A Four-Year Second Chance, With a Twist

The quiet doubling of the ITR-U window from 24 months to 48 months is a bigger shift than the headline suggests. On paper, a taxpayer who missed reporting income, mis-classified a capital gain, or forgot a foreign interest credit now has four full years from the end of the relevant assessment year to come clean under Section 139(8A) of the Income-tax Act, 1961. In practice, the longer window comes with a steeper additional-tax ladder, an unchanged set of eligibility bars, and a very specific set of things an updated return still cannot do. This article walks through what actually changed, the new Section 140B rate card with a worked example, the provisos that close the door, and the narrow but real situations where voluntary correction still makes commercial sense.

What Changed, and When It Applies From

Finance Act 2025 amended Section 139(8A) to extend the time limit for furnishing an updated return from 24 months to 48 months from the end of the relevant assessment year. The amendment is effective from 1 April 2025. For assessment year 2025-26, that means the outer deadline for an ITR-U is now 31 March 2030 rather than 31 March 2028.

The CBDT has separately notified an updated ITR-U form to reflect the longer window and the revised additional-tax slabs. Practitioners should rely on the form, instructions and any accompanying circular in their current text at the time of filing; the form has been amended multiple times since ITR-U was first introduced and specifics like schedules, declarations and reason codes do change.

One timing nuance worth holding on to. Under the old 24-month rule, AY 2021-22 would have expired on 31 March 2024 — its outer ITR-U window had closed well before the 1 April 2025 amendment. After the amendment, the Department has indicated that AY 2021-22 through AY 2024-25 can be updated within the 48-month window during FY 2025-26, subject to the eligibility bars in Section 139(8A). If you are advising on an AY that straddles the transition, read the section as it stood on the date the taxpayer is actually filing, and not as it read when ITR-U was first introduced.

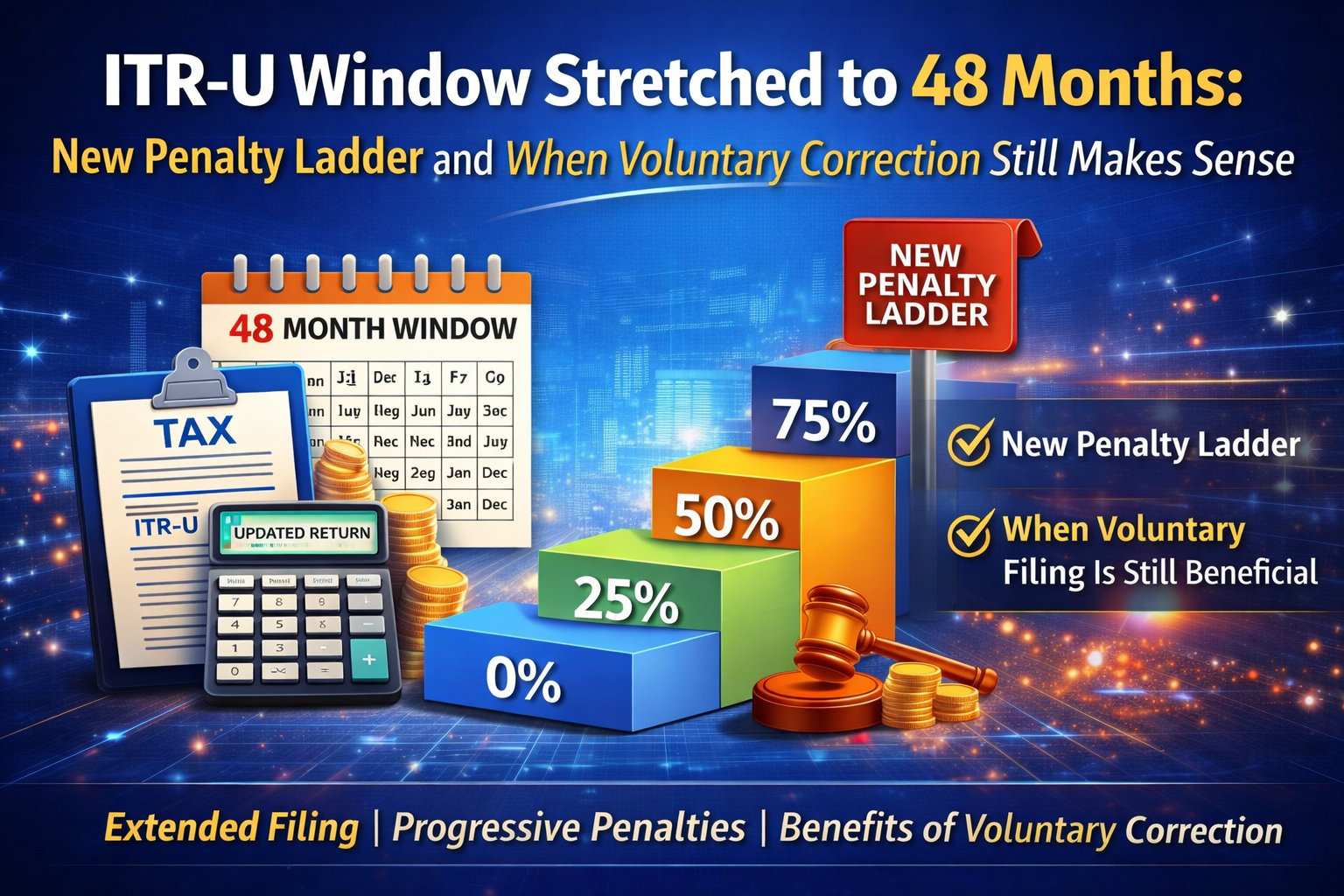

The New Additional-Tax Ladder Under Section 140B

The commercial heart of the change is the Section 140B rate card, which determines the additional tax payable on top of the normal tax and interest when an ITR-U is filed. Post-Finance Act 2025 the ladder reads as follows:

- Within 12 months from the end of the relevant assessment year: additional tax of 25% of the aggregate of tax and interest.

- After 12 months, within 24 months: additional tax of 50%.

- After 24 months, within 36 months: additional tax of 60%.

- After 36 months, within 48 months: additional tax of 70%.

The 60% and 70% slabs are new; under the earlier two-year regime, only the 25% and 50% steps existed. The effective cost of waiting is now significantly higher in years three and four.

A Worked Example at the 30% Slab

Suppose an individual taxpayer, taxed at the 30% marginal rate, omitted Rs. 10,00,000 of additional taxable income for an assessment year. Ignoring surcharge and cess for simplicity and using indicative numbers:

- Basic tax at 30%: Rs. 3,00,000.

- Interest under Sections 234A/234B/234C, say, roughly Rs. 60,000 depending on the months of delay.

- Aggregate of tax and interest: about Rs. 3,60,000.

Filed within 12 months, additional tax at 25% is roughly Rs. 90,000, so the total payout is in the region of Rs. 4,50,000. Filed in the 36 to 48 month bucket, additional tax at 70% is roughly Rs. 2,52,000, and the total payout is in the region of Rs. 6,12,000. The taxpayer is paying the same underlying tax, but the cost of the time value plus the penalty-in-substance is meaningfully larger. These numbers are rounded and illustrative, not a computation for any specific facts; actual calculations must apply the relevant slab, surcharge, cess and 234A/B/C interest as they stand for the year in question.

What ITR-U Still Cannot Do

The longer window does not expand the scope of what an updated return is allowed to achieve. Section 139(8A) continues to bar the use of ITR-U to:

- Claim a refund, or increase a refund already claimed in the original, belated or revised return.

- Reduce the total tax liability disclosed in the earlier return.

- Declare a loss, or convert an income return into a loss return.

ITR-U is, in structure, a one-way street: it is available for disclosing more income and paying more tax, not for fixing a situation in the taxpayer's favour. A taxpayer who genuinely needs to reduce liability, correct a wrongly denied refund, or carry forward a loss will usually need to look at a revised return under Section 139(5), a rectification under Section 154, or a condonation application under Section 119(2)(b), depending on the stage.

When the Door Is Closed: The Section 139(8A) Provisos

The provisos to Section 139(8A) bar an updated return in a series of situations. In broad terms, the route is not available where, for the relevant assessment year — and in some cases for preceding assessment years as well — any of the following applies:

- A search has been initiated against the assessee under Section 132, or books, documents or assets have been requisitioned under Section 132A. The bar attaches to the AY of the search or requisition and, read with the related provisos, to preceding assessment years covered by that action.

- A survey has been conducted under Section 133A (with limited carve-outs in that section itself), again with the bar extending to the AY of the survey and preceding AYs within the scope of the proviso.

- A search or requisition on another person under Section 132 or 132A has been initiated that relates to the assessee.

- Assessment, reassessment, recomputation or revision proceedings are pending or have been completed for that AY — it is the fact of pendency or completion that triggers the bar, not the mere issuance of a notice.

- Prosecution proceedings under the Act have been initiated for the relevant year.

- A prior ITR-U has already been furnished by the assessee for the same AY.

- Information is available with the assessing officer under specified laws — including exchange-of-information provisions and agreements under Section 90 or Section 90A — and has been communicated to the assessee; or the assessee is a person notified in this regard.

There is also a specific bar linked to Section 148A: where a show-cause notice under Section 148A has been issued after the 36-month point in the assessment-year timeline, the ITR-U route for that year can be closed even though the 48-month clock has not run out, subject to the carve-out in Section 148A(3). The exact text of the provisos has been amended more than once since 2022; before advising a client to file, read the section as it stands and map each proviso to the facts of the year.

When Voluntary Correction Still Makes Commercial Sense

Given the 60% and 70% slabs, when is an ITR-U still worth filing rather than waiting to see if a notice arrives? A few situations where the numbers tend to favour voluntary correction:

- Mismatches already visible in AIS/TIS. Where the omission corresponds to data the department already has through SFT, TDS, or reporting entities, the probability of a notice is high and the cost of contesting it usually exceeds the 140B additional tax.

- Section 270A misreporting exposure. Where the conduct risks being characterised as misreporting, penalty under Section 270A can go up to 200% of the tax on under-reported income, and prosecution under Section 276C is at least theoretically on the table. Against that backdrop, a 25% or 50% ladder is a cheaper outcome.

- Early-slab disclosures. Within 12 months, the 25% additional tax is the lowest-friction way to clean up a genuine omission and stop interest from compounding.

- Pre-transaction cleanups. Taxpayers preparing for a bank borrowing, an exit, due diligence in a sale, or an immigration filing often need a clean tax record more than they need to optimise the last rupee of liability; ITR-U is a defensible way to regularise historical gaps.

Conversely, at the 60% or 70% slab, the commercial case is tighter. The comparison should be honest about the likelihood of detection, the Section 270A exposure on the specific facts, and whether the eligibility bars in Section 139(8A) are even satisfied for the year in question.

Practitioner Checklist

- Run the eligibility pre-check first. Map each proviso to Section 139(8A) against the year. Has there been a search, survey, pending assessment, reassessment notice, or prosecution proceeding? If yes, the ITR-U route may be closed for that year.

- Confirm the slab that applies. Identify the end of the relevant assessment year, count months to the intended filing date, and lock the 25/50/60/70% bucket before discussing numbers with the client.

- Verify that the filing actually increases tax. An ITR-U that reduces liability, increases a refund, or declares a loss is not permitted. If the working shows a lower number, the route is wrong.

- Reconcile against AIS, TIS and 26AS. The quality of an updated return is only as good as the data it sits on. Pull the full AIS/TIS and 26AS for the year before finalising the schedule.

- Compute interest under 234A/234B/234C cleanly. The 140B additional tax sits on top of tax and interest, so a sloppy interest calculation snowballs into a sloppy additional-tax number.

- Document the reason for the update. The ITR-U form requires a reason code and brief rationale. Keep a working paper tying the reason to underlying records in case questions follow.

- Get client sign-off on the commercial trade-off. Particularly at the 60% and 70% slabs, the client should explicitly approve the voluntary route versus the wait-and-see alternative, on a written note.

- Do not rely on the filing to close exposure beyond what it covers. An ITR-U regularises the tax on the disclosed income. It does not, by itself, foreclose a survey, search or reassessment on unrelated issues.

Closing Note

The 48-month window is a genuine expansion of taxpayer options, but it is not a free pass. The new 60% and 70% slabs mean that waiting has a price, the provisos mean that the door is often not as open as it looks, and the structural bar on reducing liability or declaring a loss means that ITR-U cannot fix every problem. Treat the extension as a disciplined compliance tool for a specific category of errors — honest omissions that match data the department already has — rather than a universal safety net. Where it fits, file early in the ladder. Where it does not fit, advise the client in writing on why, and move the conversation to the right section.

Comments (0)

No comments yet. Be the first to comment!