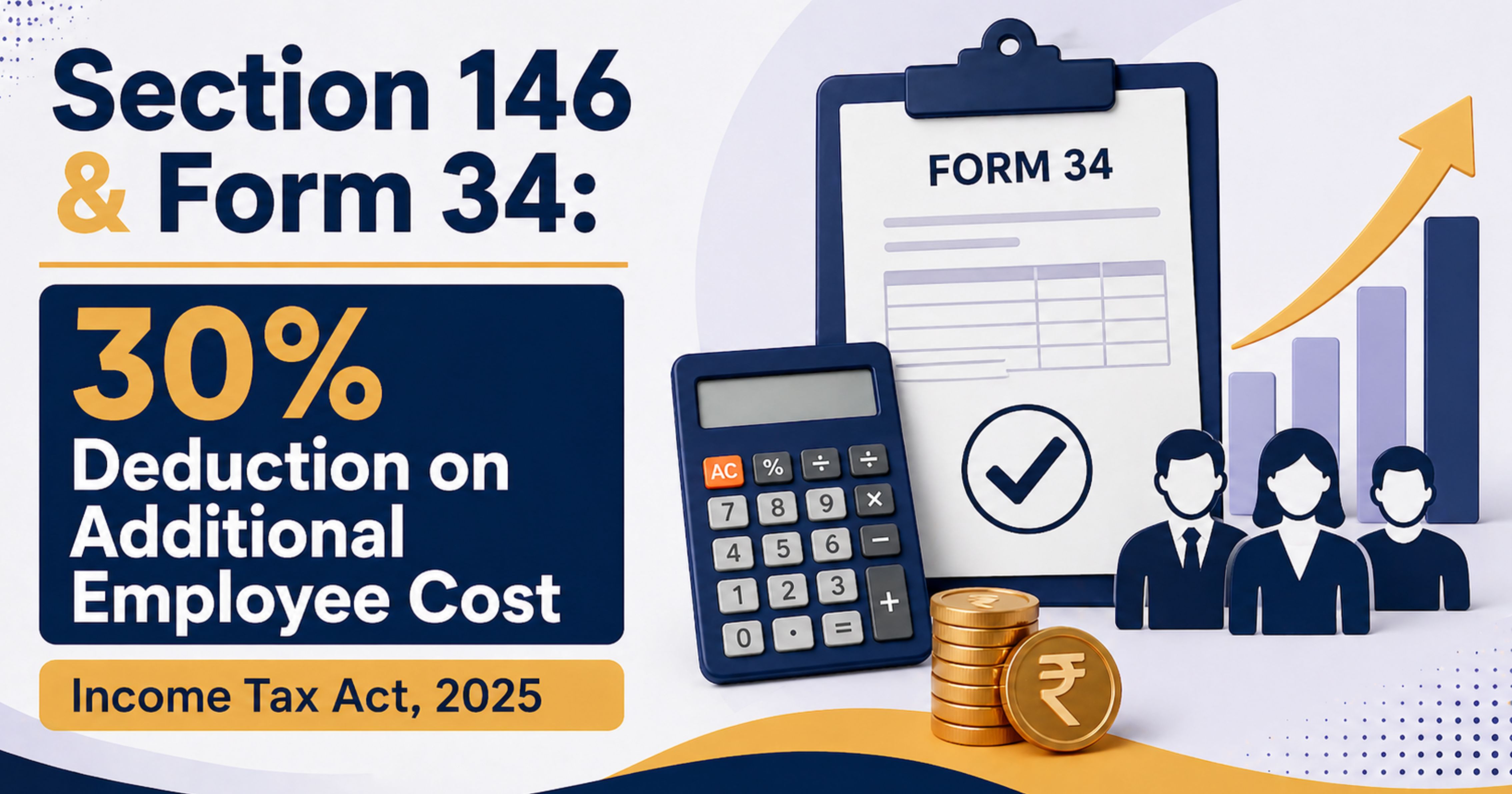

TL;DR: Section 146 of the Income Tax Act, 2025 is the new home of the additional-employee-cost deduction (the old Section 80JJAA). For Tax Year 2026-27 onwards, eligible businesses can claim a 30% deduction on additional employee cost for three consecutive tax years, starting from the year of employment. The claim must be reported in Form 34 (Rule 68 of the Income-tax Rules, 2026), certified by a Chartered Accountant, and filed with the return by every assessee liable to audit under Section 63 (the successor to old Section 44AB). Eligibility is conditional — emoluments cap of Rs. 25,000 per month, minimum 240 days (150 days for apparel, footwear and leather) of employment, banking-channel payment, and Recognised Provident Fund participation are all hard gates. Get any of them wrong and the deduction is disallowed.

1. Introduction

The Income Tax Act, 2025 rewrites the deduction architecture around employment generation. Section 146 takes over the substantive role earlier played by Section 80JJAA, while Form 34 (notified under the Income-tax Rules, 2026) replaces Form 10DA as the prescribed report.

The structural design is the same: reward businesses for net job creation, but only where the new headcount meets specific quality and compliance markers. The numbers, the conditions, and the documentation continue to do most of the work — and the deduction continues to be one of the most frequently disallowed items in scrutiny because of weak compliance with those conditions.

👉 Applicable from Tax Year 2026-27 (FY 2026-27) onwards. Claims for FY 2025-26 (AY 2026-27) continue to be governed by Section 80JJAA of the 1961 Act and Form 10DA of the 1962 Rules.

2. What Section 146 Actually Provides

Section 146 allows an eligible assessee to claim, in addition to other deductions, a sum equal to:

- 30% of the additional employee cost incurred in the course of business or profession,

- For the previous year in which the additional employees are employed, and

- For the two immediately succeeding tax years — i.e., a deduction window of three consecutive tax years starting from the year of employment.

The deduction is over and above the salary expense already debited to the profit and loss account — the salary itself remains an allowable business expenditure under the normal computation rules; Section 146 layers an additional 30% on top, for three years.

This makes hiring not just an operational decision but a tax-planning lever — provided every condition is met.

3. Form 34: The New Prescribed Report

The deduction is not self-claiming. To rely on Section 146, the assessee must:

- Obtain a report in Form 34 (Rule 68 of the Income-tax Rules, 2026) from a practising Chartered Accountant,

- Confirming that the deduction has been correctly computed in line with Section 146 and the rules thereunder, and

- Furnish the report along with the return of income.

The Form 34 obligation applies in particular to every assessee liable to audit under Section 63 — the successor to old Section 44AB. Where the assessee is not otherwise audited, the Form 34 report is the standalone CA certification on which the claim rests.

👉 Non-furnishing of Form 34 with the return is a recurring trigger for disallowance. Late filing of the return, or filing the report after the return, has historically been treated as fatal to the claim under the analogous old regime — the new Act preserves the same discipline.

4. Who Can Claim the Deduction

The deduction is available to every assessee:

- Having income chargeable under the head Profits and gains of business or profession,

- Whose accounts are required to be audited under Section 63 of the new Act, and

- Whose headcount has actually increased during the previous year on account of employment of additional employees meeting the conditions below.

Net hiring is the gating fact — if there is no increase in the total number of employees compared to the immediately preceding year, no Section 146 deduction is available, however many fresh hires the business may have made on a gross basis.

5. Key Conditions to Claim Deduction

a) Additional Employees Only

Only the cost of additional employees qualifies. An employee counts as additional only to the extent that the total number of employees in the business at the end of the previous year exceeds the total number at the end of the immediately preceding previous year.

👉 Hire 50 but lose 50 to attrition → net additional employees: zero → no deduction.

b) Emoluments Cap of Rs. 25,000 per Month

- Total emoluments paid to an additional employee must not exceed Rs. 25,000 per month.

- Note: the law uses the word emoluments — this is wider than “basic salary” and covers all sums paid to or payable to the employee in connection with the employment, but excludes employer’s contribution to PF / pension and lump-sum termination payments (see Section 7 below).

c) Minimum Days of Employment

Industry Minimum Days in the Previous Year General businesses 240 days Apparel, footwear and leather industries 150 daysImportant — the second-year deeming rule: If an additional employee in the specified industries (apparel/footwear/leather) is employed for fewer than 150 days in the year of joining, but completes 150 days or more in the immediately succeeding tax year, the employee is treated as an additional employee of that succeeding year. The three-year deduction window then runs from that succeeding year. This protects late-year hires from losing the deduction entirely.

d) Mode of Payment

Emoluments to the additional employee must be paid by:

- Account-payee cheque / account-payee bank draft,

- Electronic clearing system through a bank account, or

- Any other prescribed electronic mode.

Cash payment of emoluments to the additional employee is not eligible for the Section 146 deduction.

e) Provident Fund Participation

- The additional employee must participate in a Recognised Provident Fund.

- The deduction is not available in respect of any employee for whom the entire contribution under the Employees’ Pension Scheme is paid by the Government (typically under specific government employment-incentive schemes).

6. Cases Where the Deduction Is NOT Allowed

Section 146 is not available in the following situations:

- Where the business is formed by splitting up or reconstruction of an existing business (with the limited carve-outs the statute itself provides).

- Where the business is acquired by way of transfer from another person, or as a result of business reorganisation.

- Where the assessee fails to furnish Form 34 along with the return of income.

- Where any of the substantive conditions in Section 146 (emoluments cap, days of employment, mode of payment, PF participation) is not met for a given employee — the disallowance is computed employee-by-employee, not at the assessee level.

👉 The split/reconstruction and transfer carve-outs are designed to ensure that the deduction rewards genuine net job creation, not paper restructurings that simply shuffle existing headcount into a new entity.

7. What Counts as “Additional Employee Cost”

For the purpose of Section 146, “additional employee cost” is the total emoluments paid or payable to additional employees during the previous year.

Included Excluded Salary, wages, and any sum paid or payable to the additional employee in connection with employment Employer’s contribution to any provident fund or pension fund Allowances and similar payments forming part of regular emoluments Lump-sum payments at the time of termination, voluntary retirement or superannuation Any retirement benefit or gratuity-type paymentSpecial rule for the year a business is set up: in the very first year the business is set up, all employees employed during that year (subject to the other conditions) are treated as additional employees, and the total emoluments paid to them is the additional employee cost for that year.

8. Old Law → New Law: Quick Mapping

Old Framework (1961 Act / 1962 Rules) New Framework (2025 Act / 2026 Rules) Section 80JJAA — deduction for additional employee cost Section 146 — deduction for additional employee cost Form 10DA — CA-certified report Form 34 — CA-certified report Rule 19AB — report-prescription rule Rule 68 — report-prescription rule Section 44AB — tax audit obligation Section 63 — tax audit obligationFor practitioners, the practical implication is: read the new Section 146 alongside the old Section 80JJAA jurisprudence. ITAT and High Court rulings under the old regime — on what counts as “reconstruction”, on the second-year deeming for short-duration employees, on Form-filing timelines — will continue to be persuasive authority on identical-language provisions in the new Act, though they are not binding precedent on the new statute.

9. Practical Insight: Why This Deduction Gets Disallowed

A scan of disallowance jurisprudence under the old Section 80JJAA reveals a consistent pattern. Common failure points:

- Headcount classification errors — counting transferees from group companies as “additional employees”, or failing to apply the net-headcount test correctly.

- PF non-compliance — missing PF registration for newly hired employees, or counting employees who are not actually contributing to a recognised PF.

- Days-of-employment shortfall — not maintaining proof of 240 / 150 days, or miscounting the period when employees join mid-year.

- Cash-payment leakage — emoluments routed partly in cash, breaching the banking-channel requirement for the entire claim relating to that employee.

- Form 10DA / Form 34 not filed with the return, or filed after the return — the most common reason for disallowance, and the easiest to avoid.

👉 The deduction is documentation-heavy. Spreadsheet schedules, payroll-system extracts, PF-portal acknowledgements, and bank-payment proofs need to be reconciled and filed in a defensible package before the return is filed — not after a notice arrives.

10. Action Points for Tax Year 2026-27

- Map the headcount: lock down the total number of employees as on 31 March 2026 and 31 March 2027 — that’s the net-addition test.

- Identify the eligible cohort: from the gross hires in FY 2026-27, filter for employees with emoluments ≤ Rs. 25,000/month, ≥ 240 days (or 150 days for specified industries), banking-channel paid, and active in a recognised PF.

- Reconcile against payroll: payroll system + PF portal + bank statements should agree on every eligible employee. Mismatches are the single biggest scrutiny risk.

- Watch the second-year deeming: in apparel/footwear/leather industries, late-year joiners may roll into the next year’s claim — track them.

- File Form 34 with the return, on time. Not after.

- Retain documentation for the full deduction window: the 30% deduction runs for three years — the supporting documents need to support all three claims.

11. Conclusion

Section 146 under the Income Tax Act, 2025 is a powerful incentive for employment generation, offering real tax savings — 30% of additional employee cost, for three consecutive tax years.

However, the benefit is not automatic. It requires strict compliance with the headcount, emoluments, days-of-employment, payment-mode and PF conditions; correct CA-certified reporting in Form 34 under Rule 68; and timely filing along with the return of income.

Final takeaway: Hiring can reduce tax — but only if done correctly and compliantly. Build the eligibility checklist into HR and payroll workflows from the day the new hire joins, not into the audit working papers in September.

12. Legal References

- Section 146, Income Tax Act, 2025 — deduction in respect of employment of new employees (additional employee cost).

- Section 63, Income Tax Act, 2025 — audit of accounts of certain assessees (successor to Section 44AB of the 1961 Act).

- Rule 68, Income-tax Rules, 2026 — prescription of report in Form 34 for the purposes of Section 146.

- Section 80JJAA, Income-tax Act, 1961 — pre-2026 provision; continues to govern claims for FY 2025-26 and earlier.

- Form 10DA, Income-tax Rules, 1962 — predecessor of Form 34; used for Section 80JJAA claims under the old regime.

This article is a practitioner-oriented summary. Statutes, rules and forms are subject to amendment and CBDT clarifications. Verify the latest gazette notifications, CBDT circulars and the exact rule / form text on incometaxindia.gov.in before relying on this summary for a specific computation. For a borderline case, consult an experienced practising chartered accountant.

Comments (0)

No comments yet. Be the first to comment!