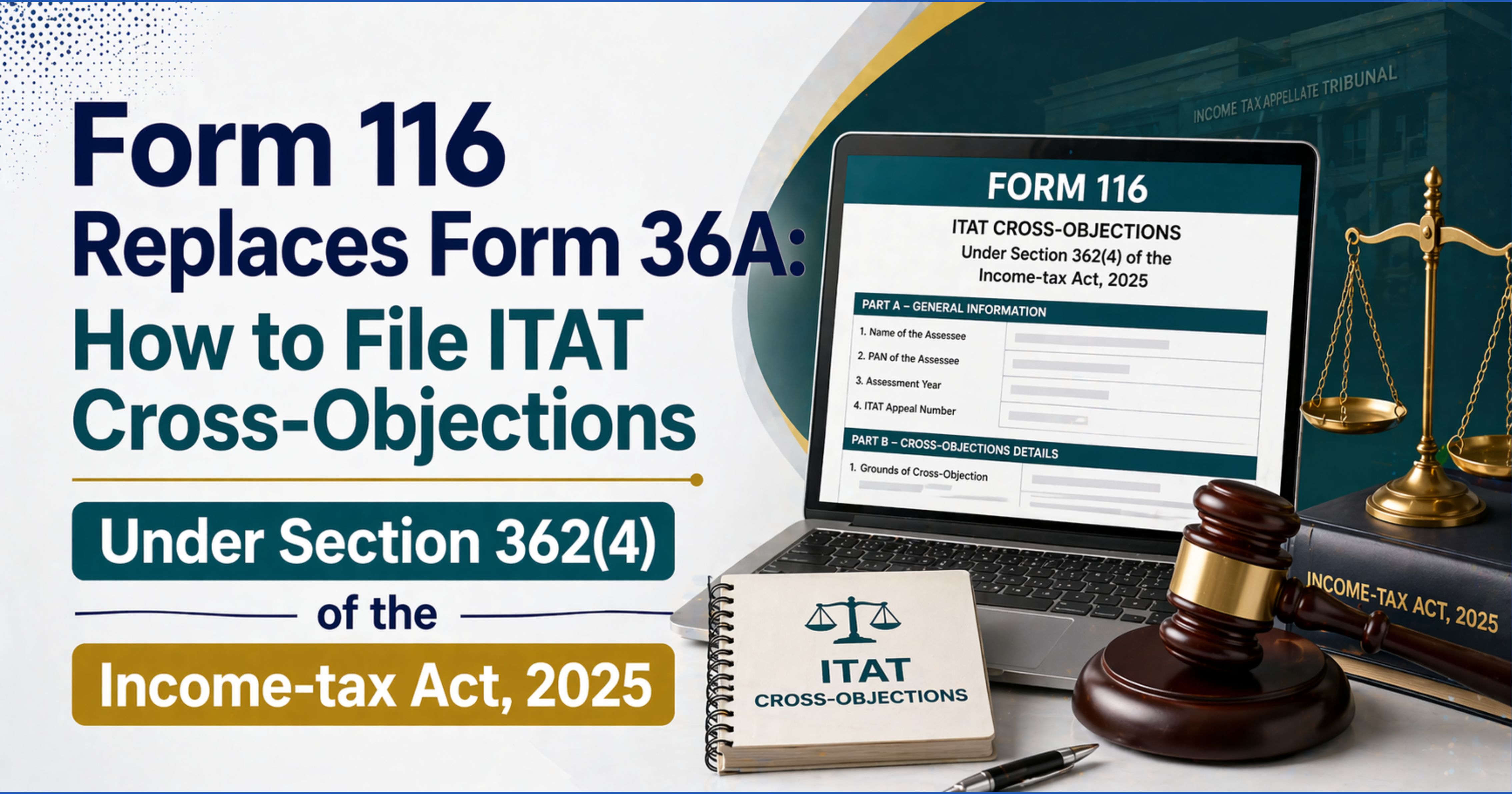

The Quiet Death of Form 36A

For decades, a respondent in an Income Tax Appellate Tribunal proceeding who did not want to file an independent appeal but did want to push back on specific findings had exactly one instrument: Form 36A, prescribed under Rule 47 of the Income-tax Rules, 1962. With the commencement of the Income-tax Act, 2025 on 1 April 2026 and the corresponding Income-tax Rules, 2026, that form has been retired. In its place, Form 116 — a memorandum of cross-objections under Section 362(4) of the new Act, read with Rule 193(2) of the new Rules — is now the prescribed instrument by which a respondent can be heard on adverse grounds without filing a fresh appeal. The CBDT’s recently published FAQs and Guidance Note on Form 116 settle most of the procedural questions practitioners had been asking since the draft Rules were released in February 2026. This note walks through what the form is, who may file it, the 30-day window that decides whether your client’s objections are on the record, and the procedural corners that turn a clean cross-objection into a defective filing.

Statutory Architecture: Section 362(4) and Rule 193(2)

Section 362 of the Income-tax Act, 2025 is the operative provision for appeals to the Appellate Tribunal. Sub-sections (1) and (2) deal with the right of appeal of the assessee and of the Principal Commissioner or Commissioner respectively. Sub-section (4) is the cross-objection provision: where an appeal under sub-section (1) or (2) has been filed and notice of that appeal has been served on the other side, that other side — the respondent — may, within 30 days of receipt of the notice, file a memorandum of cross-objections against any part of the order appealed against. The cross-objection is then disposed of by the Tribunal as if it were an appeal presented within the time prescribed for the appeal itself.

Rule 193 of the Income-tax Rules, 2026 prescribes the form. Rule 193(1) prescribes Form 115 for the principal appeal under Section 362(1) or (2), replacing Form 36 of the 1962 Rules. Rule 193(2) prescribes Form 116 for the cross-objection under Section 362(4), replacing Form 36A. For assessee-filed cross-objections, the form and the verification are to be signed by the person specified in Rule 167(3) — broadly, the same set of authorised signatories who sign the return of income (self for individuals, karta for HUF, managing director or authorised director for companies, designated partner for LLPs, principal officer for local authorities, and so on). Where an authorised representative is involved, the FAQ contemplates appropriate authorisation; practitioners should confirm the applicable signing rule for their specific category of respondent before filing rather than assuming a single signing rule applies uniformly across every scenario.

Who May File a Cross-Objection

The CBDT FAQ confirms what the statute already implies: any respondent to an ITAT appeal may file Form 116. In practice this covers three categories:

- The assessee, when the Department is the appellant. This is by far the most common scenario — CIT(A) decides part for the assessee and part for the Department, the Department appeals the part it lost, and the assessee files a cross-objection on the part the assessee lost rather than running a parallel appeal.

- The Income Tax Department (Principal Commissioner or Commissioner), when the assessee is the appellant. Symmetrical situation: the Department uses Form 116 to defend its losses on adverse grounds without filing a separate Section 362(2) appeal.

- Government deductors who are respondents in TDS-related appeals before ITAT.

Filing Form 116 is optional, not mandatory. A respondent who is content to defend the impugned order as it stands, or who is willing to lose specific grounds in exchange for not opening up the proceeding, may simply file a reply. The cross-objection is the instrument for actively challenging adverse findings within the same proceeding.

The 30-Day Window: Where Most Cross-Objections Die

Section 362(4) gives the respondent 30 days from the date of receipt of the notice of appeal to file Form 116. The clock runs from service of the notice on the respondent, not from the date the Department actually filed its Form 115, and not from the date the appeal was admitted. This is the single most common reason cross-objections fail at the threshold.

The Tribunal does have power to admit a cross-objection filed beyond 30 days if it is satisfied that there was sufficient cause for the delay, and the form itself contemplates an attached delay-condonation statement. But condonation is discretionary, requires a properly drafted petition with affidavit-grade reasons, and is not a substitute for filing on time. Where the respondent is the assessee, a missed 30-day window typically means the adverse findings of CIT(A) become final at the ITAT level and travel into any future High Court reference under Section 365 only as the appellant’s grounds, not the respondent’s.

As a practice point — not a rule of law — practitioners should diary the receipt date of the notice the moment it lands (whether by ITAT portal alert, registered post, or e-mail through the Faceless Appeal channel) and treat day 25 as the internal deadline rather than day 30. Leaving a buffer absorbs the workflow frictions that routinely consume the last three days of a limitation window.

Inside the Form: Parts A to F plus Verification

Form 116, as notified, is structured into six parts followed by a verification clause. The CBDT Guidance Note sets out the broad architecture:

- Part A — Appellant details: name, PAN/TAN, address, status (individual, HUF, company, etc.), and the role in which the appellant is before the Tribunal.

- Part B — Respondent details (the cross-objector): corresponding particulars for the party filing Form 116. This is where authorised representative details and the e-Filing portal credentials are linked to the filing.

- Part C — Appeal / cross-objection particulars: the order being appealed against (date, authority, and DIN of the CIT(A) order under the new framework), the date the order was communicated, the date the original appeal in Form 115 was filed, and the appeal number assigned by the Tribunal.

- Part D — Amount disputed / tax effect: the heads of additions, disallowances, or reliefs in dispute, with the tax effect of each. Where multiple assessment years are involved, each year is shown separately.

- Part E — Cross-objection filing details: information relating to the filing of the cross-objection itself, as set out in the notified form.

- Part F — Further related information: residual filing particulars as required by the notified form.

The grounds of cross-objection, numbered and tied to specific adverse findings of CIT(A) with tax effect attributable to each, are incorporated within the form as prescribed. The CBDT FAQ confirms that multiple grounds are permitted and additional rows may be added as required. Grounds should be drafted as concise propositions of law and fact, not as argument — the argument belongs in the written submissions filed later.

The verification clause requires the authorised signatory to confirm the truth of the contents and the authority to sign, dated and signed in the manner prescribed by the e-Filing workflow. Because the exact field layout of Parts E and F has procedural consequences, practitioners should refer to the notified form and the CBDT Guidance Note when preparing the draft rather than relying solely on secondary summaries.

Documents That Must Travel With Form 116

The CBDT FAQ and the form itself contemplate the following enclosures:

- A copy of the order being appealed against — typically the CIT(A) order or, in some categories, an order of the Assessing Officer or Principal Commissioner.

- A copy of the original appeal in Form 115 filed by the appellant, as served on the respondent.

- Supporting documents relevant to the grounds of cross-objection — for example, the assessment order, audit reports, and any documentary evidence that was on record before CIT(A) and is being relied upon at the ITAT stage.

- A delay condonation statement, where Form 116 is being filed beyond the 30-day window. This should set out the date of receipt of the notice, the reason for the delay, and the date on which the cause for delay ceased to operate.

Practically, filing now operates through the ITAT e-filing portal, and practitioners should rely on the portal-generated acknowledgement as proof of filing. Where any bench is still accepting physical filings under transitional advisories, that route is the exception rather than the rule and should be confirmed with the registry of the bench seised of the appeal before being attempted.

Procedural Rules That Catch First-Time Filers

Three rules in the CBDT FAQ deserve particular attention because they reverse what was permissible under the 1962 framework:

- No revision once filed. Per the FAQ, Form 116 cannot be revised after submission. Errors in the grounds or the disputed amounts can only be corrected by way of a separate application for amendment, which is at the discretion of the Tribunal and is not a substitute for getting the filing right the first time. Practitioners should treat the cross-objection as a final pleading, not a draft.

- E-filing is the operating route. The Form 116 workflow is live on the ITAT e-Filing portal and the filing is evidenced by the portal-generated acknowledgement. An unacknowledged PDF e-mailed to the registry carries no equivalent standing as a filed cross-objection.

- Language — English, with Hindi limited to notified benches. The notified guidance contemplates English as the standard language; Hindi is available only where the bench sits in a State notified by the President of the Appellate Tribunal under Rule 5A. Hindi is therefore not universally available across all benches, and practitioners should check the bench’s notified status before opting for a Hindi filing. Annexures in regional languages should be accompanied by a certified English translation in any event.

A fourth point that is not in the FAQ but is worth flagging: no fee is payable on Form 116. Unlike Form 115 (which carries a tiered fee of ₹500, ₹1,500 or 1% of assessed income capped at ₹10,000 depending on the slab), the cross-objection does not attract a fee. The absence of a fee is sometimes treated by junior staff as a reason to defer filing — "no fee, no urgency" — which is exactly the wrong inference. The 30-day clock runs whether or not money has changed hands.

Why a Cross-Objection Beats a Parallel Appeal

Where a CIT(A) order is mixed and both sides have something to lose, the respondent has two procedural choices: file an independent appeal in Form 115 against the adverse part within the two-month limitation under Section 362(1), or wait for the other side to appeal and then file a cross-objection in Form 116. The cross-objection route has four substantive advantages:

- One proceeding, one bench, one set of submissions. The same bench hears both the appeal and the cross-objection on the same day, against the same record. There is no duplication of paperwork and no risk of inconsistent factual findings between two ITAT benches on the same assessment year.

- No fee. The respondent saves up to ₹10,000 in appeal fee per assessment year per appeal that would otherwise have been independently filed.

- Procedural symmetry. A cross-objection is heard and disposed of "as if it were an appeal" under Section 362(4). The respondent gets the same substantive treatment of the grounds without taking on the procedural burden of a fresh appellant.

- Reduced litigation footprint. Where the appellant subsequently withdraws or settles, the cross-objection survives and is heard on its own merits — provided it was filed as a cross-objection and not as a defensive reply.

The trade-off is the 30-day window. Where a respondent is uncertain whether the other side will appeal, the safer course is to file an independent Form 115 appeal within the two-month limitation, and consider withdrawing it if the other side does not appeal. Form 116 should be the chosen instrument only where appeal by the other side is reasonably certain and the respondent is in a position to react within 30 days of service.

Practitioner Checklist Before Filing Form 116

The items below are practice points drawn from the new workflow, not statements of law — position them as guidance, not rules.

- Confirm the date of service of the notice of appeal. Pull the ITAT portal alert, the registered-post acknowledgement, or the Faceless channel timestamp. Diary an internal deadline well before the 30-day expiry.

- Pull the appellant’s Form 115 and identify the grounds being raised. The cross-objection should respond to those grounds where the respondent agrees with CIT(A) and independently raise grounds where the respondent disagrees with CIT(A). Mixing the two kills clarity.

- Cross-check the signatory for the applicable category. For assessee-filed cross-objections this is the person specified under Rule 167(3); for other categories confirm the applicable signing rule. A Form 116 signed by an unauthorised person is a high-cost and easily avoidable defect.

- Draft the grounds as numbered propositions, with tax effect for each. The grounds section does not accept narrative pleadings — the registry will raise a defect.

- Assemble and pre-verify all enclosures. CIT(A) order, Form 115 as served, key supporting documents. Confirm PDFs are within the portal’s file-size limits and OCR-searchable where possible.

- If filing late, draft the condonation statement first. The reason for delay must hold up to a sufficient-cause test on the record — "internal review pending" does not.

- Build a filing buffer. As a matter of practice, aim to complete the filing well before the 30-day expiry. Portal load and DSC issues at the wire have, in the experience of many practitioners, killed otherwise meritorious cross-objections.

- Save the e-Filing acknowledgement number and the timestamp. This, not the date the PDF was prepared, is the date of filing for limitation purposes.

Closing Note

The shift from Form 36A to Form 116 is not merely a relabelling. It consolidates cross-objections into the ITAT e-filing workflow, ties the signatory rule for assessee filings into the same framework that governs returns of income under the new Act, and removes the safety net of post-filing edits. For practitioners who have spent careers filing Form 36A as an afterthought to the main appeal, the move requires a procedural reset: the 30-day window is non-negotiable, the form is final on filing, and the grounds raised in the notified form are the pleading that the bench will read first. Get the filing right on the day it goes in — the new framework leaves little room to fix it afterwards.

Comments (0)

No comments yet. Be the first to comment!