- Bombay High Court — The Chamber of Tax Consultants v. Director General of Income Tax (Systems), WP(L)/35099/2024, interim order dated 24 December 2024.

- CBDT Income-tax ITR filing utility update, 5 July 2024 — modification excluded the Section 87A rebate against tax on income chargeable at special rates.

Tax law evolves. Verify the latest CBDT circulars, ITR utility behaviour, and any High Court / Supreme Court order on the Section 87A special-rate matter before finalising your return for AY 2026-27. For a borderline case, consult a practising chartered accountant.

Comments (0)

No comments yet. Be the first to comment!