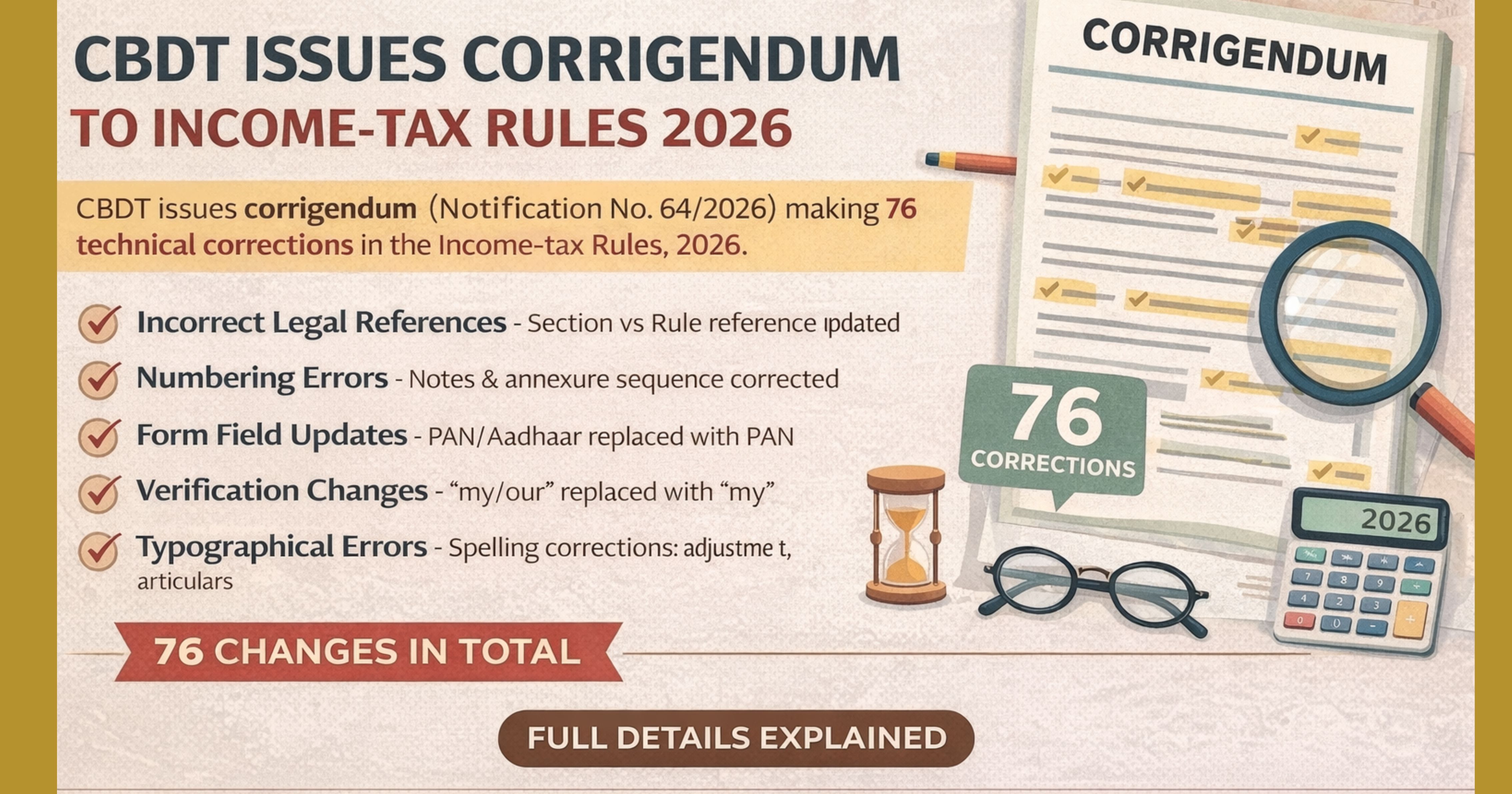

CBDT Issues Corrigendum to Income-tax Rules 2026

The Central Board of Direct Taxes (CBDT), under the Ministry of Finance, has issued a corrigendum dated 16 April 2026 to rectify errors in the Income-tax Rules, 2026 earlier notified on 20 March 2026.

This corrigendum has been notified vide Notification No. 64/2026 [G.S.R. 286(E)] and includes 76 separate corrections across multiple pages, rules, forms, and annexures.

Nature of Corrections

The corrigendum primarily addresses technical and drafting errors, which can be broadly classified into:

1. Incorrect Legal References

Several provisions incorrectly referred to sections instead of rules or vice versa.

- Rule 165 corrected reference to section 263(2)

- Rule 243 corrected references from section 242 & 244 to rule 242 & 244

These corrections are critical as wrong references may lead to incorrect interpretation of law.

2. Numbering and Structural Errors

A large number of corrections relate to wrong numbering in:

- Notes (A-1-1 changed to A-1)

- Annexures (re-numbering of clauses like (x), (xi) → (i), (ii))

- Parts and headings (VII → I, VIII → II, etc.)

These ensure consistency and proper structure of forms and schedules.

3. Form and Data Field Corrections

Several important changes have been made in forms:

- Replacement of “PAN/Aadhaar” with “PAN” in multiple places

- Removal of Aadhaar column in certain tables

- Standardisation of Contact Number format (Country Code + Number)

These changes indicate a move towards clearer identification requirements and structured data capture.

4. Verification Clause Corrections

In multiple forms and certificates:

- “my/our” replaced with “my” in verification sections

This removes ambiguity in declarations and ensures consistency in responsibility.

5. Typographical and Drafting Errors

Several typographical mistakes have been corrected:

- “adjustme t” → “adjustment”

- “articulars” → “Particulars”

- “befor adjustment” → “before adjustment”

Though minor, such corrections are important for professional documentation.

6. Content and Terminology Changes

Some substantive wording changes include:

- “specified fund or stock broker” replaced with

“constituent entity or group name” - “securitization trust” replaced with

“Venture Capital Company or Venture Capital Fund”

These changes reflect alignment with updated terminology under the new law.

7. Omissions and Deletions

The corrigendum removes certain incorrect or redundant elements:

- Removal of “drop down” wording in forms

- Omission of Aadhaar-related fields

- Deletion of unnecessary numbering and headings

8. Reformatting of Tables and Schedules

Certain schedules have been restructured, for example:

- Revised format for parent entity details in international group reporting

- Updated row structures and headings in multiple Parts (A, B, C, etc.)

Scale of Corrections

The corrigendum spans corrections from:

- Page 1664 to 2500+

- Covering rules, notes, annexures, forms, and verification clauses

- Total 76 corrections, making it a significant technical revision

Practical Impact for Chartered Accountants and Tax Professionals

While most changes are technical, their impact is important:

✔ Ensures correct interpretation of law

Wrong references (section vs rule) can lead to incorrect compliance positions

✔ Avoids filing errors

Changes in forms, fields, and numbering directly affect reporting

✔ Improves documentation accuracy

Correct terminology and structure reduce ambiguity

✔ Important for audits and certifications

Verification clause changes impact declarations and responsibility

Key Takeaway

This corrigendum does not introduce new provisions, but it plays a crucial role in:

- Cleaning drafting errors

- Aligning references correctly

- Standardising forms and reporting

For professionals, ignoring these corrections can still lead to compliance mistakes, especially in filings and certifications.

Conclusion

The CBDT corrigendum dated 16 April 2026 is a comprehensive technical correction exercise for the Income-tax Rules, 2026.

Comments (0)

No comments yet. Be the first to comment!