The Institute of Chartered Accountants of India (ICAI) has issued an important announcement dated 10th April 2026, significantly expanding the scope of the Audit Quality Maturity Model (AQMM). This move reflects ICAI’s continued focus on strengthening audit quality, enhancing transparency, and aligning Indian audit practices with global standards.

The announcement partially modifies the earlier notification dated 11th August 2025. Under the revised framework, the mandatory applicability of AQMM has been widened to include more categories of audit firms, particularly those involved in audits of high-impact entities.

What is AQMM?

The Audit Quality Maturity Model (AQMM) is a structured framework developed by ICAI to assess and improve the audit quality standards of firms. It evaluates firms across multiple parameters such as leadership, client acceptance, engagement performance, and quality control systems. AQMM 2.0 represents an updated and more comprehensive version of this model.

Key Change in Applicability:

One of the most important clarifications is that AQMM applicability is now determined based on the nature of the entity being audited, rather than the structure of the audit engagement.

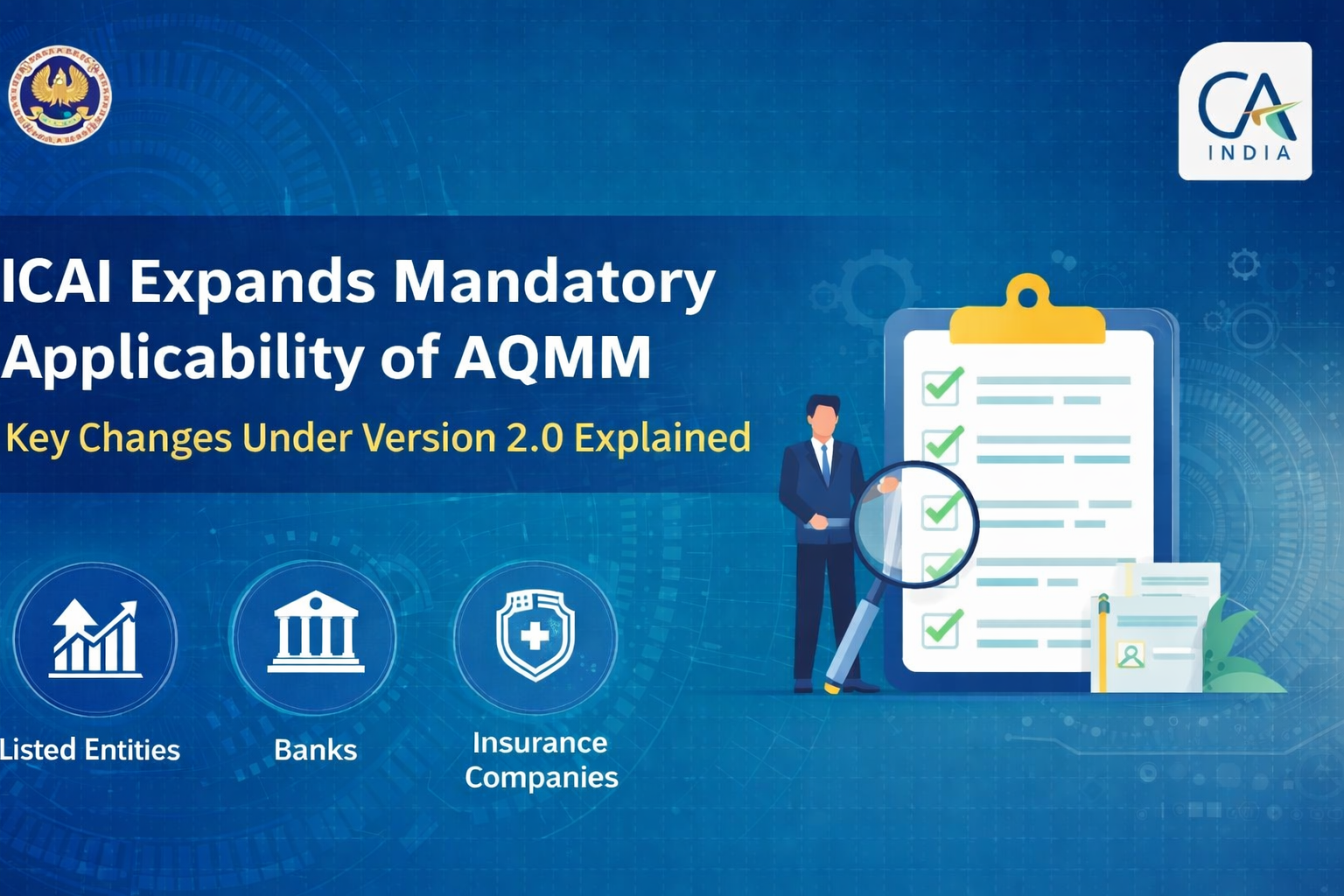

Under the revised guidelines, AQMM is now mandatory for firms auditing:

- Listed entities

- Banks (excluding co-operative banks, except multi-state co-operative banks)

- Insurance companies

Importantly, firms conducting only branch audits are excluded from this requirement.

Expanded Coverage for Group Audits:

A major shift introduced is the inclusion of firms auditing holding, subsidiary, associate, or joint venture entities of the above categories. This means even if a firm is not directly auditing a listed entity but is auditing its group entity, AQMM compliance becomes applicable.

Phased Implementation Approach:

ICAI has adopted a phased implementation strategy to ensure a smooth transition:

- From April 1, 2026:

Firms subject to Peer Review and auditing group entities of listed entities, banks, or insurance companies must comply with AQMM. - From April 1, 2026:

Firms undertaking statutory audits of large unlisted public companies (with paid-up capital of ₹500 crore or turnover of ₹1,000 crore or more, or significant borrowings/deposits) are also covered. - From April 1, 2027:

Firms auditing entities raising funds of ₹50 crore or more from banks, financial institutions, or the public will fall under AQMM.

Practical Implications for Firms:

This expansion has wide-ranging implications. Many mid-sized and even smaller firms will now come under AQMM due to their association with larger group entities. Firms will need to strengthen internal processes, documentation, and quality control mechanisms.

Additionally, since AQMM is closely linked with Peer Review, firms should proactively align their audit methodologies and governance structures to meet the enhanced expectations.

Conclusion:

ICAI’s decision to widen the scope of AQMM marks a significant step towards improving audit quality across the profession. While it increases compliance requirements, it also presents an opportunity for firms to upgrade their systems and build stronger credibility in the market. Chartered accountants and audit firms should carefully assess their engagements and prepare for timely implementation of AQMM 2.0.

Comments (0)

No comments yet. Be the first to comment!