What the New Financial Year Actually Demands

Every April brings a batch of GST housekeeping tasks, and it is easy for practitioners to conflate what is genuinely changing with what is being speculated about in WhatsApp groups. This article is a conservative, notification-anchored walkthrough of what matters for April 2026. The focus is on rules that are actually on the books or on the portal today, separated from recommendations of the 56th GST Council that still await implementing notifications.

The material is organised in three buckets: already notified and in force, portal-level advisories that practitioners need to track, and watchlist items where a change has been recommended but not yet notified.

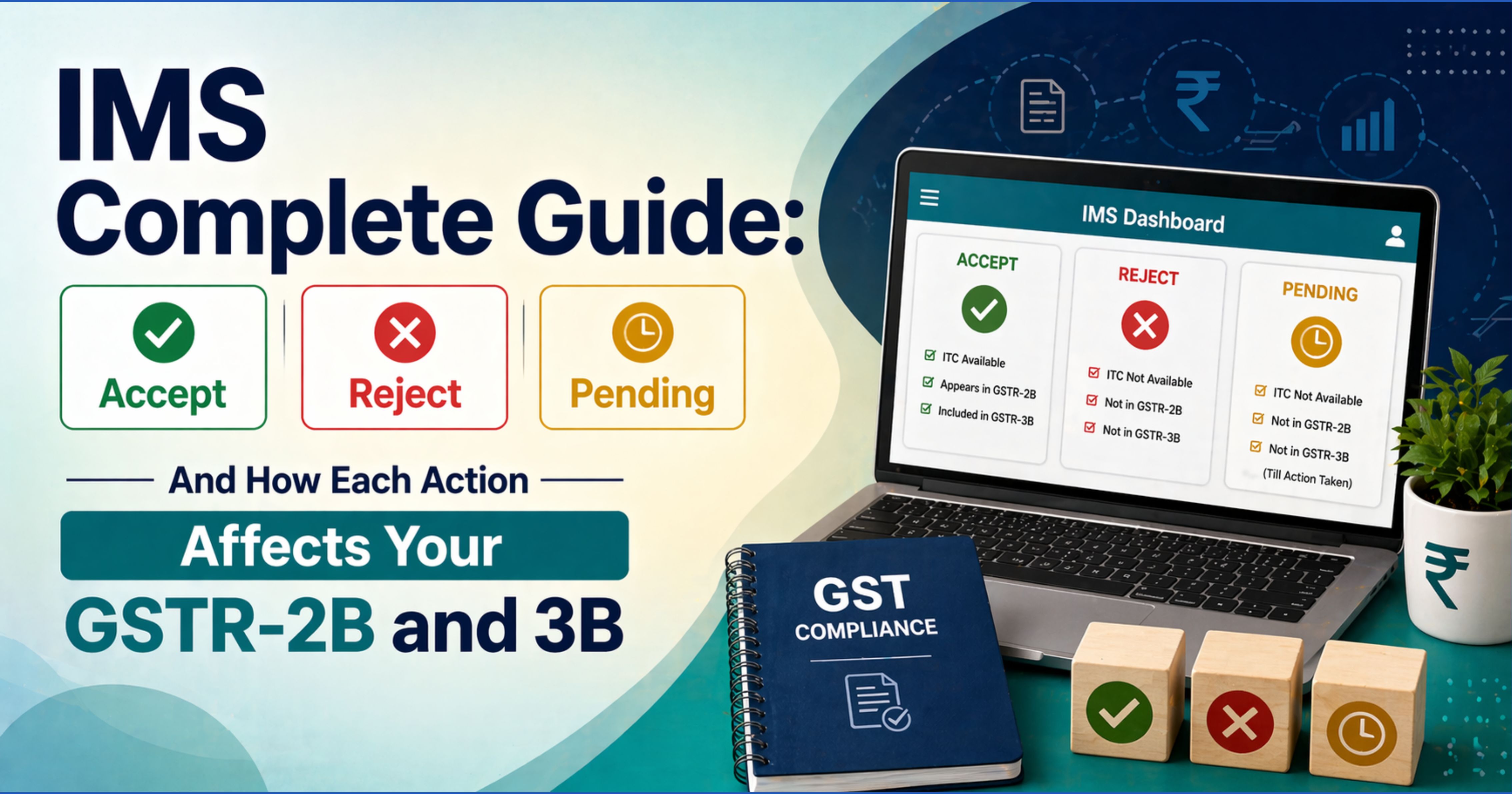

1. Invoice Management System (IMS): Operational Mechanics

The Invoice Management System went live on the GSTN portal on 1 October 2024 pursuant to GSTN advisories dated 3 September 2024 and 17 September 2024, with the detailed FAQ released on 22 September 2024. IMS is not a new April 2026 feature; it is by now a settled part of the compliance workflow, and the April 2026 exercise is about making sure the in-house process around it is robust.

How Records Flow

- Accepted records and records that are deemed accepted (no action taken before GSTR-2B generation) flow into the recipient's GSTR-2B and onwards to GSTR-3B.

- Rejected records do not flow to GSTR-2B, and the corresponding ITC is not auto-populated.

- Pending records are held back from the current month's GSTR-2B and carry forward to subsequent months until the recipient acts on them.

- Action on IMS is frozen once the recipient files GSTR-3B for the relevant tax period. Late changes therefore become a next-period exercise.

The operational implication for April is simple: IMS is now the buffer between the purchase register and GSTR-2B, and a disciplined accept-reject-pending workflow must be in place at the recipient's end. Leaving everything on deemed acceptance is legally permissible, but it means the recipient is passively claiming ITC on every supplier upload, including the ones that may not match their books.

2. GSTR-3B: Auto-Population Is Stronger, but Editability Is Not Extinct

A common misconception doing the rounds is that from April 2026 every field of GSTR-3B is hard-locked. That is not what the GSTN portal manual currently reflects. The portal today continues to show Table 3.1 and Table 3.2 values as editable by the taxpayer where the system-populated figure differs from the taxpayer's own records, with a warning and an audit trail.

What is increasingly the case is that the auto-populated figures come from GSTR-1/IFF and GSTR-1A and from the supplier-side IMS acceptance trail, and any material deviation creates a mismatch flag. The practical guidance is unchanged:

- Prefer correction at source: if GSTR-1 has an error, fix it through GSTR-1A before filing GSTR-3B for the same period.

- Treat every manual override in GSTR-3B as a documented exception — capture the reason in the workpaper.

- Do not rely on month-end manual edits as a substitute for clean source filings. Where hard-locking of specific tables is rolled out in future phases, that route will disappear.

3. E-Invoicing: Threshold, HSN, and the 30-Day Reporting Rule

Turnover Threshold

E-invoicing under Rule 48(4) continues to apply to registered persons with aggregate annual turnover above ₹5 crore in any financial year from 2017-18 onwards. This threshold has been in force since 1 August 2023 (Notification No. 10/2023-Central Tax) and is not changing on 1 April 2026. Any claim that the threshold is being reduced below ₹5 crore from April 2026 should be cross-checked against a live CBIC notification before being relied upon.

The 30-Day IRN Reporting Window

Taxpayers with aggregate annual turnover of ₹10 crore or more must report e-invoices to the IRP within 30 days of the invoice date. This restriction, first introduced for the ₹100 crore segment in November 2023, was extended to the ₹10 crore and above segment effective 1 April 2025 per the NIC advisory. It is worth a fresh reminder in April 2026 because it remains the single most common cause of e-invoice rejection for mid-sized taxpayers.

HSN Code Digit Requirement

The HSN code digit requirement on B2B invoices varies by turnover slab, not by some uniform six-digit rule:

- Aggregate annual turnover up to ₹5 crore: 4-digit HSN on B2B invoices; HSN on B2C invoices is optional.

- Aggregate annual turnover above ₹5 crore: 6-digit HSN on all invoices, B2B and B2C.

This follows the CBIC press release on HSN/SAC reporting and has not been replaced. Practitioners should cross-check the turnover-slab mapping against their invoicing software masters at the start of the new financial year.

Multi-Factor Authentication

Multi-factor authentication on the e-invoice and e-way bill portals has been made mandatory in phases by turnover, with the rollout now extending to smaller taxpayers per the advisories on ewaybillgst.gov.in and the IRP portals. April is the right month to retire shared logins and ensure every registered user is enrolled for MFA.

4. 56th GST Council: What Is Notified, What Is Not

The 56th GST Council met in September 2025 and made recommendations on rate rationalisation — the most publicised being the collapse of the 12% and 28% slabs and the introduction of a 40% rate for specified demerit goods. The bulk of the rate changes were given effect from 22 September 2025. For April 2026, the practitioner needs to distinguish carefully between what has been notified and what is still being worked out.

Specified Goods: Compensation Cess Continues

The 56th Council press release is explicit that specified goods — including cigarettes, chewing tobacco, zarda, unmanufactured tobacco, and bidi — will continue to attract the existing GST rate plus compensation cess until the loan and interest obligations that the compensation cess was designed to service are fully discharged. The transition from that point onwards is to be notified in due course. In other words, the compensation cess is not a clean sunset on 31 March 2026 for these goods.

The practical takeaway: cess-bearing sector taxpayers should continue their existing cess workflow for April 2026. Do not assume the cess has disappeared, and do not plan closing-stock entries on the assumption of a clean sunset. Monitor CBIC for transition notifications specific to each cess-bearing category.

Rate Rationalisation Catch-Up

Most of the rate changes flowing from the 56th Council took effect in September 2025. A handful of sector-specific classification corrections may still surface in the quarter ending 31 March 2026. The April exercise here is a rate master refresh — verify that every HSN in the ERP is mapped to its current notified rate and that no legacy 12% or 28% residues remain on items that have been reslotted.

5. Watchlist: Recommendations Not Yet Notified

Several items are in the recommendation or pilot stage as of the date of writing. Treat them as things to monitor, not things to plan around:

- Further reduction of the e-invoicing threshold below ₹5 crore. Not notified for April 2026.

- Extension of the 30-day IRN reporting rule to the ₹5 crore to ₹10 crore segment. Not notified.

- A replacement health or clean energy cess structure post-compensation-cess. Requires a constitutional amendment and is not in force.

- Any broader hard-lock of GSTR-3B tables beyond what is currently reflected on the portal.

6. Impact by Taxpayer Size

The April 2026 exercise is asymmetric across taxpayer size. Large taxpayers with mature ERP and reconciliation processes will experience April as a business-as-usual close. The real pressure is on the mid-sized segment — typically ₹5 crore to ₹50 crore turnover — where IMS discipline, e-invoicing within 30 days (if the client crosses ₹10 crore), and HSN slab compliance often get handled manually and drift through the year.

For the smallest taxpayers — below ₹5 crore, out of the e-invoice net and on 4-digit HSN — the April housekeeping is mostly about IMS action hygiene and a supplier-quality review. Chronic late-filers in the supplier base directly delay recipient ITC, and the earlier in the year that problem is flagged, the easier it is to renegotiate terms.

Compliance Checklist for April 2026

- Reconcile the March 2026 GSTR-2B against the purchase register and resolve mismatches before filing March GSTR-3B.

- Enable an IMS action workflow — accept, reject, pending — and assign ownership. Track deemed acceptance as an exception, not a default.

- Run a six-month supplier GSTR-1 filing history report and flag chronic late-filers for commercial review.

- Refresh the HSN master against the turnover slab: 4-digit for aggregate turnover up to ₹5 crore, 6-digit for above ₹5 crore.

- If aggregate turnover is ₹10 crore or more, check that every invoice is being reported to the IRP within 30 days of the invoice date, and set a hard cut-off in the ERP.

- Enable multi-factor authentication on the e-invoice and e-way bill portals for every registered user and retire shared logins.

- For cess-bearing sectors (tobacco, bidi, aerated waters, specified motor vehicles, coal), continue the existing compensation cess workflow and track CBIC for any transition notification specific to the product category.

- Refresh the rate master against the 56th Council notifications from September 2025 and confirm no legacy 12% or 28% residues remain.

- Document any manual override in GSTR-3B with a reason and a reference workpaper.

- Subscribe to the CBIC notification feed and schedule a short weekly review through April to catch any last-minute clarifications, particularly on IRN threshold and cess transition.

Closing Thought

April 2026 is not the rupture that some early commentary has made it out to be. IMS is not new. The e-invoice threshold is not dropping on 1 April. Compensation cess is not sunsetting cleanly for the sensitive sectors. But the cumulative effect of the changes that are already in force — IMS discipline, 30-day IRN reporting, turnover-slab HSN, MFA on the portals — is that the sloppiness which used to be absorbed by month-end manual adjustments is no longer absorbable. The practitioners who start the year with clean masters, a supplier-quality filter, and a documented IMS SOP will move through April without drama. Those who wait for a panic notification to react will spend April firefighting.

Comments (0)

No comments yet. Be the first to comment!