Why Rule 36(4) Matters Even Today

Rule 36(4) of the CGST Rules is the reason every ITC claim in India now hinges on GSTR-2B. Although the rule was effectively replaced as a limiting provision on 1 January 2022, it is the rule that trained Indian businesses and their CAs to match input credit against supplier filings — not against their own purchase books. It marked the shift from buyer-controlled ITC to supplier-driven compliance. Understanding how Rule 36(4) evolved explains how we ended up with the current 100% 2B-matching regime, and why the IMS (Invoice Management System) was introduced in late 2024.

The Starting Point — October 2019

Before Rule 36(4), a GST-registered buyer could claim ITC based on their own purchase invoices, whether or not the supplier had filed GSTR-1. This created a massive fake-invoicing problem: buyers claimed credit on invoices that did not exist in the supplier's returns.

On 9 October 2019, CBIC inserted Rule 36(4) into the CGST Rules via Notification 49/2019-Central Tax. The rule imposed the first cap on provisional ITC:

- ITC not reflected in GSTR-2A (the earlier dynamic statement) was capped at 20% of the eligible credit that was reflected

In other words, if your supplier had filed only part of your purchases in GSTR-2A, you could still claim up to 20% more on top — but no further.

The Three Tightenings

Rule 36(4) then went through three successive tightenings:

Effective Date Cap on Unreflected ITC Authority 9 Oct 2019 20% Notification 49/2019-Central Tax 1 Jan 2020 10% Notification 75/2019-Central Tax 1 Jan 2021 5% Notification 94/2020-Central Tax

Each tightening narrowed the gap between what the buyer could claim and what the supplier had actually filed. By early 2021, the squeeze was severe — if your supplier was even a few days late with GSTR-1, 95% of your ITC was already locked out of that month's claim.

The Final Shift — 100% GSTR-2B Matching from 1 January 2022

The Finance Act, 2021 amended Section 16(2) of the CGST Act to insert clause (aa), which made it a statutory condition that ITC can be availed only if the supply is reflected in the details "furnished by the supplier in the statement of outward supplies" and communicated to the recipient. CBIC gave this teeth through Notification 40/2021-Central Tax dated 29 December 2021, effective 1 January 2022:

- Rule 36(4) was substituted in its entirety

- The 5% provisional ITC buffer was removed

- ITC now flows primarily from GSTR-2B (the monthly static statement generated from supplier GSTR-1 and IFF filings)

In practice, ITC is expected to align with GSTR-2B. If an invoice is not reflected, credit is typically deferred until it appears, even though the legal position still rests on Section 16 conditions.

Why GSTR-2B Replaced GSTR-2A

GSTR-2A is dynamic — it keeps updating as suppliers file or revise their returns. That made it useless for audit trails.

GSTR-2B is static. It is generated on the 14th of each month for the preceding month, and once generated, it is locked. Whatever is in GSTR-2B for a given month serves as the primary basis for ITC availability in that period.

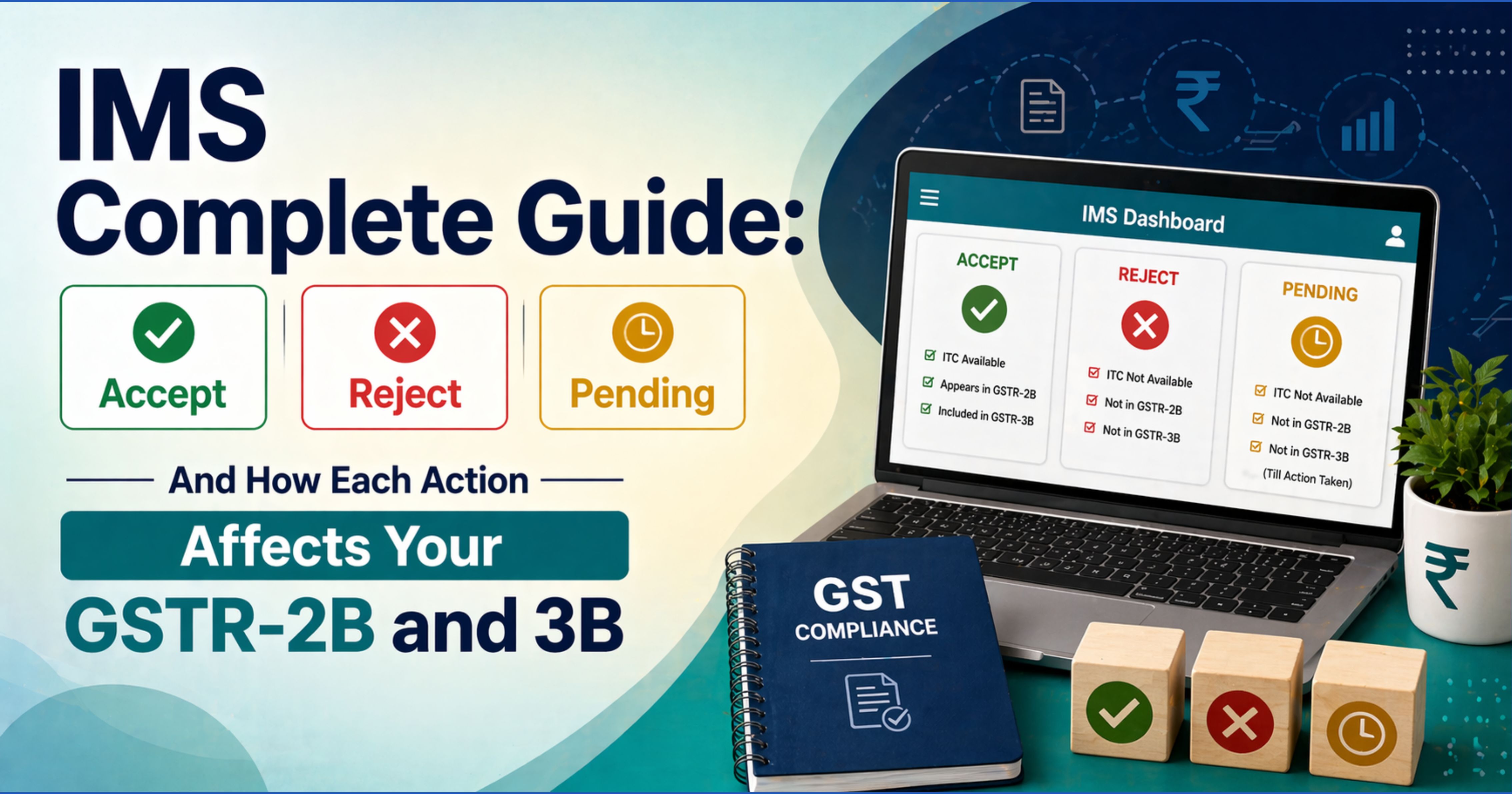

The 2024 Addition — IMS (Invoice Management System)

The 100% 2B regime gave buyers zero control over what landed in their 2B. A late supplier filing, or a clerical error in a supplier's GSTR-1, could still inflate or deflate a buyer's 2B without the buyer's knowledge.

To solve this, CBIC launched the Invoice Management System (IMS) on the GST portal from 1 October 2024. IMS allows recipients to take actions such as Accept, Reject, or mark invoices as Pending before GSTR-2B generation. These actions influence how invoices reflect in 2B, subject to GST portal rules and limits.

IMS sits upstream of GSTR-2B. The window to take action typically falls between supplier GSTR-1 filing (around the 11th) and GSTR-2B generation (around the 14th).

Summary Timeline

- Pre-Oct 2019 — ITC claimed from own purchase books; fake-invoice era

- 9 Oct 2019 — Rule 36(4) inserted: 20% cap on unreflected ITC

- 1 Jan 2020 — cap tightened to 10%

- 1 Jan 2021 — cap tightened to 5%

- 1 Jan 2022 — Rule 36(4) replaced by 100% GSTR-2B matching; Section 16(2)(aa) made it statutory

- 1 Oct 2024 — IMS launched, giving recipients action rights upstream of 2B

What This Means for Your ITC Workflow Today

- The matching is strict in practice. An invoice must be in your GSTR-2B to claim credit.

- Monthly 2B is locked from around the 14th onwards. Action on any invoice must happen during the IMS window.

- Reconcile books with 2B, not the other way around. If your books show an invoice that 2B does not, your books are not the authority — your supplier's GSTR-1 filing is.

- IMS gives you pre-2B control. Use it every month, not just at year-end.

- During GST audits, reconciliation with GSTR-2B is treated as the primary benchmark by authorities.

Bottom Line

Rule 36(4) was never an end-state. It was a three-year ramp to prepare Indian businesses for the 100% supplier-matched ITC regime that came in on 1 January 2022. The IMS that launched in October 2024 closes the last gap — giving recipients a say in what lands in their 2B. Understanding this arc is what separates a reconciled ITC register from one that will crack under a GST audit.

Comments (1)

Nicely explained.