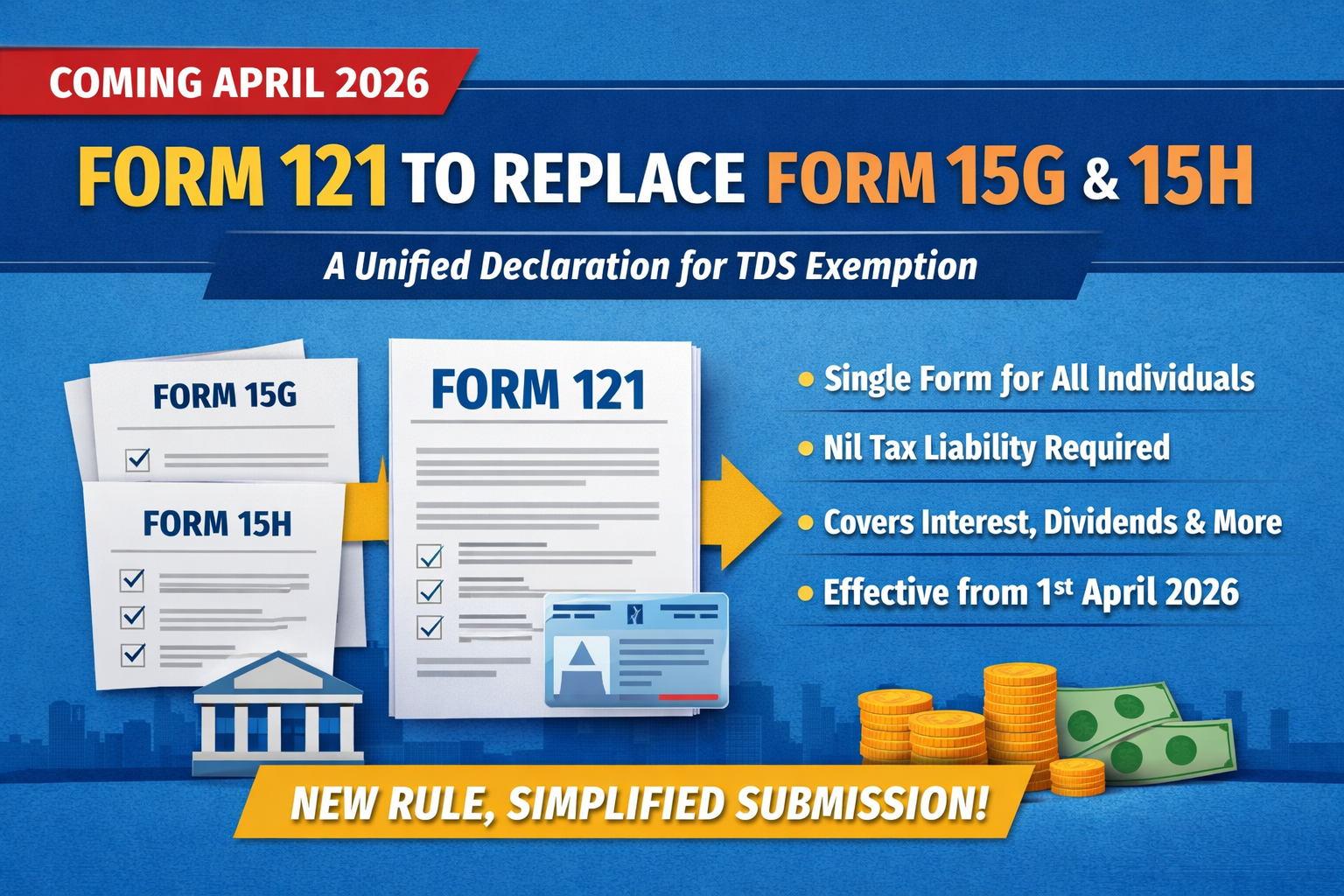

Forms 15G and 15H are being replaced by a new unified Form 121 from April 1, 2026, under the new Income-tax Rules, 2026.

This change is part of a broader effort to simplify and modernize tax reporting under the new Income-tax Act, 2025. The primary objective is to reduce duplication, standardize declarations, and improve ease of compliance for taxpayers.

What is Form 121?

Form 121 is being introduced as a single consolidated declaration form that replaces both Form 15G (for non-senior citizens) and Form 15H (for senior citizens). Its core purpose remains unchanged — to allow eligible taxpayers to declare nil tax liability and prevent deduction of TDS (Tax Deducted at Source) on specified incomes.

According to multiple reports, this new form is age-neutral, meaning there will no longer be separate forms based on age categories.

Why this change?

The move is aimed at simplifying the tax ecosystem. Earlier, taxpayers had to choose between different forms depending on age and eligibility. With Form 121:

- A single form replaces multiple declarations

- Reduces confusion and duplication

- Enables better standardisation and digital processing

- Improves compliance tracking through unified reporting systems

Experts suggest this is part of a larger trend where tax forms are being renumbered and rationalised under the new regime.

Key features being reported

Based on articles across major platforms, Form 121 is expected to include:

- A single declaration format for all eligible taxpayers

- Applicability to resident individuals, HUFs, and eligible persons

- Requirement of PAN for validation

- Filing required with each deductor (banks, institutions, etc.)

- Continued condition of nil tax liability for eligibility

Additionally, some reports highlight enhanced disclosure requirements, such as details of past ITR filings, to improve transparency and accountability.

Scope of income covered

Similar to existing forms, Form 121 is expected to cover:

- Interest income (FDs, RDs, savings)

- Dividends

- Certain other specified incomes

Its purpose remains to ensure that tax is not deducted at source when the final tax liability is zero.

Practical implications for taxpayers

This development is particularly relevant for:

- Senior citizens dependent on interest income

- Salaried individuals with low taxable income

- Investors relying on fixed deposits or similar instruments

As per media reports, early submission of Form 121 at the start of the financial year is advisable to avoid unnecessary TDS deductions.

Final perspective

While multiple leading websites and expert platforms are discussing Form 121 as a replacement for Forms 15G and 15H, the change is closely linked to the implementation of the new Income-tax framework from April 2026.

From a professional standpoint, this is a structural simplification move—aimed at reducing compliance friction while maintaining the same underlying principle:

No TDS where there is no tax liability.

Comments (0)

No comments yet. Be the first to comment!