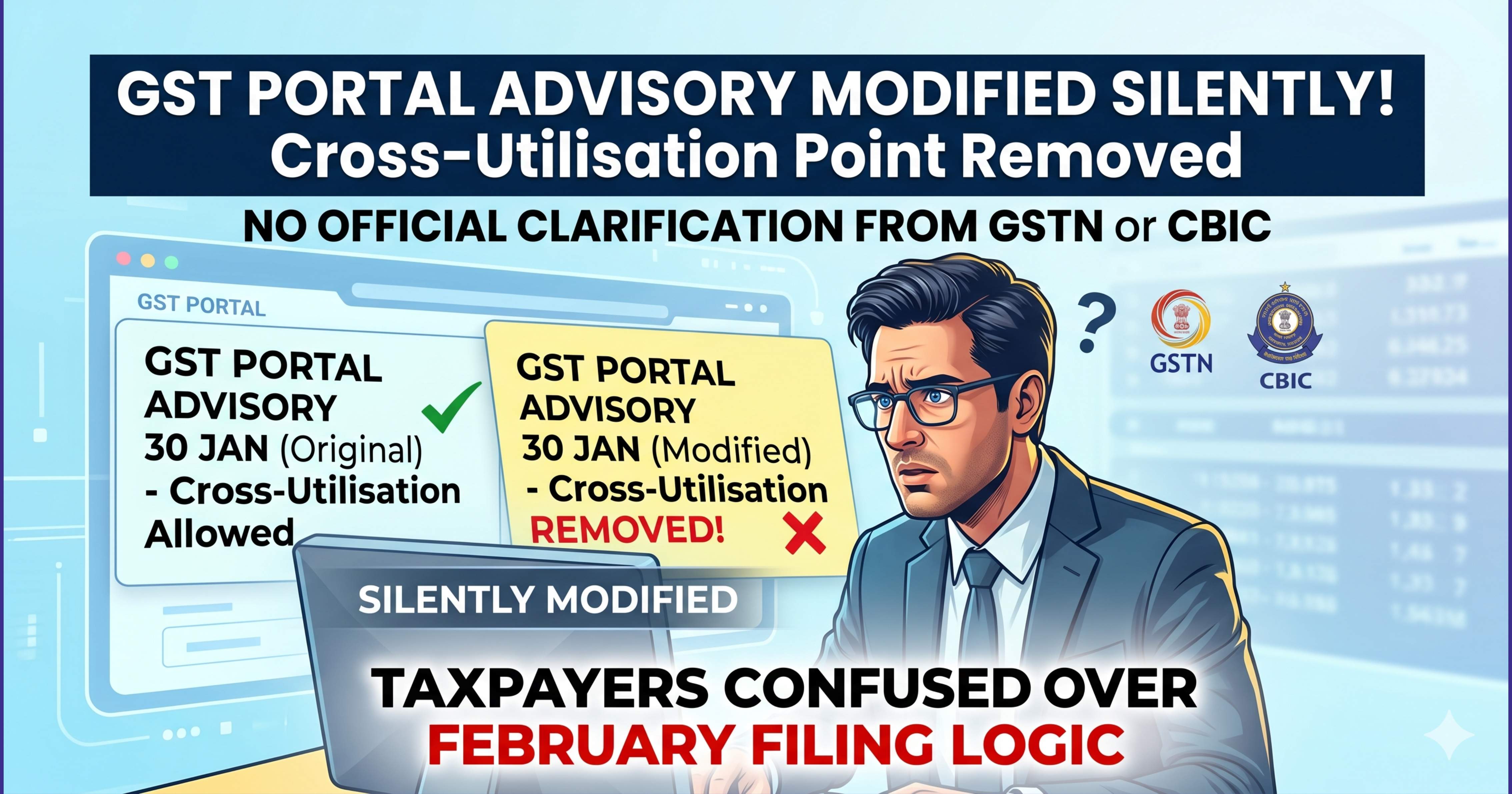

GSTN’s advisory dated 30 January 2026 (Advisory No. 647) on interest computation and GSTR-3B enhancements has become a topic of discussion among Chartered Accountants and tax professionals.

Three key aspects require attention.

1. Original Advisory (as reported on 30–31 January)

Professional publications and initial summaries of the advisory documented four enhancements:

- Revised interest computation aligned with Rule 88B(1)

- Auto-population of Tax Liability Breakup Table

- Flexibility to utilise CGST/SGST ITC for IGST (after exhausting IGST ITC)

- Interest recovery via GSTR-10 for cancelled taxpayers

The flexibility in point 3 is aligned with Sections 49A, 49B and Rule 88A.

2. Implementation on Portal

During January 2026 filings, taxpayers encountered error LG9079, which required:

Full utilisation of CGST before using SGST against IGST

This was not aligned with the flexibility described above.

Subsequently, GSTN issued Advisory No. 649 (19 February 2026) clarifying that:

- The flexibility would apply from February 2026 period onwards

3. Current Version of Advisory

The advisory currently available on the GST portal reflects three points, and the ITC cross-utilisation reference is not present in the current version.

At the time of writing, no separate clarification or communication has been issued explaining this difference.

Why This Matters

- Professionals are facing uncertainty between advisory, portal behaviour, and legal provisions

- Questions arise regarding treatment of February filings

- Consistency in official communication becomes critical for compliance confidence

Conclusion

The issue highlights the importance of alignment between advisory, system implementation, and statutory provisions.

A clarification from GSTN on:

- Current status of ITC utilisation flexibility

- Position for past filings

- Updated advisory intent

would help remove ambiguity.

Until then, professionals should rely on statutory provisions and verify portal behaviour before finalising returns.

Comments (0)

No comments yet. Be the first to comment!