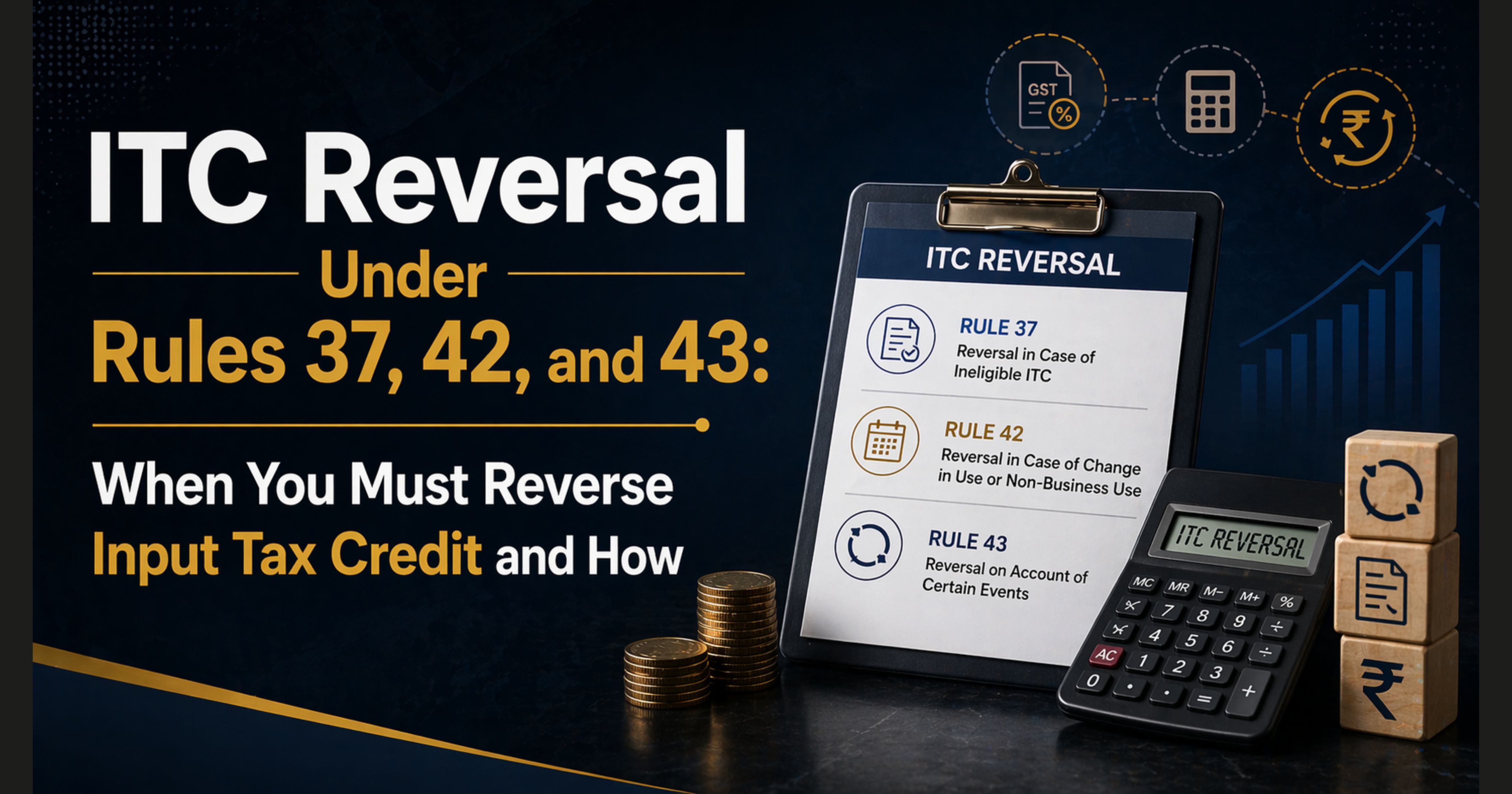

Why ITC Reversal Exists

Claiming Input Tax Credit is not the end of the story. Three rules in the CGST Rules — Rule 37, Rule 42, and Rule 43 — carve out circumstances where credit already availed must be reversed and paid back, either temporarily or permanently.

ITC reversal rules ensure that credit is retained only when underlying conditions — payment, usage, and tax compliance — are satisfied.

Each rule covers a distinct trigger:

- Rule 37 — non-payment to the supplier within 180 days

- Rule 42 — credit used for exempt supplies (inputs and input services)

- Rule 43 — credit on capital goods partly used for exempt supplies

Ignoring any of these leads to reversal notices with interest — and in some cases, penalty.

Rule 37 — Non-Payment to Supplier Within 180 Days

What the Rule Says

Under Section 16(2) second proviso, read with Rule 37, if a recipient fails to pay the supplier the invoice value plus tax within 180 days from the date of the invoice, the ITC earlier claimed must be reversed.

When the Reversal Must Be Reported

- In the GSTR-3B of the tax period following the expiry of 180 days

- The reversed amount is added to the output tax liability

- Interest is payable under Section 50 if the ITC has been utilised, from the date of utilisation till the date of reversal

When You Can Re-Claim

Once the payment is actually made to the supplier, the reversed ITC can be re-availed in the GSTR-3B of the period in which payment is made. Re-availment is generally treated as restoration of previously reversed credit and is not subject to the Section 16(4) time limit, based on CBIC clarifications.

Common Traps

- Part payments — pro-rata reversal applies to the unpaid portion

- Supplier credit notes — reduce the amount "owed" for 180-day purposes

- Related-party transactions — where book entries substitute for actual payment, careful documentation is needed

- 180 days from the invoice date, not from the supply date — this catches a lot of practitioners

Rule 42 — Reversal for Inputs and Input Services Used in Exempt Supplies

Who This Applies To

Rule 42 applies when a registered person uses inputs or input services for both taxable and exempt supplies — or for both business and non-business purposes. You cannot claim 100% credit when part of the usage goes toward exempt output.

The Formula (Simplified)

Rule 42 requires:

- T1 — inputs/services used exclusively for non-business purposes → 100% reversal

- T2 — inputs/services used exclusively for exempt supplies → 100% reversal

- T3 — inputs/services where credit is blocked under Section 17(5) → 100% reversal

- T4 — inputs/services used exclusively for taxable supplies (including zero-rated) → fully eligible, no reversal

- Common credit (C2) — remaining credit → apportioned between taxable and exempt using the formula:

D1 = (E ÷ F) × C2

Where:

- E = aggregate value of exempt supplies during the tax period

- F = total turnover during the tax period

- D1 = amount to be reversed

An additional D2 = 5% of C2 is reversed towards non-business use, where such use cannot be specifically identified.

Annual True-Up

At year-end, the monthly Rule 42 reversals are compared against a full-year recomputation. If the monthly reversals fell short, the shortfall is paid with interest. If excess, it can be re-claimed.

Where to Report

- Monthly reversal → GSTR-3B Table 4B(1) — "As per rules 38, 42 and 43 of CGST Rules"

- Annual true-up → by 30 November of the following financial year (or annual return filing, whichever earlier)

Rule 43 — Reversal for Capital Goods Used in Exempt Supplies

Who This Applies To

Rule 43 covers capital goods whose credit was originally claimed in full, but which are used partly for exempt supplies or partly for non-business purposes. Full ITC is claimed upfront, but adjusted over time through proportionate reversal.

The Mechanism (Simplified)

- Useful life of capital goods for GST purposes is 60 months (5 years) from invoice date

- Monthly credit attributable to the capital goods = total ITC ÷ 60

- The exempt-supplies portion of each month's capital credit must be reversed using a formula similar to Rule 42:

Tm = Tc ÷ 60, where Tc is the common credit on capital goods

Monthly reversal = (E ÷ F) × Tm

Where to Report

- Same row as Rule 42: GSTR-3B Table 4B(1)

- The calculation must be maintained separately in the accounts records

Change in Use

If a capital good originally used for taxable supplies is later used partly for exempt supplies, the remaining useful life (out of 60 months) is the base for the reversal calculation. Records of the switch date are critical.

Other Reversals to Know (Brief)

Beyond Rules 37, 42, 43, practitioners should also be aware of:

- Section 17(5) — blocked credits (motor vehicles, food, personal use, etc.) — no ITC can be claimed in the first place; if mistakenly claimed, reverse

- Rule 44 — reversal when a registered person opts out of GST, cancels registration, or shifts to the composition scheme

- Rule 37A — addresses cases where the supplier has not discharged tax liability within the prescribed timeline, requiring reversal in specified situations

Interest on ITC Reversals

Interest on ITC reversals generally applies at 18% p.a., depending on whether the reversal results in additional tax liability or involves wrongful utilisation of credit:

- Where the wrongly availed credit has been utilised, interest is typically payable from the date of utilisation

- Where the wrongly availed credit has not been utilised (remained in the electronic credit ledger), interest may not apply — but non-utilisation should be carefully documented

- Section 50 governs the interest framework; Section 50(1) covers delay in tax payment, and Section 50(3) covers wrongful ITC utilisation

Where Everything Lands in GSTR-3B

Reversal Type GSTR-3B Reporting Row Rule 37 (180 days) Table 4B(2) — "Others" Rule 42 (inputs/services, exempt) Table 4B(1) Rule 43 (capital goods, exempt) Table 4B(1) Rule 44 (deregistration, composition) Form ITC-03 + GSTR-3B Rule 37A (supplier non-payment) Table 4B(2)

Common Mistakes Practitioners Should Avoid

- Tracking 180 days from supply date instead of invoice date — Rule 37 runs from the invoice date

- Forgetting the year-end true-up under Rule 42 — monthly estimates rarely match the full-year ratio

- Treating zero-rated exports as exempt — they are not exempt for Rule 42/43 purposes (Section 16 of IGST Act)

- Missing Rule 43 monthly reversal on capital goods where one-time full credit was claimed

- Not paying interest alongside reversal where credit was utilised — Section 50 interest is mandatory in such cases

Audit and Documentation Checklist

- Maintain a 180-day ageing register for every unpaid purchase invoice

- Maintain a monthly Rule 42 / Rule 43 computation workbook with E, F, T1-T4, D1, D2

- Track all capital goods by invoice date, 60-month expiry, and exempt-use switchover dates

- Reconcile reversals in books with GSTR-3B Table 4B rows every quarter

- File the annual true-up no later than 30 November of the following financial year

- Authorities increasingly verify Rule 42/43 workings during audits — maintaining working papers is critical

Bottom Line

ITC is not a one-way door. Rule 37 polices cash flow to your suppliers. Rules 42 and 43 police the exempt-supply leak. The rules are mechanical, but the interest clock is unforgiving when credit has been utilised. A monthly reversal workflow that runs alongside your GSTR-3B preparation — not after — is the only way to stay audit-clean without surprise liability at year-end.

Comments (0)

No comments yet. Be the first to comment!