The single most-asked question after a client decides to file an ITR-U is: what will it actually cost? Section 140B of the Income-tax Act, 1961 is where that cost is defined. It is not a penalty in the classical sense — it is additional income-tax payable as the price of using the updated-return route under Section 139(8A). The amount is not discretionary, not appealable and not waivable. The only lever you control is timing, because the rate climbs in four steps across the 48-month window.

This piece walks through the four slabs, the base the percentage is applied to (which is where most spreadsheet errors live), three worked examples covering the first bucket, the last bucket and a compounding-interest edge case, the challan 280 heads to use, and the narrow set of situations where the arithmetic says you should not file at all. For the mechanical filing steps, read the step-by-step how-to article. For the policy background and the 48-month amendment itself, read the main hub explainer.

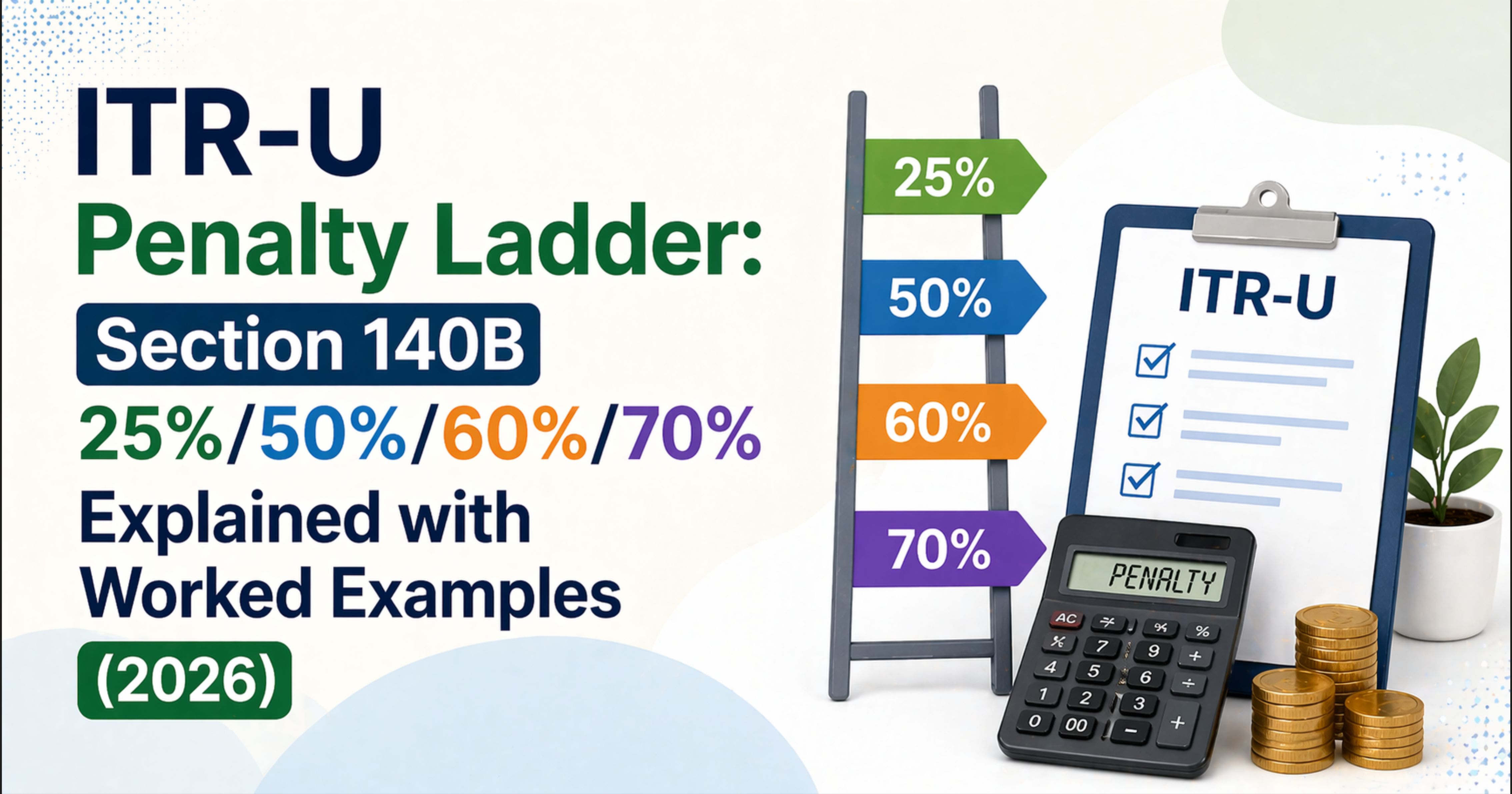

The Four Buckets: Rate, Window, Trigger

Section 140B scales the additional tax by how late the ITR-U is filed, measured from the end of the relevant assessment year. The relevant AY is the AY whose income is being updated, not the AY in which you are sitting. For the year ending 31 March 2024 (AY 2024-25), the end-of-AY clock starts on 31 March 2025.

- Bucket 1 — 25%: ITR-U filed after the belated / revised return window under Sections 139(4) and 139(5) has closed, but within 12 months from the end of the relevant AY.

- Bucket 2 — 50%: Filed after 12 months, within 24 months.

- Bucket 3 — 60%: Filed after 24 months, within 36 months. This slab and the next were inserted by the Finance Act 2025 amendment.

- Bucket 4 — 70%: Filed after 36 months, within 48 months. The outer bound — no ITR-U after this.

The bucket is fixed by the date of filing, not the date of payment and not the date of the original mistake. Filing on 15 April 2026 for AY 2024-25 crosses into bucket 2 (the end of AY 2024-25 is 31 March 2025, and 15 April 2026 is more than 12 months later). A filing plan that slips a few days across a bucket boundary can cost an extra 10 or 25 percentage points on the entire base.

The Base: What the Percentage Is Multiplied By

The 25 / 50 / 60 / 70% is not applied to the additional income, and it is not applied only to the extra tax. The base is computed through Part B-ATI of the notified ITR-U form, and it is a composite figure. Walked as a plain-English sequence:

- Start with tax on the updated total income under the regime (old or new) that applies for that AY.

- Add interest under Sections 234A, 234B and 234C computed on the updated figures, not the original ones.

- Add the late-filing fee under Section 234F where applicable (one-thousand or five-thousand rupees depending on income).

- Add any regular-assessment tax already determined for that year (for example, a Section 143(1) intimation that increased the liability).

- Subtract taxes already paid — TDS, TCS, advance tax and self-assessment tax — as credited in the earlier return or otherwise available on the portal.

- Adjust for any refund already claimed or issued in the earlier return. A refund that was claimed or issued is treated as a reduction in taxes-already-paid, which increases the base on which the 140B percentage is applied. This is the single line that surprises practitioners most often.

The figure produced by that sequence is the base. Section 140B additional tax is that base multiplied by the slab percentage for the month of filing. Critically, Section 140B is not charged on the Section 140B amount itself — the additional tax does not compound on the additional tax.

The total payable is the base plus the Section 140B amount. That combined figure is what must sit in challan 280 before you upload the JSON — not the base alone.

Worked Example 1 — Bucket 1 (25%), Small Straightforward Miss

A salaried client filed ITR-1 for AY 2025-26 in July 2025. In January 2026 they realise a freelance invoice of Rs. 2,00,000 was not reported in Other Sources. The missed income pushes taxable income from Rs. 9,00,000 (old regime) to Rs. 11,00,000. Slab tax on the additional Rs. 2,00,000 (old regime, no 87A rebate at this level) is Rs. 60,000 plus cess of Rs. 2,400. There are no interest figures to speak of because the miss is being caught inside the 12-month window and advance-tax exposure is limited.

- Additional tax on revised income (old regime, 30% slab + 4% cess): Rs. 62,400.

- Interest under 234B / 234C on the additional tax, approx 8 months to date of filing: Rs. 3,744.

- Section 234F fee: not applicable (original return was on time).

- Base for Section 140B: Rs. 62,400 + Rs. 3,744 = Rs. 66,144.

- Section 140B additional tax at 25%: Rs. 16,536.

- Total paid through challan 280: Rs. 82,680.

The client is out Rs. 16,536 for the Section 140B layer over what a revised return would have cost them if they had caught it by 31 December 2025 — a cost that doubles if the filing slips past 31 March 2026 into bucket 2.

Worked Example 2 — Bucket 4 (70%), Same Income, Very Late

Same Rs. 2,00,000 miss, but this time on AY 2022-23, discovered only now (February 2026). The end of AY 2022-23 was 31 March 2023; filing today falls in the 35-to-48-month window, bucket 4, 70% slab.

- Additional tax on revised income (old regime, 30% slab + 4% cess): Rs. 62,400 (same as above).

- Interest under 234B / 234C on the additional tax, approx 35 months from 1 April 2022 to February 2026 at 1% per month: ~Rs. 21,840.

- Section 234F fee: check if the original return was belated and a fee was already applied; if not, Rs. 5,000 applies here (income above Rs. 5,00,000).

- Base for Section 140B: Rs. 62,400 + Rs. 21,840 + Rs. 5,000 = Rs. 89,240.

- Section 140B additional tax at 70%: Rs. 62,468.

- Total paid through challan 280: Rs. 1,51,708.

The same Rs. 2,00,000 miss now costs the client Rs. 1,51,708 — nearly eighty per cent more than bucket 1. The extra Rs. 45,932 versus Example 1 comes from Section 140B at 70% instead of 25% (Rs. 45,932) and 234B interest accruing across 35 months. If the original return had claimed a refund that was issued, the base would go up further because the refund would reduce the credit for taxes-already-paid in the Part B-ATI computation.

Worked Example 3 — When 234B Compounding Balloons the Base

The trap in bucket 4 is not the 70% slab by itself — it is how Section 234B interest compounds on a large under-reported tax liability across four years. Consider a business client whose original return for AY 2022-23 missed Rs. 20,00,000 of capital gains, tax Rs. 4,00,000 plus cess Rs. 16,000.

- Additional tax on revised income: Rs. 4,16,000.

- Interest under 234B (1% per month) from April 2022 to February 2026 — approx 46 months: ~Rs. 1,91,360.

- Interest under 234A from the original due date to filing: further layer, depending on whether the original return was filed.

- Section 234F fee: Rs. 5,000 if applicable.

- Base for Section 140B: Rs. 4,16,000 + Rs. 1,91,360 + Rs. 5,000 = approx Rs. 6,12,360.

- Section 140B additional tax at 70%: Rs. 4,28,652.

- Total payable (before any TDS credit): approx Rs. 10,41,012 on an under-reported income of Rs. 20,00,000.

At this scale the combined tax-plus-interest-plus-140B layer exceeds half the under-reported income. The right question is not "can we file?" but "do the facts support a voluntary disclosure now, or is there a proviso issue that changes the answer?" — revisit the hub article's eligibility bars before paying.

When the Math Stops Making Sense

Section 140B is designed so that voluntary disclosure remains rational for taxpayers who want to close the matter. For small misses caught early, the slab is light and the arithmetic works. For very old, very large misses, the arithmetic can flip — especially when 234B has been running at 1% per month for three or four years. The tipping points are:

- Small, very old miss. If the under-reported tax is modest and the miss is in bucket 4, the 70% slab on a small base is an absolute amount the client can absorb, and filing is still usually the right call.

- Large, very old miss with heavy 234B exposure. Combined tax + 234B + 140B can approach or exceed the under-reported income itself. The voluntary-disclosure case gets thinner; the alternative (doing nothing and relying on statute-of-limitation arguments if the Department eventually issues Section 148A) is not costless either, but the trade-off is now a real decision rather than a reflex.

- Anything in an AY that is already under assessment or proceeding. ITR-U is barred by proviso in these cases — the 140B arithmetic is moot.

The decision of whether to file at all (as opposed to how much it will cost) is the subject of the next article in this cluster.

How to Pay — Challan 280 Heads

The total Section 140B amount plus the base is paid through challan 280 (ITNS 280) on the e-filing portal. The fields that matter:

- Tax applicable: (0021) Income Tax (Other than Companies) for individuals, HUFs, firms, LLPs and AOPs. Companies use (0020).

- Type of Payment: (300) Self-Assessment Tax. Do NOT use (400) Tax on Regular Assessment — that is for demand-based payments, not voluntary disclosure.

- Assessment Year — pick the AY whose income you are updating, not the AY of filing. A wrong AY on the challan is the single most common cause of ITR-U validation failure.

- Amount split: enter tax, surcharge, cess, interest, fee (234F) and "others" in their respective fields. Section 140B additional tax is entered under "others". The portal totals these and posts the consolidated figure.

- BSR code, challan serial number, date and amount — capture these four from the counterfoil and enter them in the ITR-U schedule before generating the final JSON.

Pay the full amount before you upload the JSON. A short-paid challan 280 will not validate against the computed liability in Part B-ATI, and the return will reject.

FAQ

Is Section 140B the only additional levy? Yes, for ITR-U itself. Section 234F (fee) and Sections 234A / 234B / 234C (interest) are part of the base on which the 140B percentage is applied, so you pay them once and the 140B slab applies on top.

Can I pay the Section 140B amount in instalments? No. The full challan 280 — base plus Section 140B additional tax — must be paid before the ITR-U is uploaded. Instalment facilities under the Income-tax Act do not apply to self-assessment tax on an updated return.

What if I miscalculate the Section 140B amount? If you under-pay, the return will either not validate at upload or will attract a Section 143(1) intimation raising a demand with interest. If you over-pay, the excess is refunded on processing, subject to the general refund workflow. Accuracy matters — re-walk Part B-ATI before you pay.

Does the 140B slab reset if I file a second ITR-U? You cannot file a second ITR-U for the same AY. Section 139(8A) permits one updated return per AY, and the slab is fixed by the single filing date.

Is Section 140B charged on the Section 140B amount itself? No. The percentage is applied to the Part B-ATI base (tax + interest + fee + regular-assessment tax, less credits). The 140B amount is not itself part of that base, so it does not compound.

Next Steps

If the arithmetic above supports filing, move to the step-by-step how-to article in this cluster — it walks through the utility, Part A reason codes, Part B head-wise adjustment, challan 280 payment and verification. If the arithmetic is giving you pause, or if you are unsure whether ITR-U is the right route at all versus a revised return, a rectification or doing nothing, read the decision-tree piece next. And if you need the policy background on why the 48-month window exists and how it was extended by the Finance Act 2025, read the main hub article.

Comments (0)

No comments yet. Be the first to comment!