Form 16 to ITR Filing for Salaried — Step-by-Step Guide for AY 2026-27 (FY 2025-26)

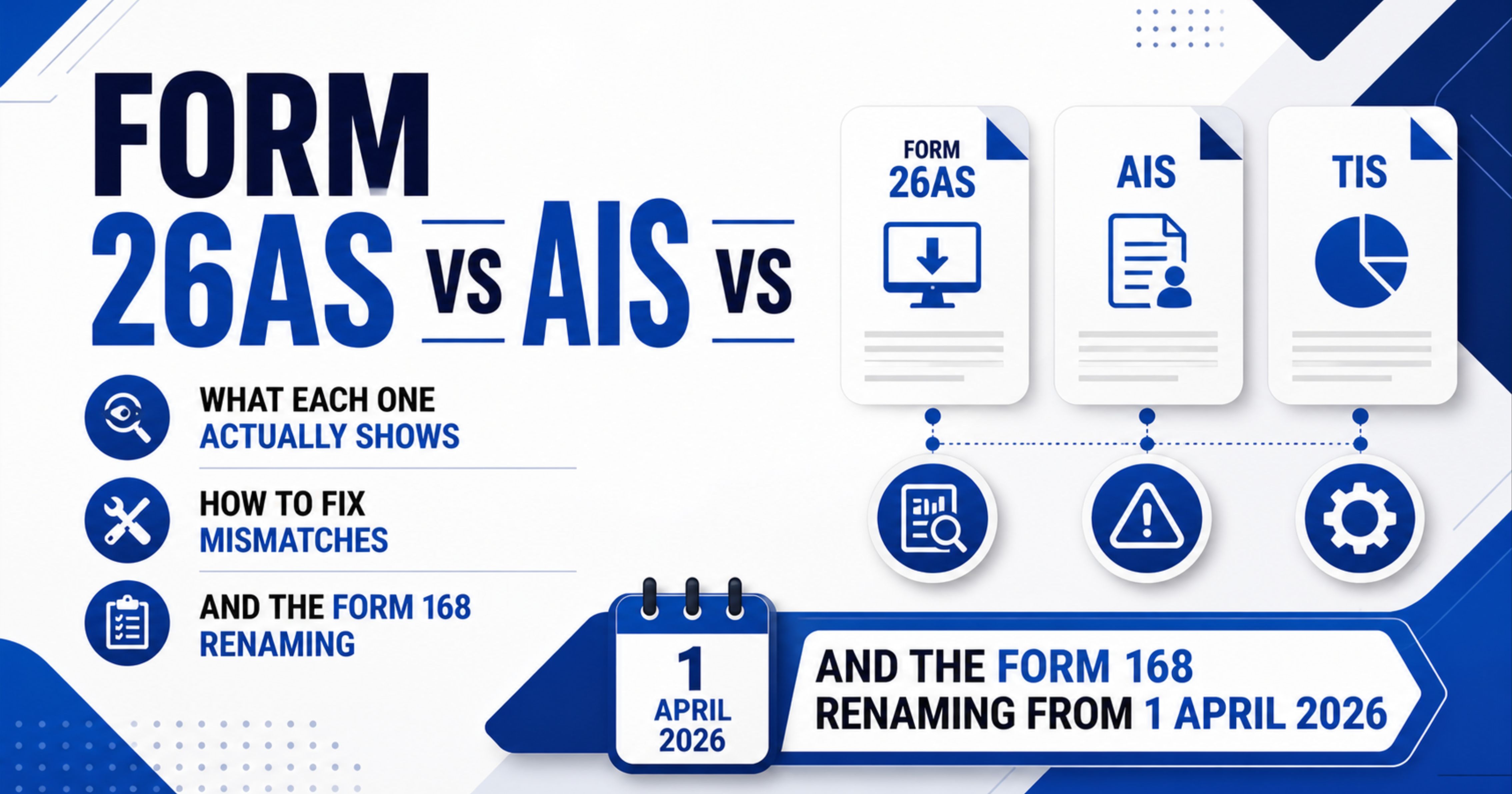

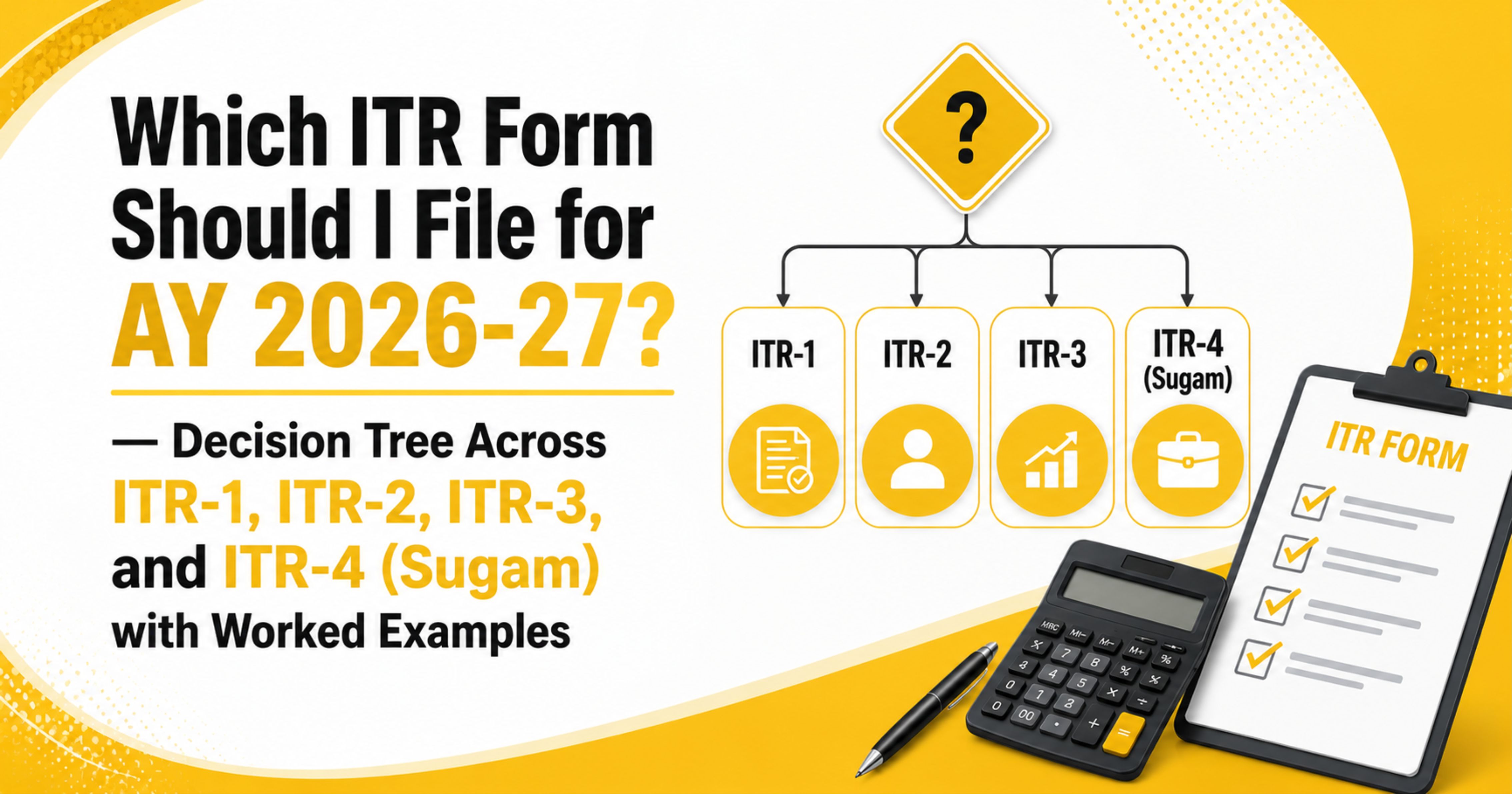

Step-by-step walk-through for salaried India: read Form 16 (Section 203 + Rule 31), reconcile with Form 26AS/AIS/TIS, pick ITR-1 (now allows two house properties + LTCG up to Rs.1.25L), choose new vs old regime, claim Sec 87A rebate (Rs.60K up to Rs.12L), and e-Verify in 30 days. Due 31 July 2026.

Priya Rao

@pf_priya

Decoding money for salaried India — budgeting, debt, first-time investing. Based in Delhi.