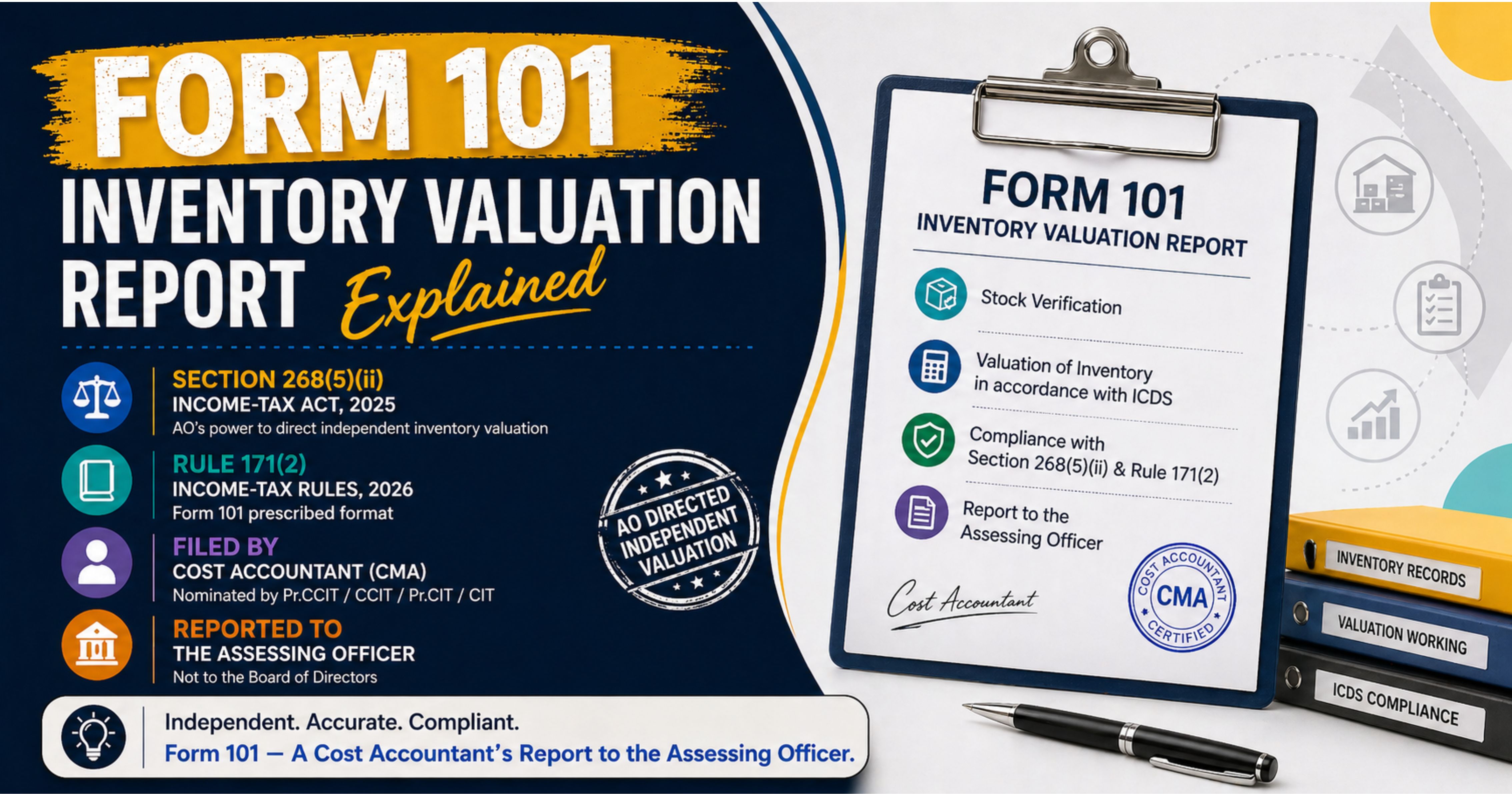

TL;DR: The Income Tax Department has notified Form No. 101 under Rule 171(2) of the Income-tax Rules, 2026 — the new Inventory Valuation Report that replaces the earlier Form 6D (notified in September 2023). It is triggered only when an Assessing Officer, drawing on the enabling power in Section 268(5)(ii) of the Income-tax Act, 2025, directs an assessee to get inventory independently valued by a Cost Accountant nominated by the competent income-tax authority. This is not a routine annual filing — it is a special, AO-triggered compliance with a hard six-month outer limit and material consequences.

The 30-Second Summary

Form 101 lands on a client’s desk only when the AO concludes that inventory needs an independent professional re-valuation. The Cost Accountant is nominated by the income-tax authority — not freely chosen by the taxpayer — and the certified report goes back to the AO as the independent benchmark against which the assessee’s own figures are tested.

Here is what every practising CA needs to know.

1. Why Form 101 Exists: The Bigger Picture

Inventory has historically been one of the softest areas of corporate accounts — easy to manipulate, hard to verify, and rarely scrutinised in depth during ordinary scrutiny assessments. Under the old Income-tax Act, 1961, Section 145A governed inventory valuation, and the standard reporting flowed through tax audit disclosures and ICDS II.

The Income-tax Act, 2025 has restructured this entirely into a three-tiered framework:

Layer Provision What It Does Substantive Standard Section 277 Lays down the overarching valuation standard, including for inventory — anchored to “lower of cost or NRV” as per ICDS, with category-wise comparison and inclusion of taxes/duties to bring goods to current location. Enabling Power Section 268(5)(ii) Empowers the AO — with prior approval of the Pr.CCIT/CCIT/Pr.CIT/CIT — to direct an independent inventory valuation. Operational Mechanism Rule 171(2) + Form No. 101 Prescribes the structured report format the Cost Accountant must file.In short: Section 268(5)(ii) provides the enabling framework, operationalised through Rule 171(2) and Form 101, against the substantive yardstick in Section 277.

2. When Does Form 101 Actually Get Triggered?

Form 101 is not a self-assessment filing. It activates only when the AO concludes that the nature, complexity, or volume of inventory transactions, or the interest of revenue, warrants independent valuation. Different client profiles carry different exposure:

Assessee Profile Trigger Likelihood Why Large manufacturing entity with multi-SKU, multi-location stock High Complexity + volume + WIP valuation discretion Construction / real estate developer High Section-specific schedules in Form 101; long-cycle inventory Trader with significant inventory variation YoY High Variation triggers AO doubt Commodity / mineral / agricultural produce business High Specialised valuation schedules built into Form 101 Trader with stable margins and clean stock records Medium Possible, but lower probability Service firm with negligible inventory Low Unlikely unless specific revenue concernPractitioner takeaway: If your client falls in the “High” rows above, Form 101 readiness should now be part of your assessment-preparedness checklist — not a reactive scramble after the AO direction lands.

3. Who Triggers, Who Files, Who Pays

This is the part most professionals get wrong on first reading.

The AO triggers it. The Cost Accountant files it. The assessee usually bears the cost.

Specifically:

- The Assessing Officer issues a direction under Section 268(5)(ii), but only with prior approval of the Principal Chief Commissioner / Chief Commissioner / Principal Commissioner / Commissioner of Income-tax.

- The Cost Accountant is nominated by the competent income-tax authority — the appointment is not entirely at the assessee’s discretion and is typically drawn from the panel maintained for this purpose. The taxpayer does not have an open choice as they would in a routine professional engagement.

- The Cost Accountant examines the books, records, stock registers, and (where needed) conducts physical site visits.

- The certified report — Form 101 — is then submitted to the AO.

Practical implication for CAs: If your client receives such a direction, you are not the signing authority on Form 101. Your role becomes one of representation, coordination, and reconciliation — ensuring the Cost Accountant has clean, complete records, and that any variance from your audited financials is explainable.

4. The Timeline: Six Months from a Defined Trigger Point

The report must be furnished within the period specified by the AO, or within an extended period not exceeding six months from the end of the month in which the AO’s direction is received by the assessee.

That trigger point matters. The clock starts not from year-end, not from assessment initiation, but from receipt of the AO’s direction.

Six months sounds long. In practice, for a manufacturing or trading client with multiple SKUs, multi-location stock, work-in-progress, and ICDS adjustments, it is tight.

Action point: The moment a Section 268(5)(ii) direction is received, treat it as a time-critical assignment. Day-one tasks:

- Lock down the stock registers and supporting documents

- Pull cost sheets and valuation workings

- Flag any methodology changes during the year

- Identify ICDS-II departures upfront

5. What Form 101 Actually Contains

Form 101 is structured in two main parts.

A. Certification by the Cost Accountant

Covers the examination of books, valuation of opening and closing inventories, ICDS compliance, and the Cost Accountant’s specific observations and qualifications.

B. Annexure

Part A — Personal Information: Assessee name, PAN, address, contact details, tax year.

Part B — Inventory Valuation Report: This is the heavy section. It covers:

- Nature of business, products, and inventory management system in use

- Methods of accounting and valuation employed — and any changes during the year

- Item-wise valuation for Finished Goods, Work-in-Progress, Raw Materials, Byproducts, Stock-in-trade, and other categories

- Comparison of values as per audited accounts vs. Cost Accountant’s valuation (this is where surprises happen)

- Disclosures on insurance claims, discrepancies, ICDS compliance, and the effect of valuation changes on profit and tax computation

- Specialised schedules for Construction Contracts, Securities held as stock-in-trade, and inventories like livestock, agricultural or forest produce, mineral oils, ores, and gases

The level of granularity is significantly higher than ordinary tax audit disclosures. This is by design — the report becomes the independent reference baseline against which the AO assesses the assessee’s own figures.

6. Documents the Cost Accountant Will Demand

Be ready with:

- Books of account and records relating to purchase, consumption, and sale of inventory items

- Financial statements and stock registers (location-wise, item-wise)

- Cost sheets and valuation workings

- Inventory management system data (ERP extracts, weighted average computations, FIFO logic, etc.)

- Insurance valuations, price lists, and physical verification reports

If your client’s stock records are poorly maintained, the Cost Accountant’s report will say so — and that observation goes straight to the AO.

7. What’s New vs. the Old Form 6D

Form 6D was introduced as recently as 27 September 2023 via CBDT Notification 82/2023 (Income-tax (Twenty-Second Amendment) Rules, 2023, under Rule 14A read with Section 142(2A) of the Income-tax Act, 1961). As confirmed in the CBDT FAQ on Form 101, the new form is positioned as the successor to Form 6D under the Income-tax Act, 2025. Key changes per the official FAQ:

- Alignment with the Income-tax Act, 2025 — section and sub-section references updated.

- “Tax Year” replaces “Assessment Year” — consistent with the new Act’s terminology.

- Simplified, standardised tabular reporting — easier comparability across assessments.

The substance is largely preserved; the packaging is new.

8. The Real Risk for Assessees (and What CAs Should Pre-empt)

Once Form 101 is filed, the AO has an independent, professionally certified valuation sitting in the file. If it differs materially from the assessee’s audited figures, expect:

- Income additions based on the Cost Accountant’s valuation

- Questions on any methodology change during the year

- ICDS-II adjustment scrutiny

- Penalty exposure under the under-reporting / mis-reporting provisions if discrepancies are unexplained

Pre-emption checklist for CAs:

- Ensure the method of inventory valuation is documented and consistently applied.

- Reconcile stock registers ↔ financial statements at every quarter-close, not just year-end.

- Document ICDS-II compliance explicitly, including departures.

- Maintain physical verification reports with proper sign-offs.

- For construction / specialised inventory clients, build dedicated valuation files that align with Form 101’s specialised schedules.

9. The Quiet Message in This Notification

Form 101 is not a routine compliance update. It is a signal.

The Department is industrialising its inventory scrutiny machinery — panels of Cost Accountants are operational, the form is standardised, and the legal framework (Section 268(5)(ii) + Section 277 + Rule 171(2)) is now tightly woven.

For CAs, this means inventory valuation can no longer be a back-office item. It needs to be treated with the same audit-level rigour as related-party transactions or ICDS adjustments.

For assessees — particularly manufacturing, trading, real estate, and commodity businesses — clean, contemporaneous, defensible inventory records are now a direct tax risk-management priority.

10. Bottom Line

Form 101 is not a compliance form. It is a valuation stress test.

If a client’s inventory numbers don’t reconcile with reality, this is where it surfaces. The Department brings its own valuer, its own format, and its own deadline. The only defence is documentation that was clean before the notice arrived.

11. Legal References

- Section 268(5)(ii), Income-tax Act, 2025 — AO’s power to direct independent inventory valuation by a nominated Cost Accountant, with prior approval of the Pr.CCIT / CCIT / Pr.CIT / CIT.

- Section 277, Income-tax Act, 2025 — method of accounting for valuation of purchase, sale and inventory; lower of cost or NRV per ICDS; category-wise comparison; inclusion of taxes/duties incurred to bring goods to current location and condition. (Successor to Section 145A of the 1961 Act.)

- Rule 171(2), Income-tax Rules, 2026 — prescribes Form 101 as the inventory valuation report under Section 268(5)(ii). (Rule 171(1) prescribes Form 100 for the audit report under Section 268(5)(i).)

- Form No. 101 — certification by the Cost Accountant, plus Annexure (Part A: assessee details; Part B: detailed inventory valuation report with specialised schedules for construction contracts, securities held as stock-in-trade, livestock, agri/forest produce, mineral oils, ores and gases).

- ICDS II (Valuation of Inventories) — the underlying computation standard the Cost Accountant must align with.

- Predecessor framework: Form 6D notified by CBDT Notification 82/2023 dated 27 September 2023 under Rule 14A read with Section 142(2A) of the Income-tax Act, 1961.

For ongoing or pre-1-April-2026 assessments, Form 6D and the Section 142(2A) framework continue to govern by virtue of the saving-and-repeal architecture in the Income-tax Act, 2025. Verify the current notification, the relevant CBDT FAQ on Forms under the Income-tax Rules, 2026, and the panel of Cost Accountants maintained by the competent authority before relying on this summary for a specific engagement. For a borderline case, consult an experienced practising chartered accountant or cost accountant.

Comments (0)

No comments yet. Be the first to comment!