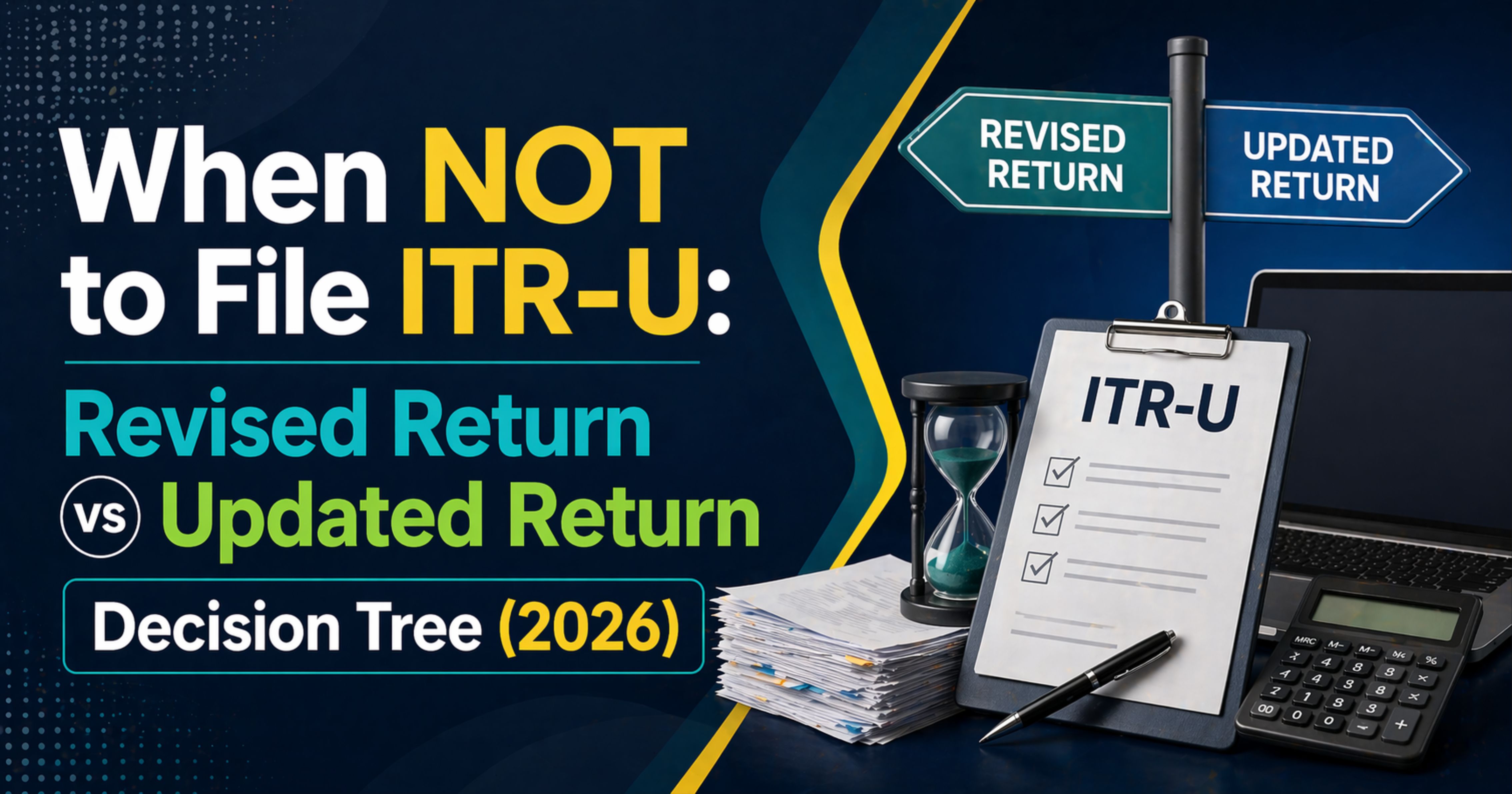

ITR-U under Section 139(8A) is a useful instrument — it fills a genuine gap in the Income-tax Act where a taxpayer realises a disclosure miss after the belated and revised return windows have closed. But it is not always the right instrument, and in several common situations it is either legally unavailable or commercially worse than the alternatives. The one-way nature of ITR-U (additional income only, never a refund, never a loss claim, never a liability reduction) means the wrong choice has no undo button.

This article walks through the decision tree a practitioner should apply before reaching for ITR-U: the 139(5) revised return that is still open, the 139(4) belated return that may still be the better fit, the Section 154 rectification that handles arithmetic errors, the Section 148A interaction that makes proactive ITR-U risky, and the narrow set of cases where doing nothing is the defensible call. For the how-to once ITR-U is the right tool, and the Section 140B arithmetic, read the other two articles in this cluster.

The Decision Tree

Walk through the following questions in order. Stop at the first "yes" that routes you to a tool other than ITR-U.

- Is the original-return deadline under Section 139(1) still open? If yes, file the original return — not ITR-U. There is no updated return until there is something to update.

- Is the revised-return deadline under Section 139(5) still open? The 139(5) window runs up to three months before the end of the relevant AY or before the original return is assessed, whichever is earlier. If you are inside this window, file a revised return — no Section 140B, no slab, no lock-out on refunds / losses / liability reductions.

- Is the belated-return deadline under Section 139(4) still open? The 139(4) window closes the same day as 139(5). If you never filed at all and are inside the window, a belated return under 139(4) attracts Section 234F fee and Section 234A interest but no Section 140B additional tax.

- Is the correction a refund, a loss claim, or a liability reduction? If yes, ITR-U is not available at all. The third and fourth provisos to Section 139(8A) bar any updated return that reduces total tax liability, increases a refund, claims a refund afresh, or declares a loss. These corrections have to be pursued through Section 154 rectification, Section 119(2)(b) condonation, an appellate remedy against a Section 143(1) intimation, or not at all.

- Is the error arithmetic, apparent from the record? If yes, Section 154 rectification is the right tool, not ITR-U. Rectification has no slab, no 48-month cap counted from end of AY, and a two-way door — it can increase or decrease liability.

- Is any proviso to Section 139(8A) triggered? Search / survey / requisition under Sections 132, 132A, 133A; pending or completed assessment, reassessment, recomputation or revision; prosecution initiated under the Act; pending Section 148A notice after the 36-month point — any of these closes the ITR-U door for that AY.

- Is the 48-month cap from the end of the relevant AY already past? If yes, ITR-U is no longer available. The Finance Act 2025 extended the outer window from 24 to 48 months effective 1 April 2025, but 48 months is the hard stop.

If you have walked past every "yes" above and still have a situation that is additional income on a closed year with no provisos triggered and within 48 months — ITR-U is the right tool, and the Section 140B ladder is the cost of using it. Otherwise, one of the alternatives below fits better.

Revised Return (139(5)) vs ITR-U (139(8A))

A side-by-side:

- Window. 139(5): up to three months before end of AY, or pre-assessment, whichever earlier. 139(8A): after the 139(4) / 139(5) window closes, up to 48 months from end of AY.

- What's allowed. 139(5): any correction — including refunds, losses, liability reductions. 139(8A): additional income only; no refunds, no losses, no liability reductions.

- Additional tax. 139(5): none (normal interest under 234B / 234C on any additional tax). 139(8A): Section 140B at 25 / 50 / 60 / 70% on the aggregate of tax + interest + fee.

- Who can file. 139(5): anyone who filed under 139(1) or 139(4). 139(8A): anyone — including taxpayers who never filed at all for that AY, as long as the 139(8A) provisos don't bar them.

- Frequency. 139(5): multiple revisions permitted within the window. 139(8A): one updated return per AY, full stop.

If 139(5) is still open for the AY in question, it is almost always the better option. The cost is lower, the scope is wider, and there is no slab.

Belated Return (139(4)) vs ITR-U (139(8A))

For taxpayers who never filed the original return:

- Window. 139(4): up to three months before end of AY, or pre-assessment, whichever earlier (same as 139(5)). 139(8A): picks up after 139(4) closes.

- Fee and interest. 139(4): Section 234F fee (Rs. 1,000 or Rs. 5,000 by income level) and Section 234A interest on any unpaid tax. 139(8A): same 234F + 234A on the base, plus Section 140B on top.

- Limitations. 139(4) accepts any kind of return — including loss and refund claims, within its rules. 139(8A) is the same one-way street as above.

A non-filer who realises the miss while 139(4) is still open should file belated, even if the fee stings. ITR-U layered on the same facts adds the 140B slab unnecessarily.

Section 154 Rectification — The Quiet Workhorse

A surprising share of "I need to file ITR-U" situations are actually Section 154 situations. Section 154 permits the rectification of any mistake apparent from the record — arithmetic errors, wrong application of a section, TDS credits mismatched with Form 26AS, a rate of tax picked incorrectly, and so on. Key differences from ITR-U:

- Rectification is two-way — it can reduce or increase liability.

- No Section 140B, no slab, no four-bucket ladder.

- The time bar is four years from the end of the financial year in which the order sought to be rectified was passed — a different clock from 139(8A)'s 48 months from end of AY.

- The trigger is a Section 143(1) intimation or other order that contains the mistake — if you just realised you made the mistake in your original return with no intimation in play, rectification is usually not the right channel.

If the mistake is an obvious arithmetic slip or a TDS-credit mismatch visible on comparing the intimation with Form 26AS, file a rectification request on the e-filing portal against the specific order. ITR-U is a heavier instrument meant for disclosure of additional income, not for correcting an arithmetic error the Department can see on the record.

Section 148A Notice — Why Proactive ITR-U Can Hurt

Section 148A is the procedure the Department now follows before issuing a Section 148 notice for reassessment: it asks the taxpayer to explain why a notice should not be issued, based on information suggesting escaped income. When a 148A notice is already in play, filing an ITR-U proactively can convert a defendable position into an admission.

- The ITR-U is a voluntary disclosure. Once filed, it locks in the additional income as conceded.

- If the 148A information was weak and a well-prepared reply could have defused the notice, you have given up that defence and paid the 140B slab as well.

- If the AY is past the 36-month point, a 148A notice can itself shut the ITR-U door under proviso (d) to Section 139(8A) — the timing interplay matters.

The right order of operations is: get the 148A letter, evaluate the underlying information, reply on the merits, and only pursue ITR-U if the facts force a disclosure. Do not reflexively reach for ITR-U the moment a 148A notice lands.

When Doing Nothing Is the Right Call

A final category: the miss is small, the AY is old, and the provisos or cost profile make ITR-U a poor fit. In these cases "do nothing now, prepare for a potential query later" is a legitimate choice — not a lazy one.

- Small rupee amount, old AY. If the under-reported tax is modest and the AY is in bucket 4 with 234B interest accrued for three or four years, the combined cost may exceed the risk-weighted expected cost of a Section 148A notice that may never come. Keep the workpapers ready; if a notice lands, respond on the merits then.

- AY past the 48-month window. ITR-U is not available. Preserve the records in case the Department reopens under Section 148 within its own time limits, which differ from 139(8A).

- AY already under assessment. Proviso bar applies; engage with the assessment officer in the assessment itself, not via ITR-U.

"Do nothing" is a decision, not a default. Document the reasoning, keep the supporting computations, and revisit the position if facts change — a partner's share being traced through a survey, for instance, may flip the calculus.

FAQ

I realised a mistake a week after filing the original return — should I file ITR-U? No. If the revised-return window under Section 139(5) is still open, file a revised return. ITR-U is for situations where 139(5) has closed.

I forgot to claim a deduction — can ITR-U add it? No. ITR-U cannot reduce tax liability, so a forgotten deduction cannot be added through an updated return. Check whether Section 154 rectification applies; if the original return has been assessed and the miss is apparent from the record, rectification may work. Otherwise the deduction is lost.

Can I file ITR-U just to update some non-income fields (address, bank account)? No. ITR-U is a tool for income and tax corrections. Non-income fields are updated through the profile section of the e-filing portal, not through a return.

The additional tax due is zero after TDS credits — can I still file ITR-U to correct the disclosure? ITR-U is meant for situations where additional tax is payable. If TDS credits cover the full liability and there is no additional tax, the update rarely changes anything substantive at CPC. Check Part B-ATI carefully — the Section 140B slab is 25% of a non-zero base, and a truly zero base is unusual once 234B and 234F are factored in.

A 148A notice just arrived — should I file ITR-U immediately? No. Evaluate the information cited in the notice, prepare a reply on the merits, and only move to ITR-U if the facts force a disclosure. Proactive ITR-U in the face of a 148A notice is often premature.

Next Steps

If you have walked the decision tree and ITR-U is the right tool, the step-by-step how-to article in this cluster covers the mechanical filing process. If the Section 140B cost is the open question, the penalty-ladder article works through the slab arithmetic and three worked examples. And if the underlying 48-month amendment and its transition mechanics are what you need, the main hub explainer is the place to start.

Comments (0)

No comments yet. Be the first to comment!