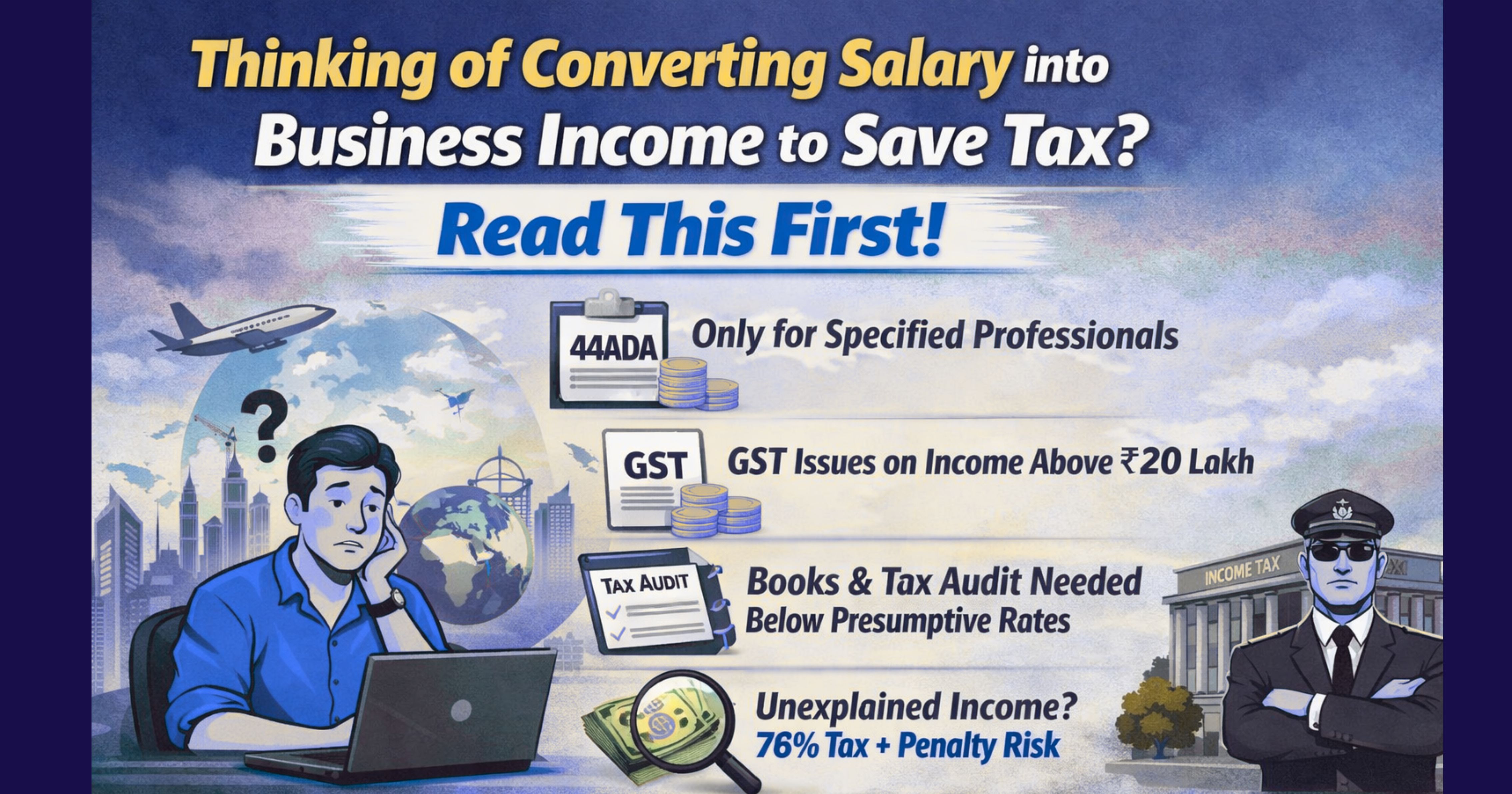

With the rise of remote work and global freelancing opportunities, a growing number of individuals are exploring whether they can classify their income as business or professional income instead of salary. The motivation is clear—presumptive taxation schemes like Section 44AD and Section 44ADA appear to offer a simple way to reduce taxable income.

However, the law does not permit such classification purely based on convenience.

The first step is to understand whether your income genuinely qualifies as professional income. Section 44ADA applies only to specified professionals such as doctors, lawyers, architects, and accountants. Many remote workers assume that earning from foreign clients or working independently makes them eligible. In reality, if the nature of work reflects characteristics of employment—such as fixed working hours, supervision, or dependency—it may still be treated as salary in substance.

Even if income is treated as business or professional income, compliance requirements increase. Once total receipts exceed ₹20 lakh, GST registration may become applicable. This includes export of services, as such receipts are considered while calculating aggregate turnover, even though they are zero-rated. As a result, freelancers working with foreign clients may still need to handle GST filings, invoicing, and compliance.

Where Section 44ADA is not applicable, taxpayers often consider Section 44AD. This scheme allows presumptive taxation at 6% or 8% of turnover, subject to conditions such as turnover limits (currently up to ₹3 crore where cash receipts are within prescribed limits). Similarly, Section 44ADA applies up to ₹50 lakh (or ₹75 lakh where cash receipts are within limits) and is available only to individuals and partnership firms, not LLPs.

A critical point often misunderstood is how presumptive taxation works. These provisions set a minimum benchmark for income declaration. Taxpayers are free to declare higher income if their actual profits are more. However, declaring income lower than the presumptive rate is not permitted unless proper books of account are maintained and, where applicable, a tax audit under Section 44AB is carried out.

Another important risk arises from mismatch between declared income and financial behaviour. If a taxpayer reports low profits but makes significant investments or incurs high expenses, the difference may be questioned. In such cases, provisions like Section 69 may apply, treating the excess as unexplained income. This income is taxed at special rates under Section 115BBE, along with penalty implications, leading to a very high effective tax burden.

Ultimately, tax authorities evaluate the substance of the arrangement rather than its label. Simply converting salary into business income on paper, without a genuine change in the nature of work, may not sustain under scrutiny.

The key takeaway is simple: tax planning must be aligned with legal provisions and actual facts. Misclassification may provide short-term benefit but can result in long-term exposure.

Comments (0)

No comments yet. Be the first to comment!