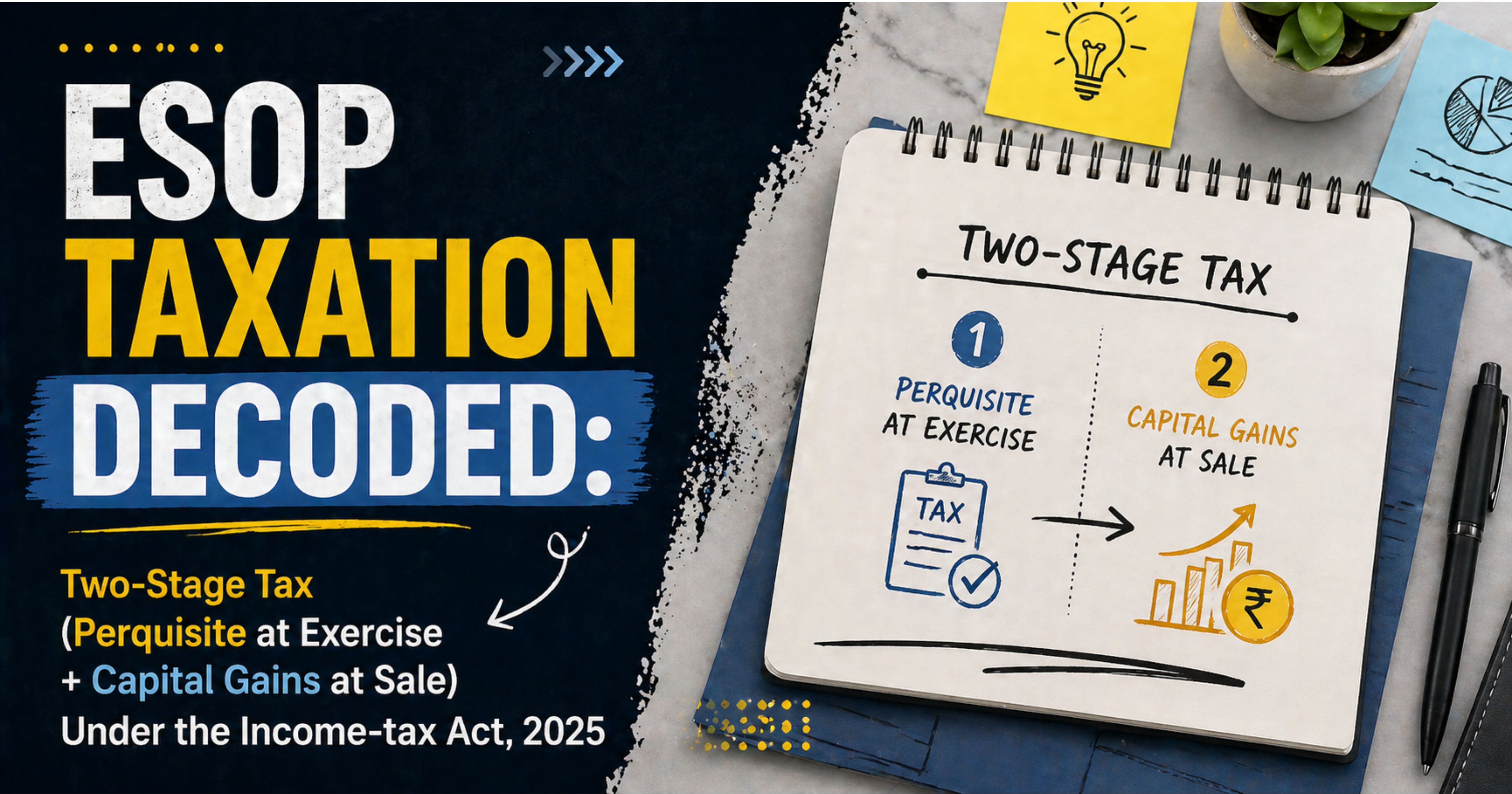

TL;DR: Under the Income-tax Act, 2025 (effective Tax Year 2026-27), ESOPs are taxed at two stages, exactly as under the 1961 Act — only the section numbers have changed. Stage 1 is at exercise: the gap between the share's fair market value on the exercise date and the price you paid is your salary perquisite under Section 17(1)(d) read with the FMV formula in Section 17(5)(h), taxed at slab rates. Stage 2 is at sale: the gap between your sale price and the FMV-on-exercise (your new cost base) is capital gain, taxed at the post-Budget-2024 rates — 12.5% LTCG / 20% STCG for listed, 12.5% LTCG / slab STCG for unlisted. Eligible-startup employees can defer the Stage 1 tax under Section 392(3) read with Section 289(3) for up to 60 months (up from 48), or until sale or job exit, whichever comes first.

The 30-Second Summary

ESOPs look like equity but get taxed first as salary, then as investment. Most employees lose money on the deal not because the stock didn't appreciate, but because they didn't budget for the cash tax bill at exercise — especially in unlisted companies where there is no liquid market to sell into. Understanding the two-stage rule is what separates an ESOP that builds wealth from one that lands you with a tax bill on paper gains you cannot convert.

1. Why ESOPs Are Taxed Twice

An ESOP is a contractual right to buy your employer's shares at a pre-fixed exercise price after a vesting period. There is no tax at grant (no transfer has happened), no tax at vesting (you have only earned the right to buy). The two taxable events are:

- Exercise — you actually pay the exercise price and the company allots shares to you. The notional gain (FMV minus exercise price) is your salary perquisite.

- Sale — you sell the shares (whether immediately, after a holding period, or in a tender / buy-back). The gain over your FMV-on-exercise cost base is capital gain.

The double-event design is deliberate: at exercise, the law treats the employer—employee compensation; at sale, it treats the investor—market relationship. Each gets its own slab, its own cost base, and its own residency-test rules.

2. Stage 1 — Perquisite at Exercise (Section 17(1)(d))

Section 17(1)(d) of the Income-tax Act, 2025 includes within "perquisite" the value of any specified security or sweat equity shares allotted or transferred, directly or indirectly, by the current or former employer, free of cost or at concessional rate, to the assessee. This is the renumbered successor to Section 17(2)(vi) of the 1961 Act — substantively unchanged.

The valuation formula is in Section 17(5)(h): the value of any specified security or sweat equity share is the fair market value on the date of exercise, as reduced by the amount actually paid by, or recovered from, the employee.

Stage 1 Perquisite = (FMV on exercise date − Exercise price) × Number of shares exercised

Determining FMV

Type of share FMV rule Listed on a recognised Indian stock exchange Average of opening and closing market prices on exercise date (per Rule 3(8) of the 1962 Rules; carried forward into the 2026 Rules) Unlisted FMV determined by a Category I merchant banker registered with SEBI, on a date not earlier than 180 days from the exercise date Foreign-listed (e.g., parent company on NASDAQ) Closing price on the foreign exchange on exercise date, converted to INR at the SBI TT buying rate (or as specified in the relevant rule)How the tax actually flows

The perquisite is added to your "Salary" income for the tax year of exercise. Your employer:

- Treats the perquisite as part of your taxable salary for the year.

- Deducts TDS under Section 392(1) of the 2025 Act (was Section 192 of 1961 Act) on the entire salary including this perquisite.

- Optionally, under Section 392(2) (was Section 192(1A)), the employer may pay the tax on the non-monetary perquisite from its own funds rather than deducting from your salary — this is the "ESOP tax loan" some companies offer; you reimburse the employer later.

The exercise-stage cash flow trap: you have paid the exercise price, the employer has deducted TDS on the perquisite, but you still hold illiquid shares (especially in unlisted companies). Many employees discover at this point that they need to either sell some of the allotted shares to a secondary buyer (where permitted), borrow, or cease exercising further options.

3. Stage 2 — Capital Gains at Sale

When you eventually sell the ESOP shares, you trigger a capital gain or loss:

Stage 2 Capital Gain = Sale price − FMV on exercise date − Allowable expenses

Note: the cost base is the FMV on exercise date, not what you paid. The Stage 1 perquisite has already taxed the gap between exercise price and FMV. To tax the gap again at Stage 2 would be double taxation.

Holding period and rates — post Budget 2024 regime

The Finance (No. 2) Act, 2024 rationalised capital gains across the board. For transfers on or after 23 July 2024 (so for FY 2024-25 onwards):

Type of share Holding period for LTCG STCG rate LTCG rate Listed equity (Indian) where STT is paid on sale More than 12 months 20% (Section 196 of 2025 Act, was Section 111A) — was 15% pre-Budget-2024 12.5% (Section 198 of 2025 Act, was Section 112A) on gains above Rs. 1,25,000 per year — was 10% above Rs. 1 lakh Unlisted equity (Indian) More than 24 months Slab rate (added to total income) 12.5% (Section 197 of 2025 Act, was Section 112) — indexation removed for transfers on or after 23 July 2024 Foreign-listed equity (e.g., NASDAQ, NYSE, LSE) More than 24 months Slab rate 12.5% (Section 197 of 2025 Act, was Section 112) — indexation not applicableFor listed shares, you pay STT (Securities Transaction Tax) on sale, and the concessional Section 196 / 198 rates apply (formerly Section 111A / 112A). For unlisted shares (including foreign-listed) STT does not apply, and the residual Section 196 is unavailable — STCG is taxed at slab rates.

The cost-base anchor in IPO scenarios

If the company was unlisted at the time of exercise but is listed at the time of sale, your cost base remains the FMV-on-exercise of the unlisted era, but your sale benefits from the listed-equity 12-month holding period running from the listing date. This is one of the cleanest ways ESOP wealth crystallises — the shares are perq-taxed at a low unlisted FMV, then sold at the post-IPO market price.

4. The Eligible-Startup Deferral — Section 392(3) read with Section 289(3)

The Stage 1 cash-tax problem is most acute at unlisted startups, where employees pay tax on illiquid paper. To address this, the law provides a deferral window for employees of eligible startups.

Who is an "eligible startup"?

An "eligible startup" under Section 140 of the Income-tax Act, 2025 (was Section 80-IAC of the 1961 Act) is a company that:

- is recognised by the Department for Promotion of Industry and Internal Trade (DPIIT) as a startup, AND

- holds a valid Inter-Ministerial Board (IMB) Certificate of eligible business under Section 140 / 80-IAC.

Of the ~1.9 lakh DPIIT-recognised startups as of April 2025, only about 3,700 hold the IMB Certificate. DPIIT recognition alone is not enough. This is the most common practitioner mistake.

What the deferral does

Under Section 392(3) of the 2025 Act read with Section 289(3) (successor to Section 192(1C) of the 1961 Act), an eligible startup is allowed to defer deduction or payment of tax on the Stage 1 perquisite. For shares allotted on or after 1 April 2026, the deferral window is 60 months (extended from 48 months under the 1961 Act) from the end of the tax year of allotment.

The deferred tax becomes payable at the earliest of:

- 60 months from the end of the tax year of allotment, OR

- The date of sale of the specified security or sweat equity share, OR

- The date on which the assessee ceases to be an employee of the issuer.

The tax is calculated at the rates in force for the year of allotment, not the year in which deferral ends — so a slab-rate change between exercise and trigger does not retrospectively help or hurt the employee.

Practical use: the deferral is most valuable when (a) the employee plans to stay at the company, (b) the company has not yet listed, and (c) the employee expects to time the sale alongside a liquidity event (IPO, secondary tender, acquisition). It does not reduce the tax owed; it postpones it.

5. Worked Examples

Example A — Listed Indian Company (no startup deferral)

Profile: Reema, software engineer at a listed Indian co. Exercise price Rs. 100. FMV on exercise date Rs. 1,000. 5,000 shares. Sells all on day 200 after exercise at Rs. 1,400.

Stage 1 (year of exercise): Perquisite = (1,000 − 100) × 5,000 = Rs. 45,00,000. Added to salary; taxed at slab; employer deducts TDS under Section 392(1).

Stage 2 (sale 200 days later, holding < 12 months ⇒ STCG): Capital gain = (1,400 − 1,000) × 5,000 = Rs. 20,00,000. Taxed at 20% under Section 196 of the 2025 Act (was Section 111A) ⇒ tax Rs. 4,00,000 + cess.

Total cash needed: exercise price Rs. 5,00,000 (paid upfront); Stage 1 tax depends on slab, can be paid via TDS withholding; Stage 2 tax of Rs. 4,00,000+ payable on sale.

Example B — Unlisted DPIIT-IMB Startup (with deferral)

Profile: Arjun, product manager at a 4-year-old unlisted startup with a valid Section 140 / Section 80-IAC IMB Certificate. Exercise price Rs. 50. SEBI merchant-banker FMV on exercise date Rs. 500. 10,000 shares. Stays employed for 4 years, then sells on a secondary at Rs. 1,200.

Stage 1 perquisite (year of exercise): (500 − 50) × 10,000 = Rs. 45,00,000. Deferred under Section 392(3) read with Section 289(3) — employer does not deduct TDS, employee does not pay self-assessment tax, in the year of exercise.

Trigger: Arjun sells on year 4. The deferred Stage 1 tax becomes payable now (sale date is the earliest of the three triggers). Tax on Rs. 45,00,000 at slab rates of the year of allotment (not year of sale) is collected via the standard Section 392 / Section 289 mechanism.

Stage 2 capital gain: (1,200 − 500) × 10,000 = Rs. 70,00,000. Holding from exercise date to sale date is over 24 months ⇒ LTCG ⇒ 12.5% under Section 197 of the 2025 Act (was Section 112) ⇒ tax Rs. 8,75,000 + cess. (No indexation under post-23-July-2024 regime.)

Without the deferral, Arjun would have had to fund the Stage 1 tax cash-out four years earlier, possibly by selling shares he could not legally sell at that point.

Example C — Foreign Parent Listed on NASDAQ

Profile: Sneha, India-resident employee of a US tech firm's Indian subsidiary, granted parent-company RSUs / ESOPs. Exercise price USD 0 (typical RSU). FMV on vesting date USD 200 per share × INR 84/USD × 100 shares = Rs. 16,80,000.

Stage 1 perquisite: Rs. 16,80,000. Indian subsidiary is the "employer" for Section 17(1)(d) purposes and deducts TDS under Section 392(1) on the INR-equivalent perquisite value.

Stage 2 capital gain: When Sneha later sells on NASDAQ at USD 250, the INR sale consideration (at the prevailing rate) minus the INR-equivalent FMV-on-vesting cost base is the capital gain. Since the shares are not listed in India, Section 196 / 198 (formerly Section 111A / 112A) do not apply — STCG is at slab if held less than 24 months, LTCG is at 12.5% under Section 197 (formerly Section 112) if held more than 24 months. Foreign-tax-credit relief under the India-US DTAA may be available for any US tax suffered.

NRIs / RNORs and the Sneha-style cross-border ESOP structures need a Schedule FA / FA-related disclosure on the ITR; missing this is a frequent compliance gap.

6. Common ESOP Tax Mistakes

- Treating Stage 1 as "deferred till sale." Without an eligible-startup IMB certificate, there is no statutory deferral. The Stage 1 perquisite hits in the year of exercise regardless of whether you can sell.

- Assuming DPIIT recognition = Section 140 / Section 80-IAC eligibility. It does not. Only ~2% of DPIIT-recognised startups hold the IMB Certificate that triggers the deferral.

- Using exercise price as Stage 2 cost base. Wrong — the cost base is FMV-on-exercise, not what you paid. Using the lower exercise price double-taxes the perquisite portion.

- Ignoring listed-vs-unlisted holding-period asymmetry. Listed equity LTCG kicks in at 12 months; unlisted at 24 months. Selling unlisted shares at month 18 means slab-rate STCG, not 12.5% LTCG.

- Forgetting that Stage 1 indexes to the year of allotment, not year of trigger. Even when deferral is used, slab rates of the allotment year apply. A move to the new regime mid-deferral does not reduce the historical liability.

- Foreign-parent ESOPs without Schedule FA disclosure. Indian residents holding foreign assets must report them in Schedule FA / FA every year — an omission can attract penalty under the Black Money Act.

- Not modelling the cash-flow gap. The Stage 1 tax bill is real cash, due at exercise, even if the shares are illiquid. Model it before you exercise, not after.

- Selling listed equity within 12 months of exercise. 20% STCG on the post-exercise gain. If you can wait one more month past month 12, the gain becomes 12.5% LTCG (above the Rs. 1.25 lakh annual exemption).

7. The Cash-Flow Decision Framework

Before exercising, model these four numbers:

- Exercise price × shares — the cash you pay to the company.

- Stage 1 tax — slab rate × (FMV − exercise price) × shares. For a 30%-slab employee at a Rs. 1 crore perquisite, this is Rs. 30 lakh in cash.

- Liquidity timing — when can you actually sell? IPO date, secondary tender date, acquisition close.

- Stage 2 expected gain — and the LTCG vs STCG threshold (12 / 24 months from exercise date).

If items 1 + 2 exceed the cash you have available, you cannot afford to exercise on this schedule — even if you "win" the bet on the share price. The single biggest reason employees lose money on ESOPs is over-exercising without a liquidity bridge.

Eligible-startup employees have an extra option: defer Stage 1 under Section 392(3) for up to 60 months. This converts the perquisite tax into a quasi-loan from the government — payable when you sell, leave, or hit the 60-month wall.

8. Bottom Line

The two-stage ESOP rule has not changed in substance from 1961 to 2025 — only the section numbers have. Section 17(1)(d) read with Section 17(5)(h) anchors the perquisite valuation at exercise; Section 392 governs the TDS mechanics; Section 392(3) read with Section 289(3) extends the eligible-startup deferral to 60 months for shares allotted on or after 1 April 2026. Stage 2 capital gains follow the post-Budget-2024 regime, with FMV-on-exercise as the cost base.

The win condition is simple: model the Stage 1 cash bill before you exercise, time the Stage 2 sale on the right side of the holding-period cliff, and use the eligible-startup deferral when it is available. The losing condition is just as simple: exercise into illiquid paper without budgeting for the salary perquisite tax, then sell early at an STCG rate. The choice is yours, and it is made before you click the "exercise" button.

9. Legal References

- Income-tax Act, 2025 — effective Tax Year 2026-27 (1 April 2026).

- Section 17(1)(d), Income-tax Act, 2025 — value of any specified security or sweat equity share allotted or transferred by employer at concessional rate to assessee, included in "perquisite". Successor to Section 17(2)(vi) of the 1961 Act.

- Section 17(5)(h), Income-tax Act, 2025 — valuation rule: FMV on exercise date minus amount paid by/recovered from the employee. Successor to Rule 3(8) read with Section 17(2)(vi) of the 1961 Act.

- Section 392(1), Income-tax Act, 2025 — TDS on salary by the employer at the average rate of income-tax computed on the rates in force for the tax year. Successor to Section 192 of the 1961 Act.

- Section 392(2), Income-tax Act, 2025 — employer's option to pay tax on non-monetary perquisites without deducting from employee. Successor to Section 192(1A) of the 1961 Act.

- Section 392(3) read with Section 289(3), Income-tax Act, 2025 — eligible-startup ESOP perquisite tax deferral; window 60 months from the end of the tax year of allotment for shares allotted on or after 1 April 2026, OR earliest of date of sale OR cessation of employment. Successor to Section 192(1C) of the 1961 Act (which had a 48-month window).

- Section 140, Income-tax Act, 2025 — eligible startup definition for the deferral and 100% profit-deduction holiday. Successor to Section 80-IAC of the 1961 Act. Requires DPIIT recognition + IMB Certificate.

- Section 196, Income-tax Act, 2025 — 20% STCG on listed equity where STT is paid on sale. Successor to Section 111A of the 1961 Act. Rate revised from 15% to 20% by Finance (No. 2) Act, 2024 for transfers on or after 23 July 2024.

- Section 198, Income-tax Act, 2025 — 12.5% LTCG on listed equity above Rs. 1,25,000 annual exemption. Successor to Section 112A of the 1961 Act. Rate revised from 10% to 12.5% and exemption raised from Rs. 1 lakh to Rs. 1.25 lakh by Finance (No. 2) Act, 2024.

- Section 197, Income-tax Act, 2025 — 12.5% LTCG on other long-term capital assets including unlisted shares. Successor to Section 112 of the 1961 Act. Indexation benefit removed for transfers on or after 23 July 2024 (with limited grandfather for resident transfers of pre-23-July-2024 land/buildings).

- Finance (No. 2) Act, 2024 and CBDT FAQ on the new capital gains regime (PIB Press Release dated 23 July 2024) — rate and holding-period changes effective 23 July 2024.

- CBDT Tutorial — Taxation of Employee Stock Option Plan (ESOP), incometaxindia.gov.in/Tutorials/50.

- Old-Act anchors: Section 17(2)(vi); Rule 3(8) and Rule 3(9) of the Income-tax Rules, 1962; Section 192 / 192(1A) / 192(1C); Section 80-IAC of the Income-tax Act, 1961.

For high-stakes ESOP decisions — a six-figure exercise, an IPO-window sale, an India-to-foreign or foreign-to-India residency change between exercise and sale, or a startup whose IMB-certificate status is unclear — consult a Certified Financial Planner and a chartered accountant. Confirm exact section text, latest CBDT clarifications, and the company's specific ESOP scheme document before relying on this summary.

Comments (0)

No comments yet. Be the first to comment!