TL;DR: The Income-tax Act, 2025 came into force on 1 April 2026. It replaces the 60-year-old Income-tax Act, 1961. The biggest single change in vocabulary: the dual "Previous Year / Assessment Year" system is retired in favour of a single "Tax Year". But here is the part most taxpayers are missing: your ITR for FY 2025-26 income, filed by 31 July 2026, is still entirely under the 1961 Act (AY 2026-27). The Tax Year concept first applies to income earned from 1 April 2026 onwards, which will be filed as Tax Year 2026-27. There is no overlap and no missing year. The 2025 Act largely re-presents existing law and does not itself introduce a fundamentally new category of tax; no major new compliance obligation applies for FY 2025-26 merely because the 2025 Act has commenced. Slabs, deductions, due dates, ITR forms, and refund mechanics for the current filing season are all governed by the 1961 Act. The core objective of the transition is structural simplification and re-organisation rather than a wholesale policy rewrite.

That said, a lot of structure has changed. The new Act has 536 sections and 16 schedules (the 1961 Act had 819 sections and 14 schedules). The Income-tax Rules, 2026 collapse 511 rules into 333. Forms drop from 399 to 190. And almost every section number you have memorised — §80C, §44ADA, §115BAC, §87A, §139, §234A — has a different number under the 2025 Act. This guide walks through what actually changed, what is just renumbering, and what you need to do differently in the AY 2026-27 filing season.

1. The Three Terms — A Quick Recap

Under the Income-tax Act, 1961, a single year of income was tracked through two separate twelve-month windows that confused taxpayers for six decades:

- Previous Year (PY) — the financial year in which the income is earned. Salary you draw from 1 April 2025 to 31 March 2026 belongs to PY 2025-26. Defined under Section 3 of the 1961 Act, the Previous Year is uniformly the financial year (1 April to 31 March), with limited exceptions for newly set-up businesses or new sources of income.

- Assessment Year (AY) — the financial year that immediately follows the Previous Year. Income of PY 2025-26 is assessed in AY 2026-27 (1 April 2026 to 31 March 2027). Defined under Section 2(9) of the 1961 Act. The AY is the period during which the ITR is filed, the assessment is completed, the refund is issued, and any scrutiny / rectification / appeal is processed.

- Financial Year (FY) — colloquial term, identical to the Previous Year in practice. The Government's accounting and budget year (1 April to 31 March).

The mismatch — income earned in one year, taxed and assessed in a different-sounding year — created confusion that no amount of CBDT outreach could fix. Forms used "AY 2026-27", banks issued Form 16 marked "FY 2025-26", clients in casual conversation used "this year's tax", and the actual filing happened anywhere between June and December of the AY. Every taxpayer query that begins with "is this for last year or this year?" traces back to this terminology.

The Income-tax Act, 2025 retires the PY / AY distinction. Income earned and taxed are tracked under a single label: the Tax Year.

What "Tax Year" Means

The Income-tax Act, 2025 defines the Tax Year as a period of twelve months contained in a financial year (1 April to 31 March). For income earned during 1 April 2026 to 31 March 2027, the label is Tax Year 2026-27. There is no separate "assessment year" label for this income — the same Tax Year 2026-27 description covers both the period of earning and the period of subsequent return-filing / assessment. This is the simplification.

The CBDT's official position, in the FAQs published on the Income Tax India portal, is that the Tax Year concept "is applicable from 01 April 2026, i.e., for income earned during FY 2026-27 onwards". The first Tax Year is therefore Tax Year 2026-27. Income for FY 2025-26 — i.e., the income you are about to file ITR for in July / October 2026 — is not labelled "Tax Year 2025-26". It remains AY 2026-27 under the 1961 Act.

2. The Transition Map — Which Act Governs Which Year

This is the part to get exactly right. Spell it out once, then refer back as needed.

Income earned during Governed by Label / Year ITR filing window FY 2024-25 (1 April 2024 – 31 March 2025) Income-tax Act, 1961 AY 2025-26 Filed in 2025 (closed for non-audit; ITR-U window open till 31 March 2030 under §139(8A) as extended by Finance Act, 2025) FY 2025-26 (1 April 2025 – 31 March 2026) Income-tax Act, 1961 AY 2026-27 31 July 2026 (non-audit) / 31 October 2026 (audit) — current filing season FY 2026-27 (1 April 2026 – 31 March 2027) Income-tax Act, 2025 Tax Year 2026-27 Filed in 2027 (due dates as notified under the new Act and Income-tax Rules, 2026) FY 2027-28 onwards Income-tax Act, 2025 Tax Year 2027-28 onwards Annual filing under the new ActTwo things to lock in:

- The 1 April 2026 date is the income cut-off, not the filing cut-off. The new Act applies to income earned from 1 April 2026 onwards. The fact that an ITR happens to be filed on (say) 25 July 2026 — i.e., after the new Act has come into force — does not change which Act governs the assessment. The assessment of FY 2025-26 income is under the 1961 Act; the new Act applies to that ITR only via the savings clause (and only for procedural / consequential aspects, not for substantive computation).

- There is no missing year and no overlap. Every rupee of income from any date falls cleanly under exactly one Act. The 1961 Act covers up to 31 March 2026; the 2025 Act covers from 1 April 2026 onwards. Neither overlap nor a gap.

3. What Section 536 of the New Act Saves

Section 536 of the Income-tax Act, 2025 is the repeal-and-savings clause. Its work is to ensure that nothing falling under the 1961 Act before 1 April 2026 is left in legal limbo. The savings cover, broadly:

- Pending proceedings — any assessment, reassessment, rectification, scrutiny, appeal, or revision initiated under the 1961 Act before 1 April 2026 continues under the 1961 Act. The transition does not push such proceedings into the new Act.

- Pending refunds, demands, and recoveries — refund claims, outstanding demands, recovery proceedings, and appeals before the CIT(A), ITAT, High Court, or Supreme Court that originated under the 1961 Act are processed under the 1961 Act.

- Notifications, circulars, instructions, approvals, registrations — existing circulars and instructions issued under the 1961 Act generally continue to be valid unless they are inconsistent with the 2025 Act or have been specifically superseded. The expectation is therefore that practitioners and taxpayers can continue to rely on existing CBDT circulars on procedural matters until and unless a specific circular is withdrawn or replaced.

- Vested rights and accrued obligations — exemptions claimed, rebates earned, deductions availed, set-offs carried forward (capital losses, business losses, unabsorbed depreciation), and benefits accrued under the 1961 Act before 31 March 2026 are preserved. Carry-forward of losses and depreciation continues into Tax Year 2026-27 and beyond on the same statutory clock that started running under the 1961 Act.

- Past assessments — if your AY 2023-24 assessment was completed under the 1961 Act, it remains a valid assessment after 1 April 2026. You do not have to "re-assess under the new Act".

The shorthand reading: once a rupee of income or a tax event was firmly under the 1961 Act, it stays under the 1961 Act for its entire downstream lifecycle — including any future appeal, rectification, or refund processing. The 2025 Act does not retrospectively re-characterise it.

4. The AY 2026-27 ITR — What Actually Changes for the Current Filing Season

Here is the answer that matters for ninety per cent of taxpayers: almost nothing changes for the ITR you file by 31 July 2026. The substantive law, slab rates, deductions, presumptive schemes, capital-gains regimes, TDS sections, and refund mechanics for FY 2025-26 income are all under the 1961 Act. The new Act is parked alongside, applicable only to FY 2026-27 income and beyond.

Things that are different in the AY 2026-27 filing window — but driven by amendments made under the 1961 Act itself by Finance Act, 2024 and Finance Act, 2025, not by the 2025 Act:

- Default tax regime — for FY 2025-26, the new tax regime under §115BAC is the default. You must affirmatively opt out into the old regime via Form 10-IEA (for income from business or profession) or by selecting the option in the ITR (for salaried / non-business filers). Non-action defaults you to the new regime.

- 87A rebate ladder — Finance Act, 2025 raised the §87A rebate ceiling under the new regime to Rs. 12 lakh of total income (capped at Rs. 60,000 of tax) for FY 2025-26 onwards, effectively zeroing out tax for taxpayers under that threshold. Earlier (up to FY 2024-25), the equivalent rebate was capped at Rs. 25,000 with a Rs. 7 lakh income ceiling. The old regime continues to provide §87A rebate up to Rs. 5 lakh of total income (capped at Rs. 12,500). Verify the exact figures on the e-filing portal before applying.

- ITR-1 expanded eligibility — for AY 2026-27, ITR-1 (Sahaj) can now be used by taxpayers with income from up to two house properties (previously one). Other Sahaj eligibility conditions (total income up to Rs. 50 lakh, no foreign assets, no agricultural income above Rs. 5,000, no capital gains except limited LTCG up to Rs. 1.25 lakh under §112A in some recent versions of Sahaj) continue to apply — verify the final notified schema before filing.

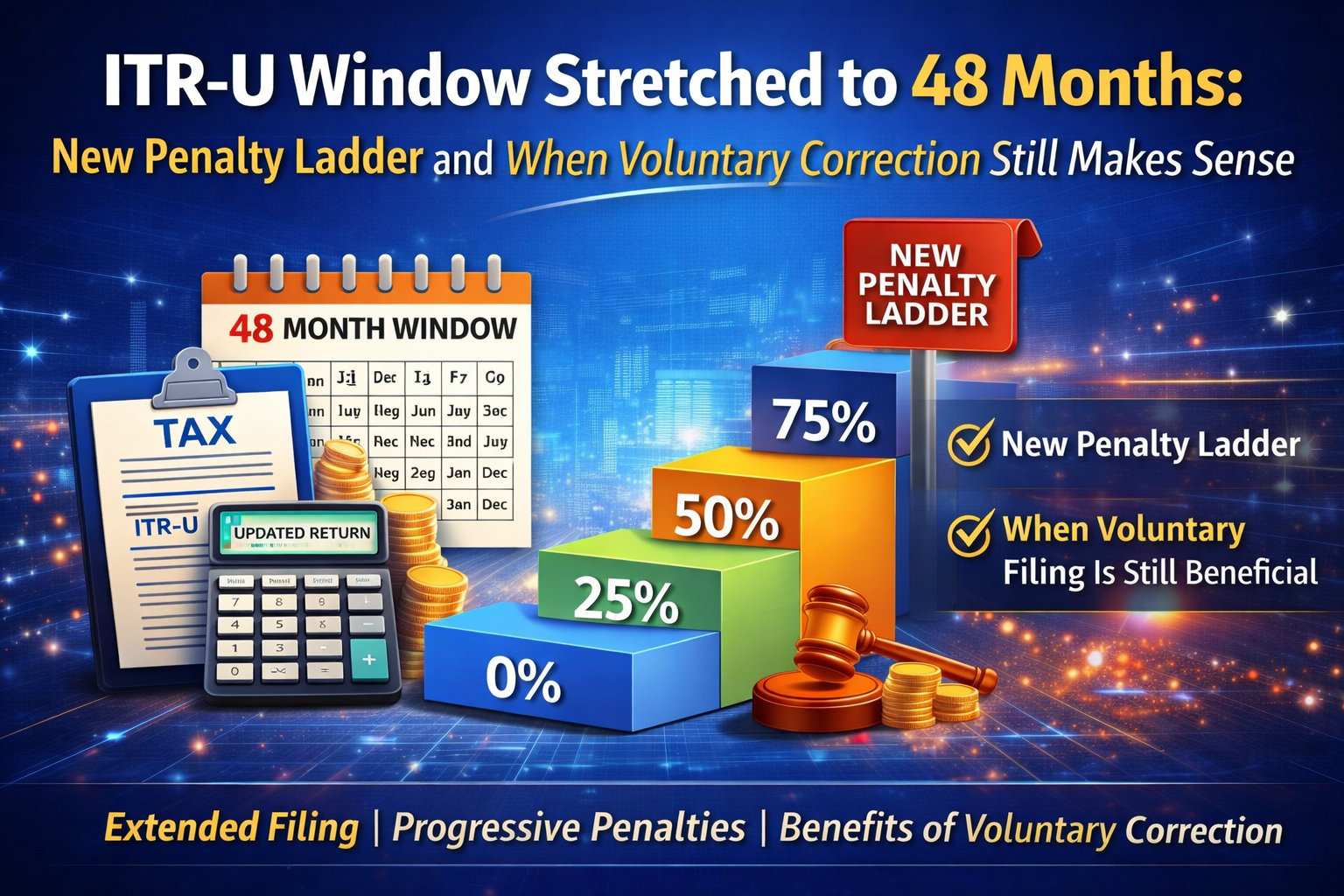

- ITR-U time window extended — the updated-return window under §139(8A) was extended by Finance Act, 2025 from 24 months to 48 months from the end of the relevant AY. The longer window applies prospectively to ITR-U filings made on or after 1 April 2025; it gives taxpayers four years instead of two to clean up missed disclosures (subject to the Section 140B additional-tax ladder of 25 % / 50 % / 60 % / 70 %).

- Direct Tax Vivad se Vishwas, 2024 — the second VsV scheme covering pending appeals and writs as on 22 July 2024 has its compliance forms and outcomes recorded during the AY 2026-27 cycle. Any taxpayer who opted in is processing their settlement under the 1961-Act-era VsV machinery.

- HRA exemption — expanded city list — the Income-tax Rules, 2026 (notified by CBDT in early 2026, applicable from FY 2026-27 onwards) expand the category of cities eligible for the higher 50 % HRA-exemption ceiling beyond the traditional four metros (Mumbai, Delhi, Chennai, Kolkata). This change does NOT apply to your AY 2026-27 ITR. For FY 2025-26 salary, the older Income-tax Rules, 1962 framework continues — only the four traditional metros qualify for the 50 % ceiling, and HRA in all other cities is at 40 %. Refer to the notified Rules 2026 for the exact list of cities that qualify for the higher ceiling from FY 2026-27 onwards.

So when you sit down to file in July 2026: open the e-filing portal as usual, pick the ITR form that fits your sources of income (the decision tree has not changed), use the 1961 Act section numbers (§80C, §80D, §24(b), §44ADA, etc.), apply the slab rates notified for FY 2025-26, and submit. The Tax Year vocabulary does not enter the picture for this year's filing.

5. Worked Example — The Same Taxpayer Across the Transition

Take Mr. Aniket, a salaried professional in Bengaluru with side-consulting income.

FY 2024-25 (PY 2024-25, AY 2025-26): Aniket earned salary plus consulting fees. He filed his ITR in July 2025 under the 1961 Act. Slab rates of FY 2024-25 applied. Rebates, deductions, and the new regime / old regime choice were exercised under the 1961 Act. His refund, if any, was issued in the AY 2025-26 cycle. Status today: closed assessment under the 1961 Act, with a 48-month ITR-U window open until 31 March 2030.

FY 2025-26 (PY 2025-26, AY 2026-27 — the year you are about to file for): Salary received during 1 April 2025 to 31 March 2026; consulting fees similarly. The Form 16 is for "FY 2025-26"; the ITR will be filed for "AY 2026-27" under the 1961 Act. Slab rates, deductions, regimes, due dates — all under the 1961 Act. The ITR is filed on or before 31 July 2026 (non-audit) or 31 October 2026 (audit). The fact that the new Income-tax Act, 2025 is in force on the date he files the ITR does not move the filing into the 2025 Act.

FY 2026-27 (Tax Year 2026-27 — the first year under the new Act): From 1 April 2026 onwards, income is governed by the Income-tax Act, 2025. Aniket's salary, consulting fees, capital gains, and any other income from this period will be aggregated under "Tax Year 2026-27". The ITR for this year — to be filed in 2027 under due dates notified by the new Act — will use the 2025 Act's section numbers, the new ITR forms (notified by CBDT under the Income-tax Rules, 2026), and the new Tax Year nomenclature. The "AY" label disappears for this year.

If Aniket has a pending appeal at the ITAT for AY 2022-23 — initiated under the 1961 Act, currently mid-hearing in 2026 — that appeal continues under the 1961 Act regardless of the new Act being in force. Section 536 saves the proceeding. The same applies to any reassessment notice under §148 issued before 31 March 2026, any rectification application under §154, any refund claim under §237, or any TDS-mismatch correction.

6. The Vocabulary Survival Guide — Old to New

Most of the substantive concepts you know carry over with new section numbers. A small selection of common references:

Concept Old Section (Income-tax Act, 1961) New Section (Income-tax Act, 2025) Definitions §2 §2 (re-organised) Previous Year §3 Replaced by Tax Year (definitions clause) Section 80C / 80D / 80G deductions framework Chapter VI-A (§80C onwards) §123 read with Schedule XV (consolidated deductions table) House property — 30 % standard deduction §24(a) Renumbered under the 2025 Act's house-property chapter Presumptive taxation — all three schemes §44AD (eligible business) + §44ADA (specified profession) + §44AE (goods carriages) Consolidated / renumbered under the 2025 Act (broadly under §58) — refer to the CBDT old-vs-new concordance for the exact sub-clause structure before citing Tax audit §44AB §63 of the 2025 Act New tax regime (default) §115BAC §202 of the 2025 Act 87A rebate §87A §156 of the 2025 Act Capital gains — STCG on equity (15 % / 20 %) §111A §196 of the 2025 Act Capital gains — LTCG on equity (12.5 %) §112A §197 of the 2025 Act Capital gains — other LTCG §112 §198 of the 2025 Act Filing of return §139 Renumbered under the 2025 Act's return-filing chapter Updated return (ITR-U) §139(8A) Carried into the 2025 Act with the 48-month window TDS chapter (salary, contractor, professional, property, NRI, etc.) §192 to §196D and §197 to §206C Renumbered into the 2025 Act's TDS chapter (broadly §392 onwards) — refer to the CBDT old-vs-new section concordance for the precise mapping of each TDS provision Repeal of 1961 Act — §536 of the 2025 ActThe atlas above is a partial list. The CBDT has published a detailed concordance on the e-filing portal mapping every old-Act section to its new-Act counterpart. For your AY 2026-27 ITR, you continue to cite the old section numbers — the new numbers apply only to filings for Tax Year 2026-27 onwards.

One thing to be careful about: any guide, blog, FAQ, or YouTube tutorial that is dated after April 2026 and references "Section 58" or "Section 156" is talking about Tax Year 2026-27 and beyond. Do not import those section numbers into your AY 2026-27 ITR — your filing is still under §44ADA and §87A respectively.

7. Pending 1961-Act Matters After 1 April 2026

The savings clause in Section 536 keeps almost everything that started under the 1961 Act on its 1961-Act track. Specifically:

- Reassessments under §147 / §148 of the 1961 Act — notices issued before 31 March 2026 continue under the 1961-Act framework. The block-period / search-and-seizure framework in the 2025 Act applies only to actions initiated on or after 1 April 2026.

- Appeals at CIT(A), ITAT, High Court, Supreme Court — pending appeals continue under the procedural and substantive law as it stood when the appeal was filed. Adverse orders against an old-Act assessment do not require the appellant to re-cast their grounds under the 2025 Act.

- Vivad se Vishwas, 2024 settlements — any taxpayer who opted into the second VsV scheme (declaration window opened in October 2024) processes their declaration, payment, and certificate under the 1961-Act-era VsV machinery; the 2025 Act does not interrupt this.

- Refund claims and rectification applications — refund claims for AY 2025-26 and earlier under §237, and rectification applications under §154, continue under the 1961 Act.

- Carry-forward of losses — capital losses, business losses, speculation losses, and unabsorbed depreciation carried forward from 1961-Act years continue to be available for set-off in Tax Year 2026-27 and onwards under the savings clause. The carry-forward clock does not reset; the 8-year (business loss), 8-year (capital loss), 4-year (speculation loss), and indefinite (unabsorbed depreciation) timelines that started under the 1961 Act continue uninterrupted.

- Section 80C / 80D / 80G investments and donations — eligibility and limits for FY 2025-26 are under the 1961 Act. Investments made on or after 1 April 2026 are claimed under §123 read with Schedule XV of the 2025 Act for Tax Year 2026-27.

8. The Income-tax Rules, 2026 — A Parallel Update

Just as the 1961 Act had the Income-tax Rules, 1962 alongside it, the 2025 Act is partnered with the Income-tax Rules, 2026, notified by CBDT in March 2026 (Notification 22/2026). The structural changes:

- Rule count — reduced from 511 to 333.

- Form count — reduced from 399 to 190. Many forms have been merged, others retired.

- HRA — the 50 % HRA exemption ceiling is expanded beyond the existing four metros (Mumbai, Delhi, Chennai, Kolkata) to a wider notified city list. Effective for Tax Year 2026-27 onwards. (Not retrospective for FY 2025-26 salary; refer to the notified Rules 2026 for the exact city list.)

- PAN-quoting threshold — revised thresholds for transactions where PAN must be quoted (cash deposits, jewellery purchases, fixed deposits, etc.). Effective from 1 April 2026 for Tax Year 2026-27 transactions. Pre-existing thresholds continue to apply for FY 2025-26 transactions.

- Challan forms for Tax Year 2026-27 — CBDT has indicated that revised challan formats apply to tax payments under the 2025 Act for Tax Year 2026-27 onwards. Important practical point: for AY 2026-27 self-assessment / advance-tax / regular-assessment payments (i.e., for FY 2025-26 income), continue using the existing 1961-Act-era challan formats. Confirm the applicable challan format on the e-filing / TIN-NSDL portal before making any payment, since challan formats can change between filing seasons.

- FAQs and Guidance Notes — CBDT has published a "FAQs on Forms as per Income-tax Rules, 2026" document and an "FAQs on Interplay and Transition" document on the e-filing portal. The transition document is the authoritative reference for any ambiguity on which Act / Rule applies to a specific transaction.

9. What Has NOT Changed — Reassurance for the Anxious Taxpayer

The 2025 Act is consolidative, not policy-shifting. The following are unchanged for FY 2025-26 (your current filing) and structurally preserved for Tax Year 2026-27:

- Slab rates for individuals, HUFs, partnerships, LLPs, and companies (subject to whatever the Finance Act of each year provides).

- The presumptive schemes (50 % deemed profit for specified professions; 6 % digital / 8 % cash for eligible business; receipts caps of Rs. 75 lakh / Rs. 3 crore where the cash-receipts test is met) — renumbered, not re-policied.

- Section 80C / 80D / 80G / 80E etc. deduction limits and conditions — re-organised under §123 + Schedule XV in the 2025 Act, with the same monetary limits unless explicitly changed by Finance Act, 2026.

- The new tax regime as the default, with the option to elect into the old regime via Form 10-IEA (business / profession income) or the ITR option (others).

- Capital-gains regimes — STCG / LTCG rates, indexation rules, Section 54 / 54F exemptions, equity grandfathering — unchanged in substance.

- TDS framework — section by section renumbered, but rates, thresholds, and quarterly deposit cycles preserved.

- The ITR family — ITR-1 (Sahaj), ITR-2, ITR-3, ITR-4 (Sugam), ITR-5, ITR-6, ITR-7 — continues with the same broad applicability logic, with annual schema updates by CBDT.

- The e-filing portal infrastructure, login flow, AIS / TIS / Form 26AS reconciliation, and Form 16 issuance cycle — operational continuity maintained.

- Refund processing under §237, intimation under §143(1), scrutiny under §143(2), faceless framework under §144B / §245MA — all preserved (with renumbering for Tax Year 2026-27 onwards).

The CBDT's stated position in its FAQs and press releases is that the 2025 Act largely re-presents existing law without imposing a fundamentally new category of tax. Specific Finance Act 2026 amendments (for instance, changes to the MAT framework and certain rate adjustments) operate from Tax Year 2026-27 onwards, but these are policy moves layered on top of the consolidation rather than the reason for the consolidation. The dominant theme of the transition is structural simplification.

10. Quick FAQ

Q. Should I file my FY 2025-26 ITR under the new Act?

No. FY 2025-26 income is governed by the Income-tax Act, 1961. The ITR for AY 2026-27 (filed by 31 July 2026 / 31 October 2026) is an old-Act filing. Do not import any 2025-Act section numbers into your return.

Q. The new Act is in force on the day I file. Doesn't that move my filing under the new Act?

No. The governing law for a return is determined primarily by the period in which the income arises (i.e., the financial year of earning), not merely by the date on which the return is filed. Income earned during FY 2025-26 falls under the 1961 Act regardless of when the ITR happens to be filed in 2026.

Q. Is "Tax Year 2025-26" a valid label?

No. The Tax Year concept first applies from 1 April 2026. The first Tax Year is Tax Year 2026-27. There is no Tax Year 2025-26. For income of FY 2025-26, the correct label remains AY 2026-27 under the 1961 Act.

Q. My capital losses from AY 2022-23 — do they survive the transition?

Yes. Carry-forward of losses (capital, business, speculative, and unabsorbed depreciation) accrued under the 1961 Act is preserved by the savings clause in Section 536 of the 2025 Act. The original carry-forward periods continue uninterrupted into Tax Year 2026-27 and beyond — broadly: 8 years for business loss and capital loss, 4 years for speculation loss, and indefinite for unabsorbed depreciation, on the same statutory clock that started under the 1961 Act.

Q. I have a pending §148 reassessment notice from December 2025. Does the new Act change anything?

No. Reassessment proceedings initiated under the 1961 Act before 1 April 2026 continue under the 1961-Act framework. The 2025-Act reassessment / search-block provisions apply only to notices issued on or after 1 April 2026.

Q. ITR-U for AY 2024-25 — under which Act?

Under the 1961 Act. ITR-U is a return of income for an earlier AY; it is governed by the same Act that governed that AY. The 48-month window under the 2025 Act-as-amended is a procedural extension, not an Act-change.

Q. Are my §80C investments made in March 2026 still valid for AY 2026-27?

Yes. §80C investments made on or before 31 March 2026 count for FY 2025-26 / AY 2026-27 under the 1961 Act. Investments made on 1 April 2026 onwards count for Tax Year 2026-27 under §123 read with Schedule XV of the 2025 Act.

Q. The new Act has 536 sections. Did the 1961 Act lose 283 sections?

The reduction is largely from consolidation, deletion of obsolete provisions, and removal of provisos / explanations / sub-clauses that bloated the 1961 Act over six decades. The substantive coverage is preserved; the structure is tighter. Many former separate sections are now sub-sections; many former explanations are now schedules.

Q. Do I need to relearn every section number?

For practising professionals and tax preparers, yes — gradually. For most individual taxpayers, no — you continue to interact with the e-filing portal which presents the schedule names and form labels rather than section numbers. The CBDT concordance on the portal will help when you read older case law or commentary.

Q. Will old case law (CIT v. X, AAR rulings, ITAT decisions) still be relevant?

Yes, where the substantive provision is unchanged in spirit. Indian courts have a strong tradition of carrying judicial interpretation across re-enactments where the underlying provision is materially the same. Specific holdings on §80C limits, §44AD audit triggers, capital-gains computation, exemption conditions, and procedural fairness continue to be persuasive under the corresponding 2025-Act sections. Where the 2025 Act materially changes wording, fresh interpretation is needed.

Q. The CBDT FAQs document — where do I find it?

On incometaxindia.gov.in, search for "FAQs on Interplay and Transition" (the authoritative transition guide) and "FAQs on Forms as per Income-tax Rules, 2026". Both are PDF downloads under the Help / Resources section. The "Objective and Scope of the New Act" page on incometax.gov.in (the e-filing portal) is a shorter summary suitable for first-time readers.

11. Statutory and Notification References

- Income-tax Act, 2025 — gazetted as Act No. 30 of 2025; commencement notified for 1 April 2026; consists of 536 sections and 16 schedules.

- Section 536 of the Income-tax Act, 2025 — repeal-and-savings clause for the Income-tax Act, 1961; preserves all rights, obligations, proceedings, and subordinate framework instruments existing on 31 March 2026.

- Income-tax Act, 1961 — Act No. 43 of 1961; in force until 31 March 2026; continues to govern all income earned up to FY 2025-26 and all proceedings initiated on or before 31 March 2026.

- Income-tax Rules, 2026 — notified by CBDT in March 2026 (Notification 22/2026); 333 rules and 190 forms; applicable from 1 April 2026 for Tax Year 2026-27 onwards.

- Income-tax Rules, 1962 — continue to apply to FY 2025-26 income / AY 2026-27 filings, alongside the 1961 Act.

- Finance Act, 2026 — incorporated as amendments to the Income-tax Act, 2025 before commencement on 1 April 2026; effective for Tax Year 2026-27 onwards.

- CBDT FAQs on Interplay and Transition — Income-tax Act, 2025 — published on incometaxindia.gov.in; the authoritative reference for transition-period questions.

- CBDT FAQs on Forms as per Income-tax Rules, 2026 — published on incometaxindia.gov.in; covers ITR forms, challan forms, and the procedural forms under the new Rules.

- "Objective and Scope of the New Act" — incometax.gov.in — short-form summary on the e-filing portal under Help / All Topics / E-filing Services.

- Press Information Bureau release "The Income Tax Act, 2025 to come into effect from 1st April, 2026" — PRID 2221416, the official commencement announcement.

- Section 139, Income-tax Act, 1961 — return-filing due dates for AY 2026-27: 31 July 2026 (non-audit individuals), 31 October 2026 (audit cases), 30 November 2026 (transfer-pricing cases). Belated and revised returns under §139(4) and §139(5) by 31 December 2026.

- Section 139(8A), Income-tax Act, 1961, as amended by Finance Act, 2025 — ITR-U updated-return window of 48 months from the end of the relevant AY.

This guide reflects the position as on 7 May 2026 — five weeks after commencement of the Income-tax Act, 2025 and during the open AY 2026-27 filing window. For complex transition scenarios — partition of HUFs straddling the cut-off, conversion of partnership firms, ESOPs vesting across the cut-off, transfer pricing for FY 2025-26 vs Tax Year 2026-27 — consult a practising chartered accountant or income-tax counsel. Subordinate notifications and CBDT clarifications continue to be issued; check the e-filing portal and the CBDT FAQs for the latest position before relying on any specific transition outcome. Nothing in this article is a substitute for professional advice.

Comments (0)

No comments yet. Be the first to comment!