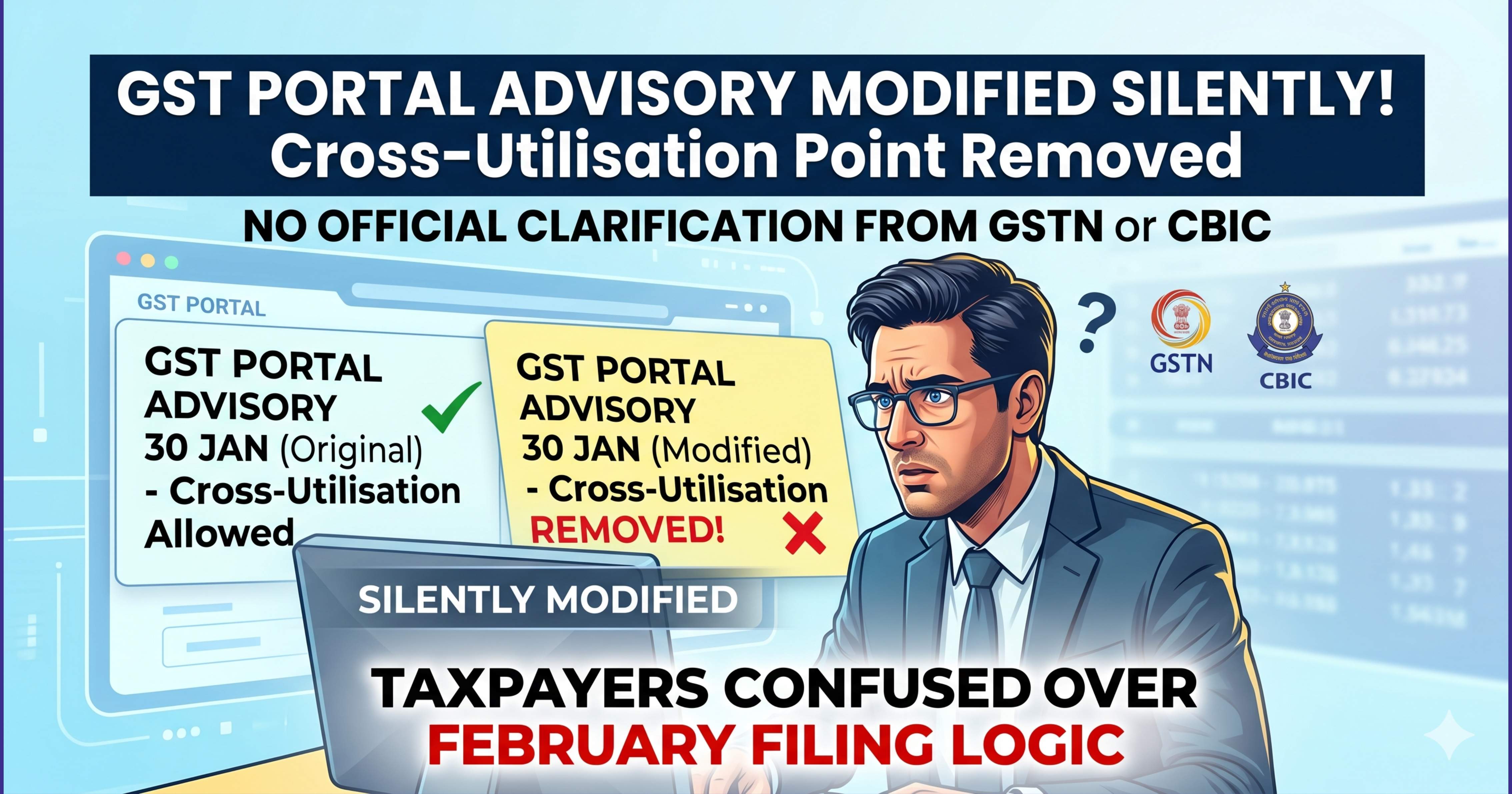

The Income-tax Department has introduced a new unified Form 141, which is now available on the e-filing portal under the e-Pay Tax section. This form is positioned as a consolidated replacement for the earlier Forms 26QB, 26QC, 26QD and 26QE, which were used for reporting tax deducted at source (TDS) on specified transactions.

Historically, different forms applied to different types of payments:

- Form 26QB for TDS on purchase of immovable property

- Form 26QC for TDS on rent by certain individuals/HUFs

- Form 26QD for TDS on payments to resident contractors and professionals

- Form 26QE for TDS on payments to non-residents under specific provisions

This multiplicity of forms often created confusion among taxpayers, especially individuals and small taxpayers who are not regularly engaged in tax compliance activities.

With the introduction of Form 141, the government appears to be moving towards standardisation and simplification of compliance. The form is described on the portal as a “Challan-cum-statement of deduction of tax under section 393(1)”, covering multiple transaction categories through a single interface.

From a practical standpoint, this change can offer several advantages:

- Reduced compliance complexity, as taxpayers no longer need to identify and select different forms

- Uniform reporting structure, leading to better consistency in filings

- Simplified navigation on the e-filing portal, as seen in the updated e-Pay Tax dashboard

However, it is important to note that while the form has been unified, the underlying tax provisions, thresholds, and rates applicable to different transactions may continue as per the law. Taxpayers must still ensure correct classification of transactions within the form and apply the appropriate provisions.

The availability of Form 141 on the portal also indicates a transition towards a more integrated compliance system, possibly aligned with broader changes under the evolving Income-tax framework.

Tax professionals should closely monitor detailed instructions, utility updates, and any notifications issued by the CBDT to understand the full scope, validation rules, and reporting requirements under this new form.

For now, Form 141 marks a significant structural shift in TDS reporting for specified transactions, aimed at making compliance more streamlined while maintaining regulatory oversight.

Comments (0)

No comments yet. Be the first to comment!