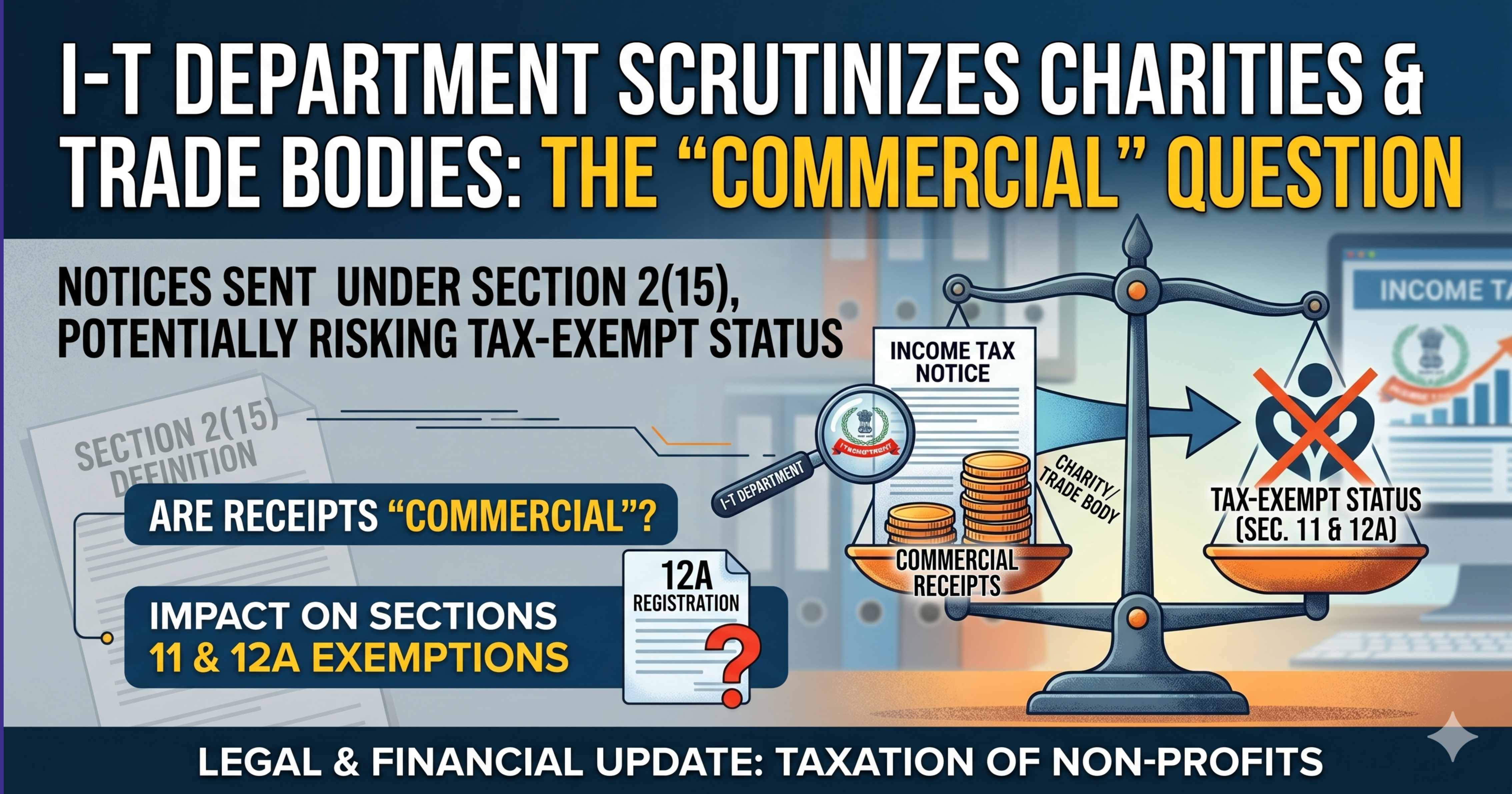

The Income-tax Department has initiated scrutiny of charitable trusts, trade associations, and educational institutions, raising concerns over the nature of certain receipts and their eligibility for tax exemption under the Income-tax Act, 1961. The development centres around the interpretation of “charitable purpose” under Section 2(15), particularly where activities may be construed as commercial in nature.

According to reports, tax authorities have issued notices to several organisations that had either applied for fresh registration or sought periodic renewal of their tax-exempt status under Section 12A. These notices question whether income streams such as seminar fees, training programme charges, certification fees, publications, and membership subscriptions fall within permissible charitable activities or amount to commercial operations.

Section 2(15) defines “charitable purpose” to include activities of general public utility but restricts entities from engaging in trade, commerce, or business beyond specified thresholds. Authorities appear to be examining whether such receipts, though aligned with organisational objectives, cross the boundary into commercial activity, thereby impacting eligibility for exemption.

The notices reportedly require organisations to justify why such receipts should not lead to denial or cancellation of registration. Entities have been asked to demonstrate that their activities remain charitable in substance, maintain proper books of account, and that income generated is incidental to their primary objectives.

Tax experts indicate that this is not an entirely new issue. Judicial precedents, including rulings by the Income Tax Appellate Tribunal (ITAT) and the Supreme Court, have consistently emphasised a “rule of consistency” and the need to examine whether the dominant purpose of an organisation remains charitable. In cases where there is no change in the nature of activities, courts have often taken a favourable view towards assessees.

However, the current round of scrutiny signals a stricter approach by the department, especially in cases involving substantial receipts from organised activities. Officials have also indicated that failure to respond adequately to notices may result in adverse conclusions regarding the genuineness of charitable intent.

Recent tribunal rulings provide some relief to taxpayers. For instance, certain ITAT benches have restored registrations of trade bodies and chambers of commerce, holding that their activities contribute to public utility and do not necessarily amount to commercial enterprise.

The development underscores the need for charitable entities and trade associations to carefully evaluate their revenue streams, documentation, and compliance framework. As scrutiny intensifies, maintaining transparency and demonstrating alignment with charitable objectives will be critical to sustaining tax-exempt status.

Comments (0)

No comments yet. Be the first to comment!